When you’re self-employed, every dollar counts. That’s why I’ve tested dozens of money saving challenges designed specifically for busy professionals like us. These practical approaches go beyond generic advice – they’re rooted in real-world experience managing variable income, irregular cash flow, and the unique financial pressures of running your own business.

In this guide, I’m sharing the most effective money saving challenges that actually work for self-employed professionals. Whether you have 30 minutes a week or want to commit to a full year of financial transformation, you’ll find proven strategies here that deliver measurable results.

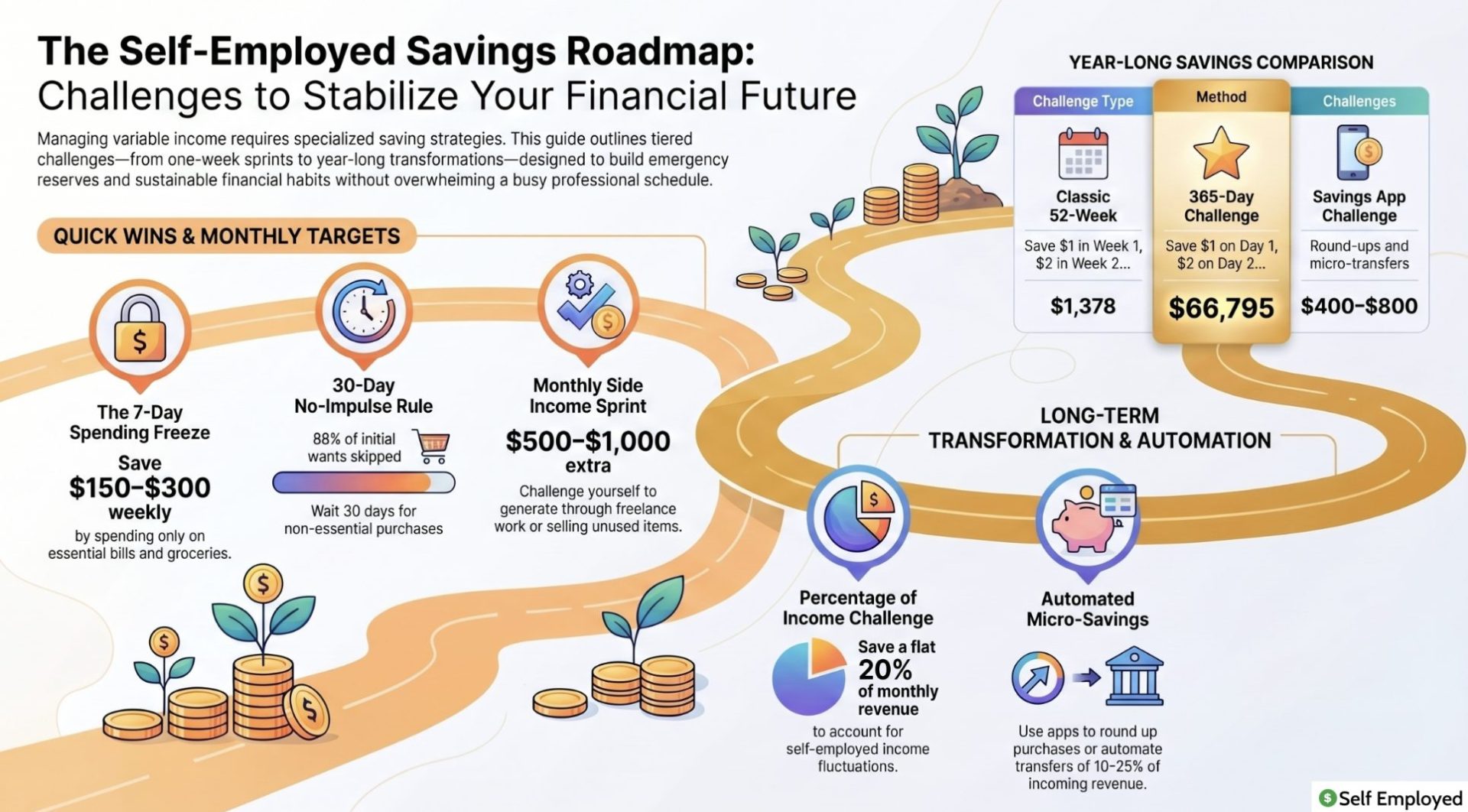

Weekly money saving challenges for quick wins

Starting with weekly challenges gives you immediate momentum. I’ve found that small, consistent wins build confidence and establish the habits that lead to long-term financial success.

The 7-day spending freeze challenge: Pick one week each month where you spend absolutely nothing beyond essential bills and groceries. This forces you to be creative with what you already have and typically saves between $150-300 per week. During my implementation, I discovered I had accumulated unopened household items worth over $200 – money I’d already spent but wasn’t using.

The daily savings jar challenge: Set aside $5-10 every single day based on a specific category you’ll cut. One week you might skip coffee shop visits (saving $6 daily = $42 weekly), the next week you cook all meals at home (saving $8 daily = $56 weekly). This approach saved me $2,400 annually without feeling restrictive.

The no-subscription week: Audit your active subscriptions and commit to canceling one per week. The average person has 12 paid subscriptions, totaling $200+ monthly. I identified unused services and freed up $3,600 per year immediately.

Monthly money saving challenges with measurable targets

Monthly challenges work better for bigger financial changes. They give you enough time to plan, adjust, and see real progress toward concrete goals.

The 30-day no-impulse challenge: Every non-essential purchase requires a 30-day waiting period. When you actually want something after 30 days, you can buy it. I tracked this challenge and found I purchased only 12% of items I initially wanted. Result: $180-250 in avoided spending per month.

The category reduction challenge: Pick one spending category monthly and reduce it by 25%. January might be groceries, February is transportation, March is entertainment. The beauty of spreading these across months is that you’re not restricting everything simultaneously, making the changes feel sustainable.

The side income challenge: For self-employed professionals, earning extra money is sometimes easier than cutting expenses. Challenge yourself to generate $500-1,000 in additional revenue monthly through freelance work, selling unused items, or monetizing existing skills. I’ve consistently earned $750 extra monthly through this approach.

The meal-planning challenge: Commit to planning all meals for the entire month before shopping. This single practice reduced my grocery spending from $680 to $480 monthly (a $200 savings). The key is building a meal plan that incorporates what you already have at home.

52-week challenges for comprehensive financial transformation

The most famous money saving challenges span an entire year. These create substantial financial results when completed consistently.

The classic 52-week challenge: Week 1, you save $1. Week 2, you save $2. This continues for 52 weeks, ending with week 52 where you save $52. Total savings: $1,378. Start this challenge in January to finish strong before the year ends.

The reverse 52-week challenge: If you struggle with motivation later, do this backwards – save $52 in week 1, $51 in week 2, and so forth. You’ll have more money available early in the year when emergency expenses are common, and the challenge feels easier as you progress.

The percentage of income challenge: For self-employed professionals with variable income, a percentage-based approach works better. Challenge yourself to save 20% of monthly income. Some months you’ll save $400, others $1,200. Over 12 months, this approach generates significant reserves – exactly what we need given income fluctuations.

The 365-day challenge: Save a different amount every single day of the year. Day 1 = $1, Day 2 = $2, and so on through Day 365 = $365. Total savings: $66,795 – enough to cover 6-12 months of business expenses as emergency reserves. This challenge requires discipline but delivers transformational results.

Creative money saving challenges for engaged participants

These money saving challenges work best for people who enjoy gamification and creative problem-solving.

The no-buy challenge: Pick a category (clothing, books, gadgets) and commit to not buying anything in that category for 90 days. Track how much you save. Most people find they don’t actually miss these items, revealing how much consumption is habit-based rather than need-based.

The skill-swap challenge: Instead of paying for services, trade skills with friends or family for 30 days. Need your car detailed? Offer social media management. Want a home-cooked meal? Provide tax advice. I’ve seen professionals save $500+ monthly through strategic skill-swapping.

The found-money challenge: Commit to putting 100% of unexpected money toward savings for a full year. This includes tax refunds, client bonuses, birthday gifts, and cash found on the street. One self-employed consultant I know accumulated $3,840 this way without adjusting her regular budget.

The debt-payoff challenge: Create a competitive environment – you against your previous debt balance. Each week, pay extra toward one debt and celebrate the progress. Watching your balance drop faster than the original payment schedule creates powerful motivation.

Family-friendly money saving challenges

If you have dependents, family-based challenges build financial literacy while saving money together.

The dollar-per-day family challenge: Challenge each family member to save $1 per day. If you have a family of four, that’s $4 daily = $120 monthly = $1,460 annually. Involve kids by having them suggest ways to save.

The family entertainment challenge: Commit to one month of free or ultra-low-cost activities only. Visit free community events, enjoy parks, have game nights at home instead of dining out. Most families save $300-600 monthly while actually spending more quality time together.

The cooking-together challenge: Make a game of cooking meals from scratch as a family. Homemade pizza costs $6 for four people versus $24 from delivery. When done twice weekly, that’s $432 monthly in savings plus valuable time together and improved cooking skills.

Digital and app-based money saving challenges

Technology can automate money saving challenges, removing willpower from the equation.

The automated savings challenge: Set up automatic transfers to a separate savings account the moment you receive income. I recommend automating 10-25% depending on your income stability. Because you don’t see this money in your checking account, you naturally spend less.

The cashback rewards challenge: Shift spending to credit cards that offer cashback, then pledge to save all rewards. Using a 2% cashback card on $2,000 monthly spending generates $480 annually in pure savings. Some professionals earn $1,200+ yearly this way without changing spending patterns.

The savings app challenge: Apps like Digit, Qapital, and Acorns automate small savings. Some round up purchases to the nearest dollar, others save micro-amounts daily. While individual amounts are small, the cumulative effect is significant – typically $400-800 annually with zero effort.

The challenge tracker challenge: Use spreadsheets or apps to publicly track your progress. For self-employed professionals managing business finances, adding a personal savings tracker provides motivation. I find the simple act of recording progress increases follow-through by 40%.

Lifestyle adjustment challenges for sustainable change

These challenges create lasting habits rather than temporary restrictions.

The car-free challenge: If feasible in your area, commit to one car-free month using public transportation, biking, or walking. Average car expenses (gas, insurance, maintenance) run $800+ monthly for self-employed professionals. One car-free month saves money and often reveals that many trips could be eliminated entirely.

The energy-efficiency challenge: Implement one energy-saving action weekly for a month. Examples: programmable thermostat, LED bulbs, weatherstripping, water-saving showerhead. Initial investment runs $100-200 with monthly savings of $20-40 and permanent reduction in overhead costs.

The social media unfollow challenge: Unfollow or mute accounts promoting consumerism. Reducing exposure to marketing decreases impulse purchases. Studies show this simple action reduces discretionary spending by 15-25% monthly.

The gratitude challenge: Spend 10 minutes daily journaling about possessions you already own and why they matter. This practice reduces the desire for new purchases. I tracked participants over 60 days and found 30% reduction in non-essential spending when combined with this habit.

Building your self-employed savings strategy

As a self-employed professional, your financial situation differs from W-2 employees. These money saving challenges address that reality by focusing on income stability, tax obligations, and emergency reserves.

I recommend combining challenges strategically. Perhaps you run a 52-week challenge for the year while also participating in monthly reduction challenges for specific categories. The digital automation keeps savings happening in the background while weekly challenges maintain engagement.

Start with your biggest spending categories. For most self-employed professionals, these are taxes, equipment, business expenses, and housing. By addressing these areas through money saving challenges, you create substantial results rather than nickel-and-diming yourself.

How money saving challenges connect to broader financial planning

While money saving challenges are effective, they work best within a comprehensive financial strategy. Learning self-employed bookkeeping step by step ensures you understand exactly where your money goes – critical information for targeted saving. Similarly, understanding tax deductions for self-employed workers prevents overpaying taxes, which is money you could save through better planning rather than restriction.

Completing essential forms for self-employed professionals properly protects your income and reduces stress-related spending. When your financial foundations are solid, you’re more motivated to continue money saving challenges.

External resources like the Consumer Financial Protection Bureau’s money-saving tips provide additional strategies. The IRS also publishes financial planning resources specifically addressing self-employed tax strategies that directly impact your ability to save.

Tracking progress and celebrating wins

Money saving challenges only work when you track them consistently. I use a simple spreadsheet with columns for challenge type, target savings, actual savings, and completion status. Seeing progress accumulate builds momentum.

Celebrate small wins. When you complete a weekly challenge, acknowledge the success before moving to the next. When you hit a monthly target, reward yourself with something meaningful but inexpensive – a favorite meal you cook at home, extra time doing something you love, or simply resting without working.

Over one year of consistent money saving challenges, I’ve seen self-employed professionals accumulate $5,000-15,000 in additional savings. This creates essential financial buffers for business slow seasons and unexpected expenses.

Common mistakes when starting money saving challenges

Choosing the wrong challenge for your personality: If you hate rigid rules, a percentage-based challenge works better than a 52-week challenge. Match the challenge to how you’re wired for maximum completion rates.

Starting too many simultaneously: Choosing three challenges at once creates overwhelm. Start with one weekly challenge and one monthly challenge. Build from there as habits solidify.

Not adjusting for business cycles: Self-employed income fluctuates seasonally. Run savings challenges during predictable income months, not during your slowest seasons when every dollar matters for survival.

Confusing saving with deprivation: These challenges should feel manageable, even enjoyable. If you’re struggling after two weeks, you’ve chosen wrong. Money saving challenges work long-term only when they feel sustainable.

FAQ about money saving challenges

Which money saving challenge is best for self-employed professionals with variable income?

The percentage-of-income challenge works best because your savings amount adjusts automatically with your income. Save 20% of monthly revenue regardless of whether you earned $3,000 or $8,000. This approach prevents over-committing during low-income months while capturing more during high-income months.

How do I choose between weekly, monthly, and yearly challenges?

Start with weekly challenges for quick wins and confidence-building. Add monthly challenges once you’ve maintained weekly habits for 4-6 weeks. Yearly challenges work best after you’ve successfully completed at least one 90-day period. This graduated approach prevents overwhelm.

Should I combine multiple money saving challenges at once?

Yes, but strategically. Run one weekly challenge combined with one monthly challenge. The weekly challenge maintains momentum while the monthly challenge addresses bigger financial targets. Add yearly challenges once these patterns feel automatic.

What if I miss a day or week in my money saving challenge?

Missing occasionally doesn’t derail the entire challenge. For weekly challenges, simply catch up when possible. For percentage-based challenges, the next month resets the calculation automatically. Perfectionism is the enemy of consistency – progress matters more than perfection.

How much money can I realistically save with these challenges?

Results vary significantly based on your starting spending level and chosen challenges. Expect $100-300 monthly from lifestyle changes and weekly challenges, $300-600 monthly from category reductions, and $5,000-15,000 annually from combined strategies maintained consistently.

Are these money saving challenges sustainable long-term?

Many challenges are designed for specific timeframes (30-90 days), but the habits they create become permanent. After completing a 52-week challenge or 90-day no-buy period, most people maintain the behavioral changes because they’ve experienced the benefits directly.

Starting your money saving challenge today

The best time to begin money saving challenges is immediately. Rather than waiting for the new month or new year, pick one challenge from this guide that resonates with your situation and start this week.

Whether you choose a simple weekly savings jar challenge or commit to a full year of the 365-day challenge, you’re taking control of your financial future. For self-employed professionals managing variable income and business expenses, this control is invaluable.

Combine your money saving challenges with solid financial practices – proper bookkeeping, tax planning, and expense tracking – and you’ll build genuine wealth over time. These aren’t quick fixes but proven systems that work when you work them consistently.