Understanding self employed tax forms is one of the most important steps you can take to avoid penalties, stay compliant, and keep more of your money. I’m Elliot, and after helping countless independent workers navigate their tax obligations, I can tell you that the single most common (and costly) mistake is missing a form or filing something incorrectly. This guide breaks down exactly which forms matter, when they’re due, and how to handle each one – whether you’re a freelancer, independent contractor, or small business owner.

Why self employed tax forms are different from employee filings

Traditional W-2 employees receive a single form at year-end and file a relatively straightforward return. Self-employed individuals face a different reality: you are responsible for reporting your own income, calculating your own tax liability, paying estimated taxes quarterly, and filing multiple forms that employees never see. Miss a deadline, miscalculate estimated taxes, or leave out a form, and penalties follow quickly. The IRS processes self-employment returns with close attention to Schedule C and Schedule SE, and discrepancies trigger automatic flags.

The One Big Beautiful Bill Act, signed into law on July 4, 2025, made many Tax Cuts and Jobs Act provisions permanent and introduced new deductions for self-employed workers, including tip income and overtime deductions. This makes it even more important to stay current on which forms to use and how to claim new benefits.

Form W-9: Request for Taxpayer Identification Number

Every self-employed engagement starts here. Clients request a W-9 before they can pay you as an independent contractor, because they need your Taxpayer Identification Number (SSN or EIN) to file accurate 1099s at year-end.

You complete the W-9, not the client. Keep blank copies ready so you can respond immediately when a new client requests one – delays can hold up your first payment. The W-9 itself doesn’t affect your taxes directly, but it sets the chain in motion that leads to the 1099 forms you’ll report at filing time.

When to complete: whenever a client requests it, at the start of any new business relationship.

Form 1099-NEC: Nonemployee Compensation

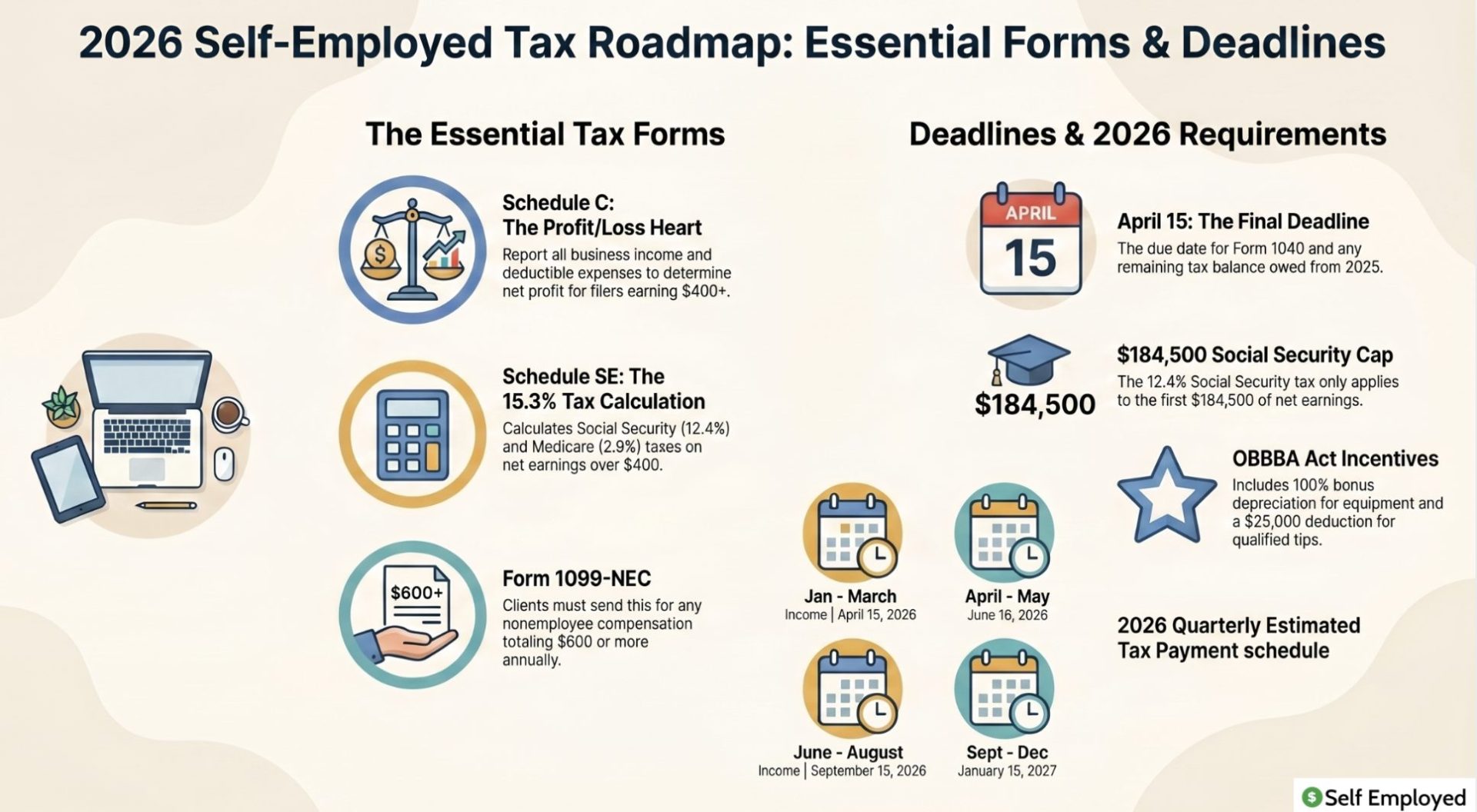

Clients who pay you $600 or more in a calendar year must file Form 1099-NEC with the IRS and send you a copy by January 31. This is how the IRS verifies that your self-employment income matches what clients report paying you.

You will receive 1099-NEC forms from all qualifying clients each February. Keep these organized – you’ll need them to verify your income when completing Schedule C. Report all 1099-NEC income on your federal return. If a client fails to send a 1099, you still need to report the income. The IRS cross-matches client 1099 filings against your return, and unreported income triggers automatic notice letters. For detailed guidance on 1099 requirements, the IRS Form 1099-NEC page covers filing deadlines and exceptions.

Schedule C: Profit or Loss from Business

Schedule C is the heart of self-employment tax filing. This is where you report all business income and every deductible business expense, arriving at your net profit – the number that feeds both your income tax calculation and your self-employment tax on Schedule SE.

Schedule C is organized into five parts: income, expenses, cost of goods sold, vehicle information, and other business details. The expenses section is where most self-employed individuals have room to reduce their tax bill significantly. Common deductible categories include home office, vehicle mileage, software subscriptions, advertising, professional development, supplies, and professional service fees.

You must file Schedule C if your net self-employment income is $400 or more. Even a net loss can be valuable – Schedule C losses offset other income on your return, which can reduce your overall tax liability. Maintaining strong bookkeeping for the self-employed throughout the year makes completing Schedule C straightforward and defensible in the event of an audit.

Schedule SE: Self-Employment Tax

Schedule SE calculates your self-employment tax – the 15.3% that covers Social Security (12.4%) and Medicare (2.9%). This is the tax that catches most first-year freelancers off guard, because it’s on top of your income tax, not instead of it.

The Social Security portion applies to net self-employment earnings up to $184,500 for 2026 (up from $176,100 in 2025). The Medicare portion applies to all net self-employment income with no cap, plus an additional 0.9% surtax on earnings over $200,000 for single filers.

One important offset: you can deduct half of your self-employment tax (the employer-equivalent portion) from your adjusted gross income on Form 1040. This above-the-line deduction is available whether or not you itemize, and it reduces your income tax at both the federal and state levels. File Schedule SE whenever your net self-employment earnings reach $400 or more.

Form 1040: U.S. Individual Income Tax Return

Form 1040 is your main federal tax return. Schedule C and Schedule SE both attach to your 1040. This is where your total income, all deductions, and your final tax liability come together. The due date is April 15, with an extension available to October 15 (though extension of time to file does not extend time to pay).

The One Big Beautiful Bill Act extended and expanded several deductions that affect self-employed filers. Notably, for 2025 through 2028, individuals in eligible tip-receiving occupations can deduct up to $25,000 in qualified tip income annually. Bonus depreciation (100% first-year expensing) applies to qualifying business property purchased after January 19, 2025. Consult the IRS guidance on OBBBA provisions for a full breakdown of changes affecting your 2025 return.

Form 1040-ES: Quarterly Estimated Tax Payments

If you expect to owe $1,000 or more in federal taxes after withholding and credits, you are required to make quarterly estimated payments. This is how self-employed individuals pre-pay their income tax and self-employment tax throughout the year, rather than owing a large lump sum in April.

The quarterly payment schedule is:

- April 15 (for January-March income)

- June 16 (for April-May income)

- September 15 (for June-August income)

- January 15 of the following year (for September-December income)

The safe harbor calculation: pay 100% of your prior year’s total tax liability across four installments (or 110% if your AGI exceeded $150,000). This protects you from underpayment penalties regardless of how your current year income changes. Use Form 1040-ES worksheets to calculate each payment, or pay directly through IRS Direct Pay or the Electronic Federal Tax Payment System (EFTPS).

Form 8829: Home Office Deduction

If you claim the home office deduction using the actual expense method, you file Form 8829 to calculate the allowable deduction based on the percentage of your home used exclusively and regularly for business. The simplified method ($5 per square foot, up to 300 square feet) does not require Form 8829 – you report it directly on Schedule C.

The home office deduction is often under-claimed because self-employed individuals either don’t realize they qualify or fear it will trigger an audit. In practice, a properly calculated and documented home office deduction is entirely legitimate. Your home office deduction guide covers the qualification requirements and calculation methods in detail.

Other important forms

Schedule 1 (Additional Income and Adjustments) reports other income sources – rental income, alimony, prizes – and above-the-line deductions including your self-employment tax deduction and self-employed health insurance deduction. Most self-employed individuals will file Schedule 1 alongside their main 1040.

Form 4562 (Depreciation and Amortization) is required if you’re deducting depreciation on business equipment or vehicles. With 100% bonus depreciation available for qualifying property under current law, many self-employed individuals can fully deduct major equipment purchases in the year of purchase.

State tax forms vary by state but generally mirror the federal structure – your state income tax return starts with your federal adjusted gross income and applies state-specific adjustments. Review your specific state’s requirements, especially if you operate across state lines. See our state self-employment tax guides for state-specific filing requirements.

Common filing mistakes to avoid

The most costly mistake is underreporting income. The IRS receives copies of all 1099 forms filed against your SSN and automatically matches them to your return. If your reported income is lower than your 1099 total, you’ll receive a CP2000 notice and owe the difference plus interest and penalties.

Missing quarterly payment deadlines is another frequent issue. The IRS charges underpayment penalties from the date the payment was due, not from April 15. Missing even one quarterly payment can add up to meaningful penalties on a large tax liability.

Claiming home office or vehicle deductions without documentation is a risk. Keep a contemporaneous mileage log, retain receipts for home office expenses, and document your home office measurements. Auditors ask for this documentation routinely.

Frequently Asked Questions

What self employed tax forms do I need to file?

Most self-employed individuals need Schedule C (business income and expenses), Schedule SE (self-employment tax), Form 1040 (main return), and Form 1040-ES (quarterly estimated payments). You may also need Schedule 1, Form 8829 (home office), and Form 4562 (depreciation). State returns require their own forms, which vary by state.

When is the deadline for filing self-employed taxes?

The federal filing deadline is April 15. You can request an automatic extension to October 15, but any taxes owed are still due by April 15. Quarterly estimated payments have separate deadlines: April 15, June 16, September 15, and January 15 of the following year.

Do I need to file if my self-employment income is below $400?

No Schedule SE or self-employment tax is required if your net self-employment earnings are under $400. However, you must still file Form 1040 if you meet other income filing thresholds, and you should still report any gross income on Schedule C even if expenses reduce your net below $400.

What happens if I don’t make quarterly estimated tax payments?

The IRS charges an underpayment penalty calculated as a percentage of the underpaid amount for each day it was late. For 2026, the underpayment rate is typically around 7-8% annually. The safe harbor rule protects you if you pay 100% of your prior year’s tax liability (110% if your prior-year AGI exceeded $150,000) across four quarterly payments.

What is the difference between Schedule C and Schedule SE?

Schedule C calculates your net profit from business activities – income minus deductible expenses. Schedule SE takes that net profit and calculates your self-employment tax (15.3% for Social Security and Medicare). Both forms attach to your Form 1040. Schedule SE uses the net profit figure from Schedule C as its starting point.

Should I hire a professional for my self-employed taxes?

For simple situations with one income source and straightforward expenses, quality tax software like TurboTax Self-Employed or TaxAct handles the forms well. If you have multiple clients, significant asset purchases, home office claims, or earn over $100,000, a CPA or enrolled agent who specializes in self-employment can often save more in taxes than their fee costs.