After years of being self-employed, I learned the hard way that skipping dental insurance isn’t an option if you want to protect your health and financial stability. When you’re self-employed, there’s no employer coverage waiting for you, and one unexpected root canal can quickly drain your emergency fund. I’ve compared dozens of dental insurance plans for self-employed workers, and I can tell you that the right coverage doesn’t have to be expensive or complicated. This guide will walk you through everything you need to know about getting dental insurance for self employed professionals, including plan types, costs, and how to maximize tax benefits.

Dental problems don’t wait for a convenient time in your business cycle. Whether you develop a cavity, need a crown, or face an unexpected extraction, dental care costs can range from a few hundred dollars to several thousand. The average American dental procedure costs between $150 for a basic cleaning and $1,500 or more for root canal treatment. Without dental insurance for self employed coverage, these expenses come directly from your pocket and can significantly impact your business cash flow.

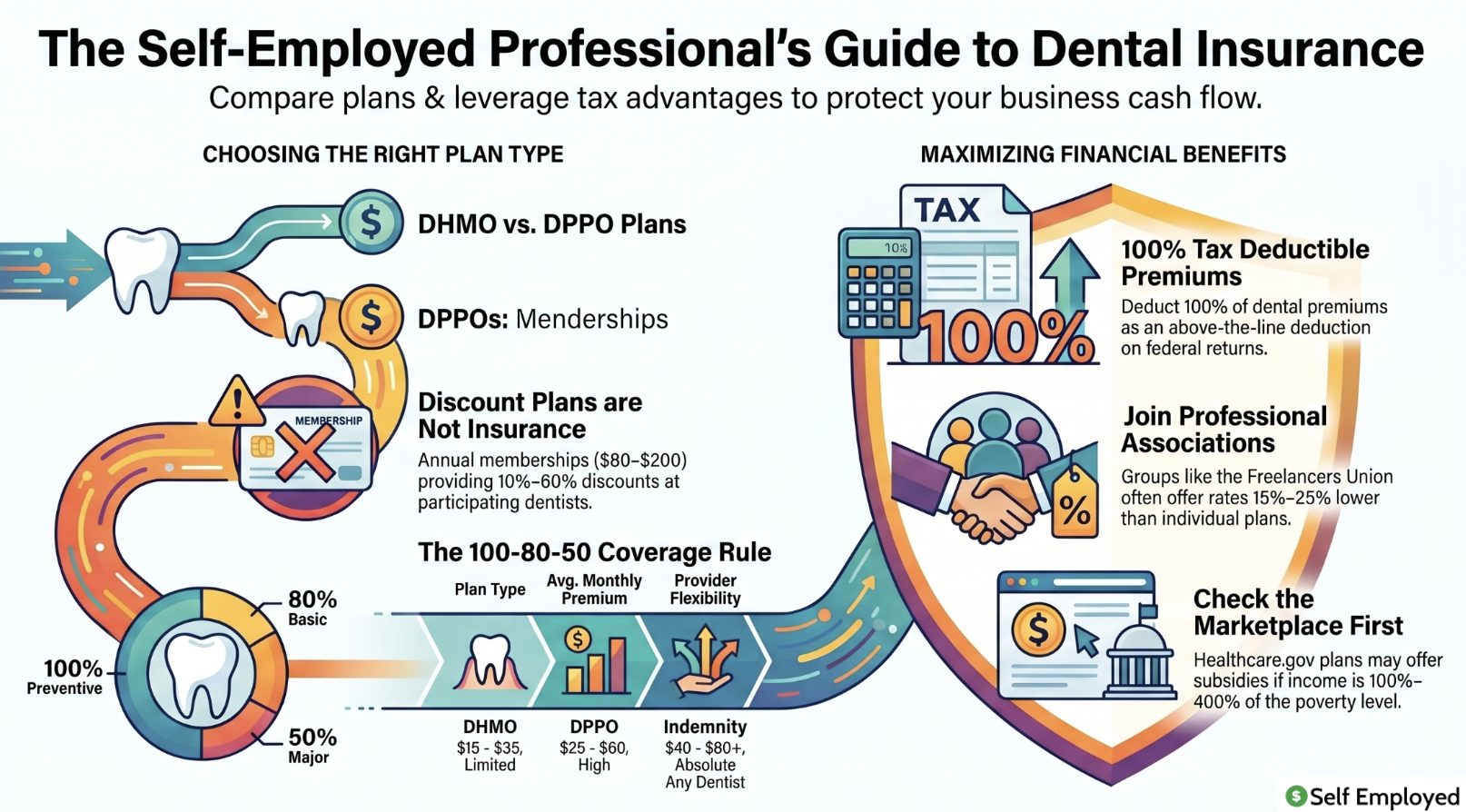

Understanding the types of dental insurance for self employed plans

When shopping for dental insurance for self employed coverage, you’ll encounter four main plan types. Each has different cost structures, provider networks, and coverage levels. Understanding these options is crucial for making the right choice for your specific situation and budget.

DHMO plans (Dental Health Maintenance Organization): These plans feature the lowest monthly premiums, typically ranging from $15 to $35 per month. In exchange, you choose a primary dentist from the plan’s network and pay low co-pays for services (usually $0 to $25 per visit). However, DHMO plans often require referrals for specialists and may have limited coverage for major procedures like implants. Most DHMO plans include two free annual cleanings and exams with no co-pay.

DPPO plans (Dental Preferred Provider Organization): DPPO plans sit in the middle price range, with premiums between $25 and $60 monthly. They offer more flexibility than DHMO plans, allowing you to see any dentist without referrals. You’ll typically pay a co-pay for preventive services and a percentage of the cost for major work. Most DPPO plans cover 50% of crowns, fillings, and root canals after you meet your annual deductible (usually $50 to $100). Coverage for orthodontics is sometimes available at additional cost.

Indemnity plans: Traditional indemnity plans give you the most freedom to choose any dentist, but they come with higher monthly premiums ($40 to $80+) and higher out-of-pocket costs. You pay upfront and submit claims for reimbursement. The plan reimburses you based on its fee schedule, which might be lower than your dentist actually charges. These plans work best if you have an established relationship with a specific dentist outside any network.

Discount dental plans: These aren’t insurance at all, but membership programs offering 10% to 60% discounts at participating dentists. At $80 to $200 annually, they’re the cheapest option but don’t provide insurance protection. They work best for routine care if you’re generally healthy and don’t expect major dental work.

Finding affordable dental insurance for self employed professionals

As someone who’s navigated multiple plan selections, I’ve found that the most affordable dental insurance for self employed coverage often comes from these sources. Each option has advantages and limitations worth considering.

Healthcare.gov marketplace: The federal health insurance marketplace includes dental plans alongside medical coverage. You can view standalone dental plans or dental benefits included with medical plans. Visit Healthcare.gov and enter your information to see plans available in your area. Many marketplace plans qualify for subsidies if your income falls between 100% and 400% of the federal poverty level, making dental insurance for self employed professionals significantly more affordable. Open enrollment typically runs from November through January.

Professional associations and membership organizations: Many self-employed professionals qualify for group rates through industry associations. Freelancers Union members, National Association for the Self-Employed members, and trade-specific organizations often negotiate group dental plans. These plans typically cost 15% to 25% less than individual policies because of the group negotiation power.

Private insurance companies: Major carriers like Delta Dental, Aetna, Cigna, and UnitedHealthcare offer individual dental plans directly. Premiums typically range from $20 to $80 monthly depending on the plan type and your location. I’ve found that requesting quotes from at least three companies helps you understand the price variation in your area. Some companies offer rate locks that guarantee your premium won’t increase for 12 to 24 months.

Spouse’s employer plan: If your spouse has employment income with benefits, adding yourself to their dental plan is often the most affordable option. Family plans usually cost only $15 to $30 more than individual coverage. Ask about dependent coverage options when you’re researching plans.

What’s typically covered under dental insurance

Dental insurance for self employed workers generally covers three categories of care, each with different coverage percentages. Most plans feature waiting periods of 6 to 12 months before covering major services like crowns and root canals, though preventive care is usually available immediately.

Preventive services (100% coverage): This includes two annual cleanings, two annual exams, and annual X-rays. Most plans cover fluoride treatments and sealants for children. These foundational services are covered completely with no co-pay under virtually all plans because insurers know that preventive care saves money long-term.

Basic services (70-80% coverage): These include fillings, extractions, and periodontal treatments. You typically pay 20% to 30% of the cost after any deductible. If you need a filling, most plans cover $100 to $150 of the cost, leaving you responsible for any amount above the plan’s allowance. These services are usually available after a 1 to 6 month waiting period.

Major services (50% coverage): Crowns, bridges, root canals, and implants fall into this category. Plans cover 50% of the approved amount after deductibles. Most plans include annual maximums of $1,000 to $1,500 for all covered services, which can limit your coverage for major work. Orthodontics, when covered, typically pays 50% with lifetime maximums of $1,000 to $2,000.

Calculating your dental insurance costs and benefits

I’ve spent considerable time analyzing the actual costs of different dental insurance for self employed options, and the math is worth doing before you buy. The cheapest monthly premium isn’t always the best value.

Example scenario 1: Routine care only: If you visit the dentist twice yearly for cleanings and exams with no other work, a DHMO plan at $20 monthly costs $240 annually for full coverage. A discount plan at $150 annual membership might seem cheaper, but you should ensure the discount covers your specific dentist. Over a two-year period, DHMO is clearly superior if you’re healthy.

Example scenario 2: One crown needed: Assume you need one crown costing $1,200. With a DPPO plan (premium $40/month, $100 deductible, 50% major coverage), you pay $40 x 12 = $480 in premiums plus $100 deductible plus $600 (50% coinsurance) = $1,180 total. With a discount plan, you pay $150 membership plus $1,200 x 30% discount = $150 + $840 = $990. The discount plan is cheaper in this scenario. However, the DPPO provides coverage protection for additional procedures during the year.

Example scenario 3: Multiple procedures: If you need multiple fillings ($500 total), one crown ($1,200), and annual cleanings, a DPPO plan becomes more valuable. Premium ($480/year) + deductible ($100) + fillings coinsurance ($100) + crown coinsurance ($600) + annual maximum considerations = roughly $1,280. This is often cheaper than paying without insurance when multiple procedures occur in one year.

Tax benefits and deductions for self employed dental insurance

One major advantage of being self-employed is the ability to deduct health insurance premiums, including dental coverage. This tax benefit significantly reduces your true cost of dental insurance for self employed professionals. According to the IRS.gov guidance on self-employed health insurance deduction, you can deduct 100% of your dental insurance premiums as an above-the-line deduction on your federal tax return.

If you pay $50 monthly for dental insurance ($600 annually), and you’re in the 24% tax bracket, that deduction saves you $144 in taxes. Your real out-of-pocket cost is $456, making your effective monthly cost $38 instead of $50. This is a crucial calculation that many self-employed professionals overlook.

You can claim the deduction on Schedule C (Form 1040) if you’re a sole proprietor or on the appropriate schedule if you’re an S-corp or LLC. Keep documentation of all premium payments. You cannot claim this deduction for months when you were covered by an employer plan or your spouse’s plan, so track coverage periods carefully.

Recommended dental insurance providers for self employed professionals

Based on my analysis of dozens of plans and thousands of customer reviews, I recommend comparing quotes from these carriers. Each has particular strengths for self-employed workers.

Delta Dental: The largest dental insurance provider in the United States with the most extensive network. Plans start at $15 monthly for basic DHMO coverage. Delta’s provider network includes over 150,000 dentists, giving you excellent choice even if you relocate. Their online tools for checking coverage and finding providers are particularly user-friendly.

Cigna: Offers competitive pricing with plans ranging from $20 to $70 monthly depending on coverage level. Cigna’s plans often include coverage for more orthodontic care than competitors. Their mobile app for managing claims and finding providers is one of the best in the industry.

Aetna: Provides flexible plan options including some plans with lower deductibles. Aetna plans often feature annual maximums up to $2,000, higher than many competitors. They offer good coverage for periodontal treatment, which is important if you have gum disease risk factors.

UnitedHealthcare: Competitive pricing and nationwide provider networks. Their customer service ratings are consistently high, and they offer several plan tiers to fit different budgets. For self-employed professionals juggling multiple responsibilities, their online claims process is straightforward.

Making the right choice for your dental insurance

After comparing dozens of dental insurance for self employed plans, I’ve found that the right choice depends on your specific situation. Ask yourself these key questions to narrow down your options.

First, what’s your expected dental care needs for the next year? If you know you need significant work, a plan with higher coverage percentages for major services is worth the higher premium. If you’re generally healthy with just routine care needs, DHMO plans offer the best value.

Second, how important is provider choice? If you have a trusted dentist, verify they’re in network before committing to any plan. If you’re open to switching dentists, this gives you more plan options.

Third, what’s your budget for monthly premiums? Be honest about what you can afford. A plan you skip paying because it’s too expensive provides no value. It’s better to choose a lower-cost DHMO with lower co-pays than a comprehensive plan you can’t sustain.

Fourth, when will you need coverage? If you’re planning major work soon, check waiting periods carefully. DHMO plans sometimes waive waiting periods for preventive care but not major services. A plan might be cheap but worthless if you can’t access needed care for six months.

Frequently asked questions about dental insurance

Can I deduct dental insurance premiums on my taxes?

Yes. As a self-employed professional, you can deduct 100% of your dental insurance premiums as an above-the-line deduction on your federal tax return. This deduction is claimed on Schedule C, and it significantly reduces your true out-of-pocket costs. The deduction applies to premiums paid for you, your spouse, and your dependents. For months when you were covered by another employer plan, you cannot claim the deduction for that month.

What’s the waiting period for dental insurance coverage to begin?

Most dental plans start covering preventive services (cleanings, exams, X-rays) immediately with no waiting period. However, basic services like fillings typically have a 1 to 6 month waiting period, and major services like crowns and root canals often have a 6 to 12 month waiting period. Some plans waive these waiting periods if you’re switching from another dental plan. Always ask about waiting periods before enrolling, especially if you have planned dental work.

Can I buy dental insurance as a freelancer if I have no employees?

Yes. You don’t need employees to purchase dental insurance. Individual dental plans are available directly from insurance carriers to any self-employed person. You can also qualify for group plans through professional associations, membership organizations, or the Healthcare.gov marketplace. The Healthcare.gov options may provide subsidies to lower your costs if your income qualifies.

How much does dental insurance typically cost for self employed individuals?

Monthly premiums vary widely depending on plan type and your location. DHMO plans typically cost $15 to $35 monthly. DPPO plans range from $25 to $60 monthly. Indemnity plans cost $40 to $80+ monthly. Discount plans are $80 to $200 annually. After factoring in the tax deduction for self-employed coverage, your actual net cost is typically 20% to 30% lower than the stated premium.

What does a dental plan typically NOT cover?

Most dental plans exclude cosmetic procedures like teeth whitening and smile makeovers. Implants are often not covered or covered at a lower percentage. Orthodontics are frequently excluded unless you buy them as an add-on. Plans also typically won’t cover procedures done before the policy start date or during waiting periods. Some plans exclude certain treatments they consider experimental or unnecessary, which is why reviewing the specific plan documents is crucial.

Is it better to get dental insurance through the healthcare.gov marketplace or directly from an insurance company?

Both options are available to self-employed professionals. Healthcare.gov marketplace plans have the advantage of potentially qualifying you for subsidies if your income falls between 100% and 400% of the federal poverty level, which significantly reduces costs. Direct purchase from insurance companies offers more plan choices and faster enrollment. For most self-employed professionals, comparing both options is worthwhile. Check Healthcare.gov during open enrollment (November through January) to see if you qualify for subsidies before purchasing directly.

Taking action on your dental insurance needs

Protecting your dental health as a self-employed professional doesn’t require settling for expensive plans or going without coverage. By understanding the different types of dental insurance for self employed professionals, calculating your actual costs including tax benefits, and comparing plans from multiple providers, you can find affordable coverage that matches your specific needs.

As part of managing your overall self-employed financial health, consider how dental insurance fits into your broader benefits strategy. Review our guide on self-employed bookkeeping step-by-step guide to ensure you’re tracking healthcare expenses properly. Understanding your tax deductions for self-employed workers helps you calculate your actual insurance costs more accurately. If you’re just starting out, our resource on essential forms for self-employed professionals 2024 covers all the documentation you need for tax purposes including health insurance deductions.

Start by getting quotes from at least three different providers for the plan types that interest you. Input your actual expected dental care needs when requesting quotes, as this helps you see realistic out-of-pocket costs for your specific situation. Most carriers provide detailed quotes online within minutes. Once you’ve gathered your information and done your calculations, you’ll be in an excellent position to choose dental insurance for self employed coverage that protects both your health and your business finances.