As someone who’s researched dozens of disability policies for self-employed clients, I’ve found that disability insurance for self employed workers is one of the most overlooked protections. Most self-employed professionals believe they’re too healthy to ever need it, yet disability statistics tell a different story. If you can’t work, your income stops immediately, and your bills don’t. That’s where disability insurance for self employed income protection becomes essential.

Why self-employed workers need disability insurance

The fundamental challenge of self-employment is income instability without a safety net. Unlike employees who receive short-term disability through their employer, self-employed professionals must create their own protection. In my experience working with freelancers, contractors, and business owners, I’ve seen how quickly a health crisis can become a financial crisis.

Consider this: if you’re injured or become ill and can’t work for six months, who replaces your income? Social Security disability benefits exist, but they’re difficult to qualify for and take months to process. That’s the gap disability insurance for self employed workers fills.

Beyond income replacement, having a solid disability policy protects your business reputation. If you’re forced to turn away clients due to illness, some may not return. Disability insurance for self employed professionals ensures you can honor commitments or communicate professionally about temporary limitations.

Understanding disability insurance types

Short-term vs long-term disability

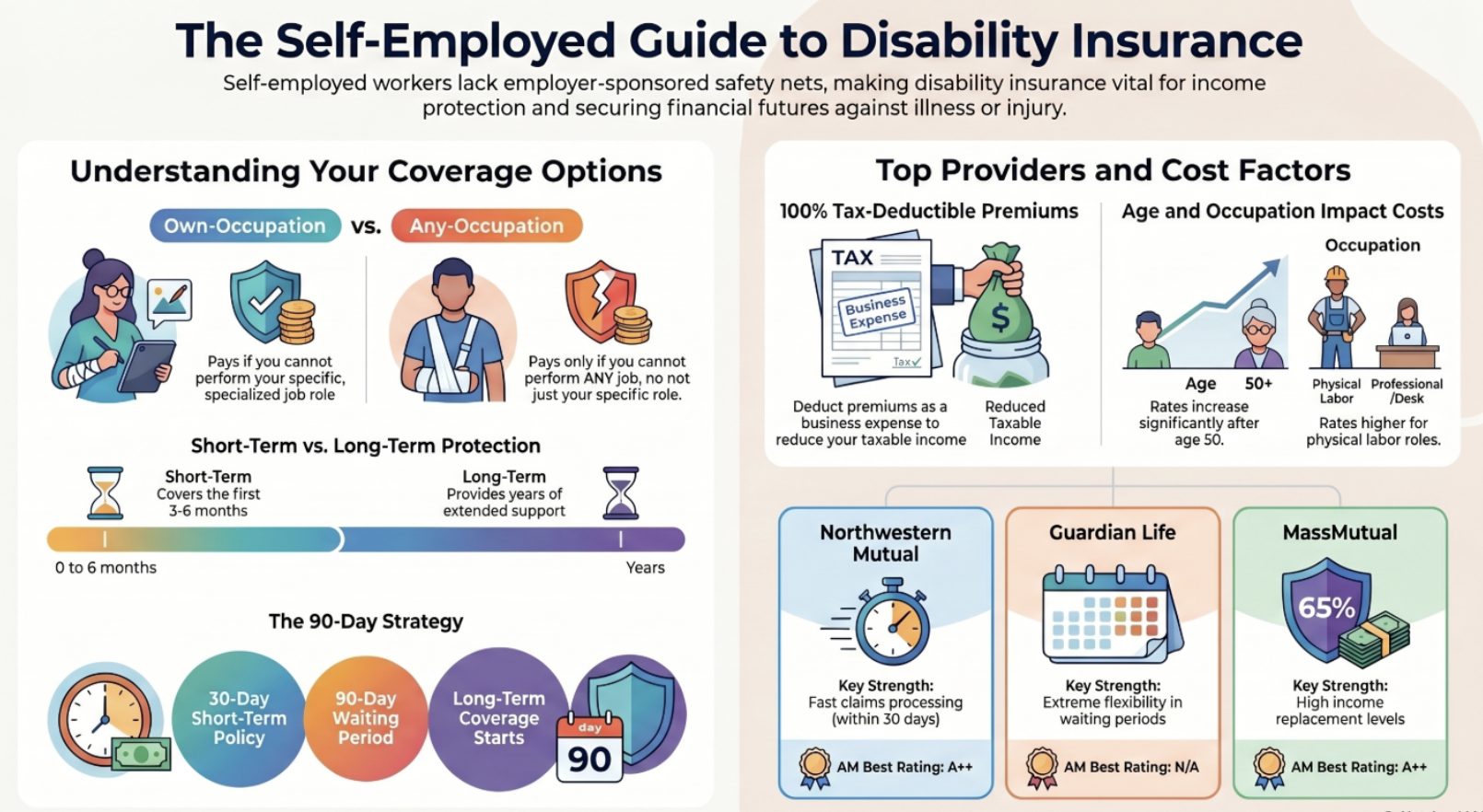

The first decision when selecting disability insurance for self employed needs involves choosing between short-term and long-term coverage, or combining both.

Short-term disability typically covers 3 to 6 months of benefits. The waiting period (called the elimination period) is usually 14 to 30 days. In my experience, short-term policies help bridge the gap during recovery from surgery or acute illness. The premiums are lower, making them affordable for most self-employed individuals.

Long-term disability provides benefits for years, sometimes until age 65. The elimination period is typically 90 days or longer. If you’re concerned about a serious condition that prevents work for an extended period, long-term disability insurance for self employed income protection is crucial. These policies cost more but offer comprehensive protection.

Many self-employed professionals opt for both. A 30-day short-term policy bridges the gap while long-term coverage activates at 90 days. This combination approach maximizes protection without excessive premium costs.

Own-occupation vs any-occupation coverage

This distinction matters significantly for self-employed workers choosing disability insurance. Own-occupation coverage pays benefits if you can’t perform your specific job. Any-occupation coverage only pays if you can’t work in any job for which you’re reasonably qualified.

For disability insurance for self employed professionals, own-occupation coverage is preferable. If you’re a consultant who becomes unable to do client work due to hearing loss, own-occupation pays benefits even if you could theoretically do other work. Any-occupation policies are cheaper but less protective.

Top disability insurance providers for self-employed workers

Northwestern Mutual disability insurance

Northwestern Mutual has long been a trusted choice for disability insurance for self employed individuals. The company, founded in 1859, brings credibility and financial strength to the table. Their A++ rating from AM Best reflects stability that matters when you need benefits decades later.

Northwestern Mutual specializes in customizable plans. You control the elimination period, benefit period, and income replacement percentage. Their claims process is documented to move quickly, with decisions typically within 30 days. For high-income self-employed professionals, Northwestern Mutual offers competitive rates on disability insurance for self employed income protection.

Guardian Life disability insurance

Guardian has been in business since 1860 and understands the needs of self-employed workers. Their disability insurance for self employed clients offers exceptional flexibility in design.

What sets Guardian apart is the range of waiting periods available: 30, 60, 90, 180, 360, or 720 days. Your benefit period can be 2 years, 5 years, 10 years, or extend until age 65, 67, or 70. They offer multiple riders including automatic benefit increases and cost-of-living adjustments. If you’re in a professional field with increasing income, these riders on disability insurance for self employed needs make sense.

MassMutual disability insurance

MassMutual, established in 1851, brings over 170 years of insurance experience. Their A++ AM Best rating ensures financial stability for long-term disability commitments.

MassMutual’s strength lies in high income replacement. Their policies offer up to 65% income replacement, among the highest in the industry. For disability insurance for self employed professionals earning substantial incomes, this coverage level is appealing. Their customizable riders let you add automatic benefit increases and catastrophic disability coverage. The drawback is they require agent interaction rather than online quotes, which some self-employed workers find inconvenient.

Principal Life Insurance

Principal has been serving self-employed workers since 1879. Their disability insurance for self employed clients emphasizes affordability without sacrificing coverage quality.

Principal’s policies are available with various elimination periods and benefit periods. They’re known for reasonable premiums relative to coverage. For cost-conscious self-employed professionals, Principal’s disability insurance for self employed needs often provides good value. Their underwriting process is relatively quick, allowing policies to activate within weeks.

How to choose disability insurance for self-employed needs

Selecting the right policy requires honest assessment of your situation. Start by calculating your monthly expenses. If you earn $5,000 monthly but spend $3,500, you need to replace at least that amount during disability.

Next, consider your emergency fund. If you have six months of expenses saved, you might choose a 90-day elimination period on disability insurance for self employed income protection. If you have minimal savings, a 30-day period provides faster benefit payments.

Evaluate your industry risk. Consultants working from a desk face different disability risks than contractors doing physical work. Own-occupation coverage matters more for specialized professionals where recovery might allow some work but not your specific field.

Review your other income sources. Do you have rental income, investments, or a spouse’s income? Disability insurance for self employed workers should protect your primary income source while considering other resources. You typically can’t get disability insurance for self employed that exceeds 65% of your average income—insurance companies want to prevent over-insuring.

Cost factors for disability insurance for self-employed workers

Premiums depend on several factors. Your age matters significantly. At 30, disability insurance for self employed workers costs roughly $30 to $50 monthly for $2,000 in monthly benefits. At 50, the same coverage costs $80 to $150 monthly.

Your occupation affects pricing. White-collar professionals get better rates than laborers. Your health history matters too. If you have diabetes or high blood pressure, disability insurance for self employed applicants typically costs 20 to 50 percent more.

Policy design choices impact cost. A 90-day elimination period on disability insurance for self employed coverage costs less than a 30-day period. Longer benefit periods cost more. Own-occupation coverage costs more than any-occupation. Monthly benefits of $1,000 cost far less than $5,000 monthly benefits.

The good news: disability insurance for self employed individuals is tax-deductible as a business expense. If you pay $500 annually, you reduce your taxable income by that amount, effectively reducing your true cost through tax savings.

Common questions about disability insurance for self-employed professionals

What counts as disability for self-employed workers?

A disability must prevent you from performing your occupation (under own-occupation policies) or any occupation (under any-occupation policies). This includes illnesses like cancer or heart disease, injuries from accidents, or surgeries with long recovery periods. Mental health conditions and pregnancy-related disabilities also qualify under most disability insurance for self employed policies.

How long does it take to receive benefits?

After you file a claim, most disability insurance for self employed providers take 30 to 60 days to approve or deny. Once approved, benefits begin after your elimination period expires. If you chose a 90-day elimination period, you wait 90 days from disability start date before receiving payments, regardless of how long approval takes.

Can I get disability insurance if I have a pre-existing condition?

Yes, but your premiums will be higher. When applying for disability insurance for self employed coverage, insurers ask detailed health questions. Pre-existing conditions increase risk, so they increase premiums. Some conditions may result in exclusions (like if you have a history of depression, mental health disabilities might be excluded). Underwriting varies by insurer, so shop with multiple companies when you have health concerns.

What happens to my disability insurance if my income changes?

Most disability insurance for self employed workers can be adjusted when income changes significantly. If your business grows 50 percent, you can typically increase your benefit amount. Conversely, if business contracts, you can reduce coverage. Some policies have annual increase riders that automatically increase benefits by a set percentage annually to keep pace with inflation.

Does disability insurance for self employed workers cover temporary disability?

Yes, that’s exactly what short-term disability insurance for self employed workers provides. Short-term policies cover temporary disabilities lasting weeks to months. Long-term policies take over if disability extends beyond the initial period. Many self-employed professionals maintain both to maximize protection during recovery periods.

How do I apply for disability insurance if I’m self-employed?

Contact insurance brokers who specialize in self-employed coverage. You’ll provide tax returns proving income, complete health questionnaires, and specify your desired coverage. Many insurers require APS (Attending Physician Statement) if you’ve had recent health issues. The application process typically takes 4 to 8 weeks, though some companies expedite it.

Can I deduct disability insurance premiums as a business expense?

Yes. Disability insurance for self employed workers qualifies as a business deduction. You report premiums on Schedule C (Form 1040) under business expenses. This reduces your adjusted gross income and your self-employment tax. Consult your tax professional about properly documenting this deduction for your specific business structure.

What if I’m denied disability insurance for self employed coverage?

If denied, request the insurer’s explanation in writing. You can appeal, provide additional medical records, or ask about modified policies with higher premiums or lower benefit amounts. You might also try other insurers, as underwriting standards vary. Working with a broker who specializes in disability insurance for self employed workers with health issues increases approval odds.

Taking action on disability insurance for self-employed protection

Protecting your income deserves the same attention you give to protecting your home or car. Disability insurance for self employed professionals fills a critical gap in your financial protection strategy. The cost is modest compared to the risk of losing your entire income.

Start by calculating your monthly expenses and desired benefit amount. Contact 3 to 5 insurers specializing in disability insurance for self employed workers. Get quotes for both short-term and long-term coverage. Compare own-occupation versus any-occupation options.

Review the policies carefully before signing. Understand the elimination period, benefit period, and riders included. Ask about non-cancellable and guaranteed renewable provisions, which lock in your rates and prevent cancellation.

For additional information on managing your self-employed finances, check out our comprehensive guides on self-employed bookkeeping, essential forms for self-employed professionals, and California self-employment taxes. You might also explore options for self-employed pension plans and self-employment ideas for income diversification.

For official information on disability benefits, the Social Security Administration’s disability benefits page explains government support options. The U.S. Small Business Administration’s disability insurance guidance provides additional context for self-employed business owners.

Your ability to work is your most valuable asset as a self-employed professional. Protecting it with adequate disability insurance for self employed income protection is one of the wisest investments you can make.