Hi, I’m Elliot from Selfemployed.com, and I’ve spent the better part of two decades helping self-employed professionals and gig workers navigate the financial landscape. Emergency expenses don’t wait for steady paychecks, and I’ve seen firsthand how critical quick cash solutions are when you’re managing your own business. In this guide, I’m sharing what you need to know about emergency cash advances in 2026 to get the fast funding you need without breaking the bank.

When unexpected costs pop up, self-employed individuals face a unique challenge. You can’t simply ask your employer for an advance, and traditional banks often move too slowly. Emergency cash advances fill that gap, offering funds within hours rather than weeks. The key is understanding your options and choosing the right fit for your situation.

## Understanding Cash Advances for Self-Employed Professionals

A cash advance is fundamentally different from a traditional loan. Instead of borrowing against your creditworthiness, you’re borrowing against your future earnings or revenue. This distinction matters because it opens doors for self-employed professionals who might struggle with conventional lending due to income variability.

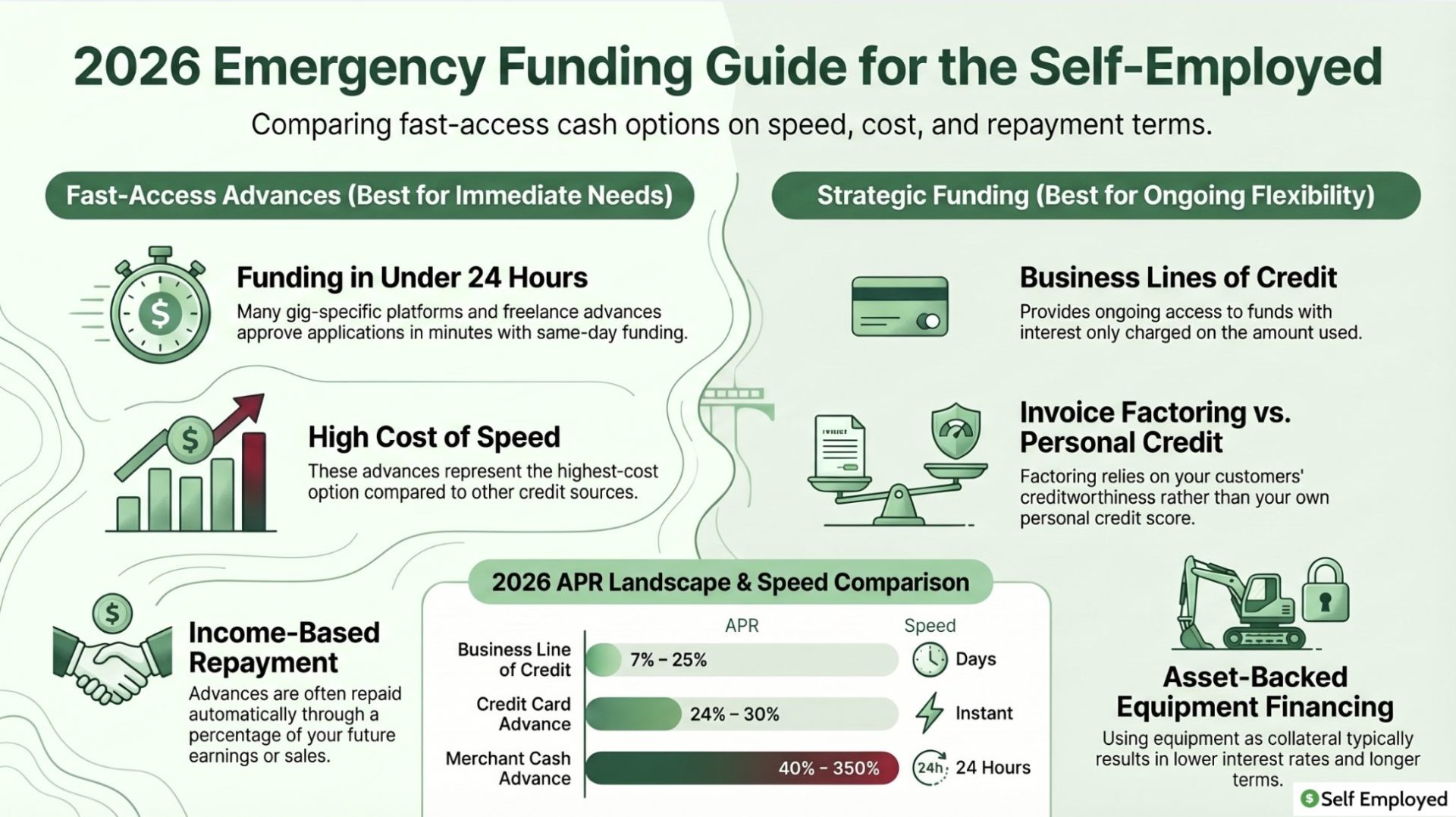

The appeal is straightforward: speed. Many platforms approve applications in minutes and fund accounts within 24 hours. You’ll typically find that qualification requirements are more forgiving than traditional loans, which is especially valuable if your credit score isn’t perfect or your income documentation is complex.

However, this speed and accessibility comes with trade-offs. Interest rates and fees are generally higher than traditional loans. As of 2026, merchant cash advances carry APRs ranging from 40% to 350%, depending on the provider and your repayment terms. Credit card cash advances typically fall between 24% and 30% APR.

## Freelance Cash Advances and Income-Based Funding

If you’re a freelancer or contractor, income-based cash advances are designed specifically for your situation. These products let you access money based on your pipeline of future work or invoices. Many allow borrowing up to $20,000, with repayment automatically deducted from future client payments.

The process is remarkably simple. You complete an online application, get approved in minutes, and see funds hit your account within 24 hours. Because repayment is tied to your actual earnings, there’s no rigid monthly payment schedule that could stress your cash flow during lean months.

What makes this especially valuable is the flexibility around income verification. Unlike traditional loans requiring two years of tax returns, platforms accepting freelancers often only need your bank statements from the last few months or documentation of client contracts.

## Merchant Cash Advances for Business Owners

If you run a business that processes credit card payments, merchant cash advances offer another route. You receive a lump sum upfront, and repayment comes from a percentage of your daily or weekly card sales.

The advantage is that your repayment adjusts naturally with your revenue. Slow month? You pay less. Strong month? You pay more. This flexibility can be crucial for seasonal businesses or those with unpredictable cash flow.

The significant drawback is cost. As I mentioned, APRs regularly exceed 100%, sometimes reaching 350%. These are genuinely expensive funds, and I typically recommend exploring other options first. Use merchant cash advances only when time is critical and alternatives simply aren’t available.

## Business Lines of Credit: A Flexible Safety Net

Unlike one-time cash advances, a business line of credit provides ongoing access to funds. You establish a credit limit—perhaps $10,000 to $50,000—and draw only what you need. You pay interest only on the amount you’ve actually used.

This makes lines of credit ideal for managing cash flow fluctuations throughout the year. During slow periods, you draw what you need. When revenue picks up, you pay it back and rebuild your available credit. Many lines of credit charge between 7% and 25% APR, making them more affordable than merchant cash advances while still less competitive than standard personal loans.

Approval typically requires showing your business bank statements and basic financial documentation. Two years of business operation is the general standard, though some lenders are flexible with established freelancers or contractors with strong income history.

## Personal Loans and Equipment Financing Options

For larger purchases or longer repayment timelines, personal loans offer stability through fixed rates and predictable monthly payments. Current APRs for personal loans range from 5.99% to 35.99%, with approval typically requiring a credit score above 620.

Equipment financing deserves special attention if you need business tools or vehicles. Rather than draining cash reserves, you finance the equipment itself, which serves as collateral. This arrangement often results in lower rates since the lender has a tangible asset to recover if things go wrong. Many programs allow financing up to $5 million and offer flexible terms spanning three to five years.

Both options typically require personal guarantees from business owners, meaning you’re personally responsible if the business can’t pay. Before committing, make sure you’re comfortable with that obligation.

## Short-Term Loans: Quick Solutions for Immediate Needs

Short-term loans bridge the gap between cash advances and traditional financing. Typically repaid within six to twelve months, these loans offer faster approval than conventional products while maintaining lower rates than merchant cash advances.

You can usually borrow between $1,000 and $50,000, depending on the lender and your financial profile. Interest rates vary widely based on credit score and lender type. Online lenders often provide the fastest turnaround, sometimes funding within 24 hours of approval.

The trade-off is higher rates compared to longer-term products. For comparison, traditional personal loans at five-year terms might carry 10% APR, while a one-year loan could exceed 20%. That said, if your emergency is temporary and you’ll resolve it within months, the higher cost might be worth it for the peace of mind.

## SBA Loans: Government-Backed Stability

Small Business Administration loans offer another layer of security. Because the government backs these loans, lenders can afford to be more flexible with approval criteria. Many borrowers with credit scores as low as 600 qualify, provided they meet other requirements.

Typical SBA loan requirements include a minimum credit score of 600, at least three years in business, and monthly revenue of at least $10,000. Interest rates are generally favorable—often between 7% and 10%—and you can borrow up to $2 million for disaster scenarios or standard working capital needs.

The downside is the application process. SBA loans require extensive documentation and can take two to three months to close. This isn’t a solution for same-day cash needs, but if you can wait a few weeks and want truly affordable long-term funding, SBA loans are hard to beat.

## Invoice Factoring and Accounts Receivable Solutions

If your business regularly extends credit to clients, your unpaid invoices represent real value. Invoice factoring companies purchase these invoices at a discount, giving you immediate cash. Once customers pay, you receive the remainder minus the factoring fee.

This approach offers a critical advantage: qualification focuses on your customers’ creditworthiness, not your personal credit. Many factoring services approve applications with limited requirements and fund within 24 to 48 hours. Factoring fees typically run 2% to 5% of invoice value, depending on the factor’s risk assessment and payment terms.

The ideal scenario is factoring invoices from established clients with reliable payment histories. Be cautious about factoring invoices from new or questionable customers, as fees will be higher and the lender might reject them entirely.

## Earned Wage Access and Gig Economy Solutions

For gig workers and those in the sharing economy, earned wage access represents an emerging category. These platforms let you access a portion of your earnings before your official payout day—sometimes just hours after completing work.

As of 2026, platforms specifically designed for freelancers, contractors, online sellers, and gig workers often have no minimum credit score requirements and can qualify you with just three months of work history. Costs are typically modest compared to traditional cash advances—often $2 to $3 per withdrawal rather than interest-based charges.

These solutions work exceptionally well for managing the irregular timing of gig income. They reduce the stress of waiting days or weeks for payment while your bills are due now.

## Comparing Your Emergency Cash Advance Options

Choosing the right emergency funding starts with understanding your situation. Ask yourself: How much do I need? How quickly? How long can I take to repay?

For immediate needs under $500 within 24 hours, gig-specific cash apps are your best bet. For $1,000 to $5,000 within days, freelance income-based advances work well. For $5,000 to $20,000 with moderate flexibility, personal loans or business lines of credit make sense. For larger amounts or ongoing access, equipment financing or short-term business loans fit better.

Always compare APRs directly. A merchant cash advance showing a 1.5 factor rate translates to roughly 150% APR annually, which is dramatically more expensive than a personal loan at 15% APR even if the initial dollar amount feels smaller.

## Building Long-Term Financial Stability

While emergency cash advances solve immediate problems, they’re not a sustainable long-term strategy. Self-employed professionals benefit most from developing steady cash reserves and diverse funding relationships.

Start building an emergency fund covering three to six months of expenses. At the same time, establish credit lines before you need them. Lenders are more willing to approve credit lines when you don’t desperately need the money. This proactive approach gives you options when true emergencies arrive.

Keep your credit score healthy by paying bills on time, keeping credit card balances low, and monitoring your credit report for errors. A credit score above 700 opens doors to better rates across all lending products.

## Making Your Emergency Cash Advance Decision

Emergency cash advances serve a genuine purpose in the self-employed toolkit. They bridge gaps created by irregular income and unexpected expenses. The key is using them strategically while building systems and relationships that gradually reduce your dependence on emergency funding.

When you do need emergency cash, you now understand your options. Choose the solution that balances speed, cost, and flexibility for your specific situation. And remember: the best emergency fund is the one you never need to use.

## Frequently Asked Questions

What is the difference between a cash advance and a loan?

A cash advance is typically repaid from future earnings or revenue, while a loan is repaid through set monthly payments. Cash advances are often faster to obtain but usually more expensive.

Can I get a cash advance if I have poor credit?

Yes. Many cash advance options specifically for freelancers and gig workers don’t require strong credit scores. Approval often depends on your recent income history instead.

How quickly can I get emergency funding?

Many cash advances fund within 24 hours of approval. Some gig economy platforms can provide funds within hours. SBA loans typically take 2-3 months.

What’s the average APR for emergency cash advances in 2026?

Rates vary widely. Credit card advances run 24-30% APR, merchant cash advances 40-350% APR, while personal loans typically range 5.99-35.99% APR.

Should I use merchant cash advances if I run a business?

Only as a last resort. While flexible, merchant cash advances are expensive. Explore business lines of credit, equipment financing, or SBA loans first for better rates.

How can I prepare for emergencies before they happen?

Build an emergency fund covering 3-6 months of expenses, establish credit lines before you need them, and maintain a credit score above 700.