I remember trying to buy a home while juggling 1099s, irregular invoices, and a modest savings account. I wasn’t short on income, but proving it felt like a second job. My goal was simple: lock a fair loan without draining cash needed for taxes and slow months. I wanted low fees, clear docs, and a lender who “gets” variable pay. I spoke with loan officers, dug into fee sheets, and compared preapprovals. A few lenders were great with W-2s, then froze when I mentioned K-1s and write-offs.

What finally clicked was this: the best lenders for self-employed folks make underwriting easier, not harder. They lean on bank statements, CPA letters, and smart income analysis. I also learned you don’t need the fanciest product to win. Fee transparency, rate locks that fit your timeline, and access to down payment help can beat a flashy ad.

Comparison of 7 best mortgage lenders in 2026 with pricing and recommended use cases

What is a mortgage lender?

A mortgage lender is a financial services company or credit union that approves, funds, and services home loans. Its core job is to evaluate risk and issue a mortgage you can repay.

In lending, the saying “cash is king” translates to “proof is king.” The right lender helps self-employed borrowers turn variable income into a clear, documented story that qualifies for financing.

For example, qualifying with a lender skilled at analyzing bank statements can turn a denied file into an approval with the same income. That difference can be worth tens of thousands over the life of a loan compared with renting longer.

The core purpose is simple: lenders help buyers, including freelancers and business owners, submit documents, verify income/assets from tax returns or statements, and close on a loan that fits their monthly cash flow.

Borrowers often pair the lender’s work with a realtor, a housing counselor, and sometimes a down payment assistance program or grant from state and local agencies. A good CPA can also help present income accurately.

Not every lender handles self-employment the same way, so choosing carefully can save real money and weeks of stress.

How to choose the best mortgage lender

Picking a lender can feel overwhelming. There are banks, credit unions, online lenders, and brokers, all claiming to offer the best rates and the fastest closing.

I wrote this specifically to help self-employed readers match with lenders that respect variable income and protect tight budgets.

Most lists you’ll find are written by lenders or sites that rank sponsors higher. I am not sponsored by any platform on this list. This is a straight, honest take based on my research and hands-on experience advising self-employed buyers.

Here are some questions you should ask when looking for a lender:

- What lender fees apply, and can any be waived or credited?

- How do they calculate self-employed income (bank statements, CPA letters, average over 12–24 months)?

- Do they support low-down payment programs and down payment assistance?

- How fast and clear is preapproval, and is it a hard pull?

- What happens to costs as the loan amount or points change?

- What disclosures and loan estimates will I get, and how soon?

- How strong is their communication during underwriting and at closing?

- If I need to switch lenders, how tough is it to transfer the appraisal or restart?

- Do they service the loan after closing, and what are the support hours?

It’s a lot to weigh, but my ranked picks below address these points with real tradeoffs, not marketing fluff.

Okay, enough of me rambling, let’s get into the list.

7 best mortgage lenders in 2026

Here are my top picks for the best mortgage lenders:

- Better Mortgage

- Rocket Mortgage

- Guild Mortgage

- New American Funding

- Guaranteed Rate

- Navy Federal Credit Union

- Angel Oak Home Loans

Let’s see which one is right for you.

1. Better Mortgage

Better Mortgage is a digital-first lender focused on fee transparency and speed. It’s known for promoting $0 lender fees on many loans and a fast online process from preapproval to close.

You can start with an online preapproval in minutes. The dashboard walks you through docs, asset verification, and disclosures. Daily tasks include uploading bank statements, e-signing forms, and comparing rate-and-point options in real time.

In recent years, Better has added more tools for digital verification and streamlined rate locks. That helps self-employed borrowers move quickly when a clean contract comes in, even if income is less straightforward.

For higher-complexity files, Better offers options such as extended rate locks and lender credits (when available) to offset third-party costs. It also pairs borrowers with loan consultants who focus on scenario planning.

I like Better for tight-budget shoppers who want clear numbers without haggling over junk fees. The online experience reduces back-and-forth and keeps your timeline on track.

Support is responsive via phone, chat, and email, and the disclosures are easy to read. That matters when you’re juggling clients, taxes, and a purchase deadline.

How Better Mortgage works and key features

Better centers everything in a clean web portal. You’ll see your loan estimate, rate options, and document checklist in one place. Templates guide uploads for tax returns, K-1s, or bank statements if needed.

Advanced users can toggle points, lock lengths, and compare scenarios before committing. Integrations help quickly verify assets and credit. Analytics show your rate and fee breakdown so you can spot savings by adjusting credits or points.

Automations ping you about missing docs, and closing timelines update as milestones are cleared. Better also offers resources on appraisal, title, and homeowners’ insurance so you can plan cash needs.

Support is available by chat and phone during extended hours. The overall feel is beginner-friendly with enough control for detail-minded buyers.

Who Better Mortgage is for

Best for freelancers, solo LLC owners, consultants, online creators, and gig workers who want low lender fees and fast preapproval. It works well for purchase loans under tight timelines and simple to moderate self-employment setups. If you need niche non-QM products or extensive manual underwriting, a specialty lender may be a better fit. No great technical skill needed—just be organized with docs.

Better Mortgage pricing

Better’s pricing model highlights $0 lender fees on many loans, which can cut hundreds to thousands from closing costs. You still pay third-party costs like appraisal, title, and prepaid items.

- Conventional Purchase: $0 lender fees on many loans; low down options where eligible; standard rate-and-point choices

- FHA: Low down payment; mortgage insurance applies; lender fees often $0 from Better

- Jumbo: Higher loan amounts; pricing depends on credit and reserves; rate locks available

Compared with peers, $0 lender fees can be strong value if your rate is competitive. Annual savings don’t apply here, but locking strategy and lender credits can shift costs. Always compare a written Loan Estimate across at least two lenders.

Pros and cons of Better Mortgage

Pros

- $0 lender fees on many loans keeps cash to close lower

- Fast online preapproval and clear disclosures

- Easy to compare points vs. credits inside the portal

- Responsive support for document checklists

Cons

- Not a fit for complex non-QM or niche income cases

- No branch network for face-to-face help

- Rates vary daily—always compare written quotes

If you want low fees and a clean digital process, start here. If you need bank-statement underwriting or unusual credit, consider a specialty lender.

Better Mortgage reviews

Public review scores vary by time period and platform. Check recent borrower feedback on Trustpilot and Google for current sentiment, as online lenders often see wide swings during busy markets.

2. Rocket Mortgage

Rocket Mortgage is an all-digital lender known for speed and a polished app. Backed by one of the largest mortgage companies in the U.S., it brings scale, support, and clear workflows.

You can get an online preapproval quickly and manage everything in the app. The interface guides document uploads, credit pulls, and e-signatures. Day to day, you’ll adjust rate options, respond to underwriter notes, and track milestones.

Rocket has invested in income analysis tools that interpret tax returns and variable income. That’s helpful if you write off expenses and need a consistent picture of cash flow.

Advanced options include extended locks, appraisal waivers when eligible, and programs for low down payments. Its servicing arm also keeps many loans after closing, which can simplify life later.

I’ve had positive experiences with Rocket’s communication cadence. The app nudges you at the right moments, and loan officers are reachable when things get urgent.

Design and support are standouts. If you like seeing every step and getting quick answers, Rocket checks those boxes.

How Rocket Mortgage works and key features

Rocket uses a mobile-first dashboard with a guided checklist. Templates cover W-2, 1099, K-1, and corporate returns. You can fine-tune points and compare monthly payment changes by slider.

Integrations pull in bank data to verify assets. Reporting shows cash to close, prepaid items, and how credits affect totals. Automations flag missing pages or signatures.

Extra tools include calculators, education on mortgage insurance, and refinance scenarios for later. Support is available by phone, chat, and secure messages.

The experience is friendly for first-timers but deep enough for complex files. It balances clarity and control well.

Who Rocket Mortgage is for

Great for self-employed buyers who want speed, a strong app, and steady guidance. Consultants, agency owners, rideshare drivers, and e-commerce sellers fit well. If you need non-QM bank statement loans, look to a specialist. Tech skill isn’t required—just comfort using a mobile app.

Rocket Mortgage pricing

Rocket doesn’t charge an application fee for most loans. Total costs include lender fees (which vary), third-party fees, and any points you choose to pay or credits you receive.

- Conventional: Low down options; standard lender fees; rate-and-point choices

- FHA/VA: Low or $0 down paths where eligible; mortgage insurance or funding fee rules apply

- Jumbo: Competitive for strong credit; extended locks available

Value is usually solid for the tech and support. Always compare Loan Estimates from the same day across lenders, since daily pricing can change the totals more than fees alone.

Pros and cons of Rocket Mortgage

Pros

- Excellent app and clear milestone tracking

- Helpful income analysis for self-employed files

- Strong servicing experience after closing

- Reliable support during busy periods

Cons

- Lender fees vary—get a same-day comparison

- Not a pure fee-free model

- Non-QM options limited compared to specialists

If you want speed and guidance with typical self-employed docs, Rocket is a top pick. For edge-case income, pair with a specialist quote.

Rocket Mortgage reviews

Independent ratings vary by source and time. Check recent borrower feedback from Google and J.D. Power studies to identify service trends during your shopping window.

3. Guild Mortgage

Guild Mortgage is a full-service lender with deep experience in first-time buyer programs and down payment assistance. Its branch network and local know-how help self-employed buyers stretch cash.

You can start online or through a loan officer. The process is traditional but organized: preapproval, disclosures, underwriting, and closing, with assistance with DPA paperwork where available.

Guild tracks state and local grants and often partners with housing agencies. That matters when every dollar of cash to close counts.

Higher-tier options include extended locks, renovation loans, and tailored underwriting support. Guild’s manual touch can be helpful for nuanced income stories.

I like Guild for buyers who want hands-on help with subsidies and grants. Team members know which programs pair with FHA, conventional, or USDA loans.

Branch-level service is a plus. If you prefer in-person conversations and a lender who knows local programs, Guild stands out.

How Guild Mortgage works and key features

Guild combines an online portal with branch support. You’ll upload tax returns and bank statements, then work with your officer on income calculations. Templates and checklists keep docs tidy.

Customization comes from pairing the right loan with DPA programs. Reporting shows cash-to-close and how grants affect your bottom line. Automations handle disclosures and status updates.

Guild also offers renovation and USDA loans, which some competitors skip. Support is available by phone, email, and in person.

Overall, it’s friendly for first-timers and helpful for complex local program stacking. Not the flashiest tech, but strong results for budget-minded buyers.

Who Guild Mortgage is for

Best for self-employed first-time buyers, gig workers, tradespeople, and small business owners who want down payment help. Great for buyers in states with strong grant programs. If you want a pure online flow, this may feel slower, but the guidance can save money. Minimal technical skill required.

Guild Mortgage pricing

Guild’s costs depend on loan type, market pricing, and local fees. Many borrowers combine low-down-payment options with grants to reduce cash-to-close.

- Conventional: 3% down options where eligible; lender fees vary by branch

- FHA/USDA: Low down or $0 down with program rules; mortgage insurance applies

- Renovation/Other: 203(k) and similar; longer timelines; fees vary

Compared with online-only lenders, fees can be similar once grants are applied. The main value is access to DPA and hands-on guidance. Always compare a same-day Loan Estimate.

Pros and cons of Guild Mortgage

Pros

- Strong access to down payment assistance and grants

- Hands-on support for income documentation

- Wide product menu, including USDA and renovation loans

Cons

- Tech feels slower than top online lenders

- Branch-based fees and timelines can vary

- Not ideal if you want a fully self-serve experience

If stacking programs and lowering cash to close is key, Guild is a smart pick. Rate hawks who want instant online changes may prefer a digital lender.

Guild Mortgage reviews

Reviews vary by local branch. Check recent Google ratings for your branch and ask your officer for references tied to self-employed closings in your market.

4. New American Funding

New American Funding is a direct lender with a reputation for hands-on underwriting and bilingual support. It’s known for helping borrowers who need careful income review.

You can start online or with a loan officer. The portal is straightforward for uploads, and teams help gather CPA letters, profit-and-loss statements, and explanations when needed.

Recent process improvements have focused on faster turn times and better communication. That helps self-employed borrowers move through underwriting without guesswork.

On the premium side, New American offers extended locks and a broad loan menu. Manual attention to income trends can make the difference for borderline files.

I’ve seen good results with borrowers who had write-offs that other lenders had confused. Careful documentation and a patient officer helped them close.

Support quality is a strength. If you value human review more than flashy tech, this is a good match.

How New American Funding works and key features

The interface is simple: checklist, uploads, and e-sign. Templates for K-1s, 1120-S, and Schedule C guide the process. Officers walk you through sourcing bank statements and drafting letters of explanation.

Customization comes from pairing the right program with your income pattern. Status updates and closing timelines are clear. You’ll get help modeling points vs. credits to manage cash to close.

Support is available by phone and email with bilingual teams. The overall experience favors thoroughness and clarity over speed-at-all-costs.

It’s beginner-friendly and thoughtful for complex self-employed files.

Who New American Funding is for

Best for freelancers, small business owners, trades, rideshare drivers, and multi-income households needing a detailed review. Good for first-time buyers who want help balancing points, credits, and monthly payments. If you want instant online approvals and zero hand-holding, look elsewhere. Minimal tech skills needed.

New American Funding pricing

Costs vary by product, market, and file complexity. Expect standard lender fees plus third-party charges, with room to use credits to lower cash at close.

- Conventional: 3%–5% down, where eligible; lender fees vary

- FHA/VA: Low or $0 down paths; program rules and insurance/funding fees apply

- Jumbo/Other: Pricing tied to credit, reserves, and property type

Value is strongest for borrowers who need careful underwriting to qualify. Always compare a same-day Loan Estimate to check fees and rate against peers.

Pros and cons of New American Funding

Pros

- Thorough self-employed income review

- Bilingual support and patient guidance

- Clear modeling of points and credits

Cons

- Online tools are solid but not top-tier

- Timelines depend on documentation speed

- Fees vary—must compare written quotes

If you need a careful read of complex income, this is a strong choice. Pure rate chasers might prefer a larger online lender for speed.

New American Funding reviews

Public reviews can vary by branch and time. Look up recent Google ratings for your local office and ask for recent references from self-employed buyers.

5. Guaranteed Rate

Guaranteed Rate blends a tech-forward experience with a large product menu. Its “Same Day Mortgage” offering often helps qualified buyers move quickly from application to approval.

The interface is modern and clear. You can upload docs, tweak points, and track progress online while working with a loan officer on edge cases.

Recent pushes on speed and digital underwriting have made it more appealing to self-employed borrowers who want quick answers without sacrificing options.

Premium features include extended locks and a range of low-down-payment paths. Branch support can step in when income needs manual review.

I like Guaranteed Rate for rate shoppers who still want guidance. The balance of speed and service works well for clean to moderately complex files.

Education resources help you plan cash to close and compare structures. That’s valuable when every dollar matters.

How Guaranteed Rate works and key features

You’ll use a guided online portal with smart checklists. Templates flag missing pages, and calculators model payment changes when you adjust points or credits.

Advanced users can explore lock terms and program options. Integrations help verify assets and credit promptly. Reporting keeps you current on cash to close and conditions.

Automation speeds approvals, while loan officers manage manual reviews. Support is available by phone and chat, with branch help when needed.

Overall, it’s a strong blend of speed and hand-holding—good for beginners and pros.

Who Guaranteed Rate is for

Best for self-employed buyers who want quick turnarounds and competitive pricing. Good fit for consultants, agency owners, and contractors with organized books. If you need non-QM bank-statement loans, consider a specialist. Comfort with online tools helps, but isn’t required.

Guaranteed Rate pricing

Pricing includes standard lender fees, third-party fees, and optional points. Down payment and mortgage insurance rules depend on the program.

- Conventional: Low down options; lender fees vary

- FHA/VA/USDA: Program-driven costs; low or $0 down paths

- Jumbo/Other: Competitive for strong credit; extended locks available

Relative value is strong for borrowers who want speed plus choice. Always compare written Loan Estimates the same day to capture a fair rate-and-fee snapshot.

Pros and cons of Guaranteed Rate

Pros

- Fast digital approvals in many cases

- Clear pricing tools and calculators

- Large product menu for various profiles

Cons

- Lender fees vary; must compare

- Non-QM options are limited in-house

- Experience can differ by branch/loan officer

If you want quick movement and solid rates, it’s a contender. If you need flexible documentation beyond agency guidelines, consider a non-QM lender.

Guaranteed Rate reviews

Ratings differ by branch and time. Check current Google reviews for your local team and recent borrower stories from self-employed clients.

6. Navy Federal Credit Union

Navy Federal Credit Union serves eligible members of the military community and their families. It’s known for low fees, strong service, and member-focused programs.

You’ll apply online or at a branch. The process is member-first, with guidance for VA loans and other options. Docs are handled through a secure portal with clear checklists.

Recent tech upgrades have improved online status tracking. For self-employed VA borrowers, experienced staff can explain how residual income and guidelines work.

Premium value comes from $0 down VA loans and no PMI on some products. For tight budgets, that can free up cash each month.

I like Navy Federal for eligible buyers who want predictable fees and service. Membership rules apply, but the savings can be real.

Support is easy to reach, and post-closing service is a strong suit.

How Navy Federal works and key features

The portal manages docs, disclosures, and messages. Templates for self-employed income help you upload the right returns and statements. Officers guide VA specifics and alternative programs if VA isn’t a fit.

Tools include calculators and clear cash-to-close views. Automations remind you about conditions and appraisal steps. Support is available by phone, at the branch, and via secure messages.

The experience is beginner-friendly, with strong hand-holding. It’s geared to the military community’s needs.

Who Navy Federal is for

Best for eligible VA borrowers, reservists, veterans, and families seeking low- or $ 0-down options and predictable fees. Great for self-employed members with VA eligibility. If you’re not eligible for membership, choose another lender. No special tech skills needed.

Navy Federal pricing

Pricing depends on loan type. VA loans often allow $0 down payment, and some products have no PMI, which reduces monthly costs. Standard third-party fees apply.

- VA Loans: $0 down for eligible members; funding fee rules apply

- Conventional: Low down options; no PMI on some special products

- Other Programs: Vary by market and member profile

Compared with for-profit lenders, member-focused pricing and no PMI on select loans can be valuable. Always review a Loan Estimate to compare rates and fees.

Pros and cons of Navy Federal

Pros

- $0 down VA options for eligible members

- No PMI on some products reduces the monthly payment

- Member-first service and support

Cons

- Membership eligibility required

- The product menu is narrower than that of large national lenders

- Timelines can vary with volume

If you qualify for membership, put Navy Federal on your shortlist. If not, pick a comparable lender with low fees.

Navy Federal reviews

Reviews vary by product and branch. Review recent member feedback and compare VA-specific borrower experiences over the past 6–12 months.

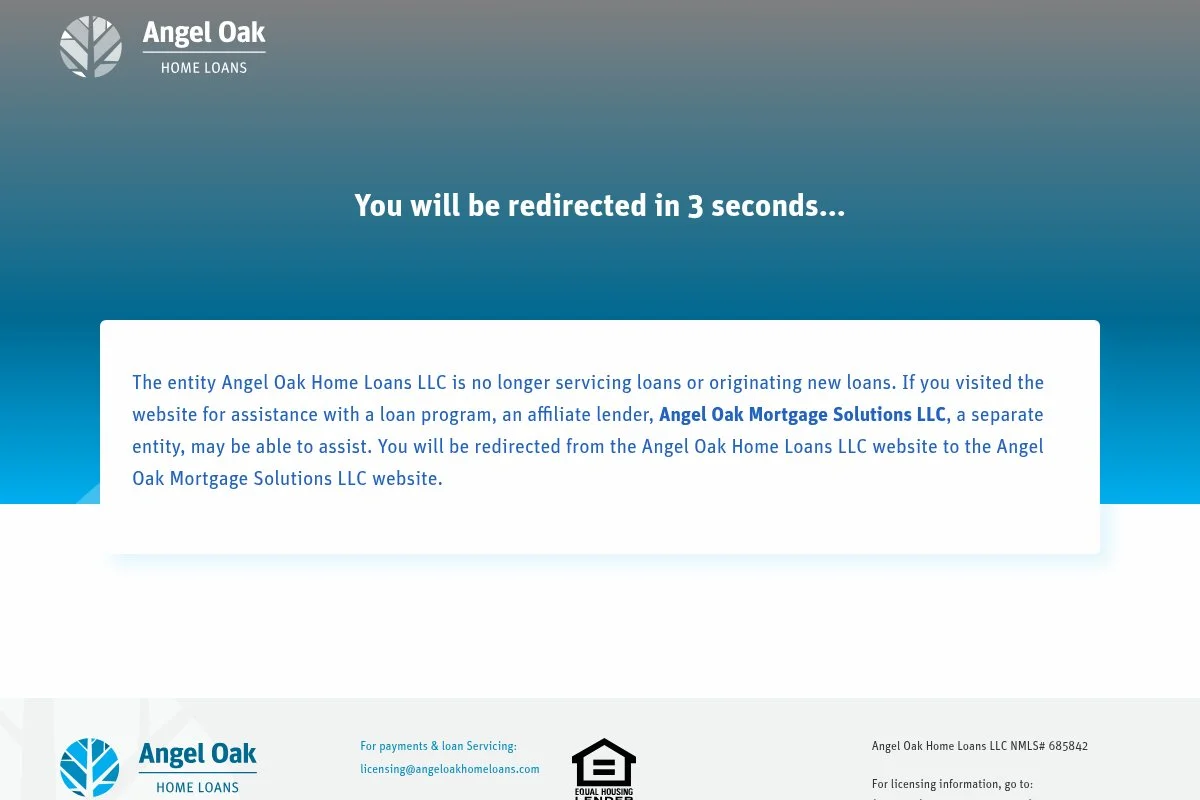

7. Angel Oak Home Loans

Angel Oak Home Loans focuses on non-QM lending, including bank statement mortgages for self-employed borrowers. If tax write-offs lower your qualifying income, this is a notable option.

You’ll work with a loan officer to select a program and provide bank statements, P&L statements, or other alternative docs. The process is hands-on and tailored to your income pattern.

Non-QM programs have expanded in recent years, giving more paths to qualify outside agency rules. That helps buyers who are strong in reality but thin on paper.

Angel Oak offers features such as 12–24-month bank statement averaging and options for recent credit events. These programs trade higher rates/fees for the ability to qualify.

I recommend getting a non-QM quote if two agency lenders say no. Sometimes the math works, even with a higher rate, when rent is rising fast.

Support is consultative. Expect more documentation and explanations, but a better fit for your true income story.

How Angel Oak works and key features

Angel Oak builds underwriting around your cash flow. The officer reviews bank statements, averages deposits, and builds a qualifying income number. You’ll upload everything through a secure portal.

Customization includes loan terms, prepayment rules, and options that fit recent credit events. Reporting clarifies cash-to-close and how reserves affect approval.

Automation is lighter due to manual review. Support is phone-first with close officer contact. No-frills tech, but high-touch help.

For advanced users who value flexibility over headline rate, it’s powerful. Beginners can manage it with a patient officer.

Who Angel Oak is for

Best for entrepreneurs, real estate agents, consultants, seasonal earners, and investors with heavy write-offs. Ideal when tax returns don’t reflect true cash flow. If you qualify easily for an agency loan, a standard lender will be cheaper. No special tech skills needed—expect more paperwork.

Angel Oak pricing

Non-QM pricing includes higher rates and fees than agency loans. Down payments are usually larger, and reserves may be required.

- Bank Statement Loans: 12–24 months of statements; higher down payment is common

- Asset Qualifier/Other: Qualification from assets or alternative docs; custom terms

- Investor Programs: DSCR-style options; tailored pricing

This path costs more but can unlock an approval when agency paths fail. Always compare the total five-year cost to renting or waiting.

Pros and cons of Angel Oak

Pros

- Bank statement and alternative documentation programs

- Flexible options after credit events

- Hands-on underwriting for unique income

Cons

- Higher rates and fees than agency loans

- More paperwork and longer timelines

- Not ideal if you qualify for standard programs

If you need flexibility more than the lowest possible rate, Angel Oak can make homeownership possible. If budget rules all, try agency options first.

Angel Oak reviews

Public non-QM reviews vary by region and market cycles. Ask for recent self-employed borrower references and compare quotes with at least one agency lender.

What is the best mortgage lender right now?

My top picks right now are Better Mortgage, Rocket Mortgage, and Guild Mortgage. Each shines for self-employed borrowers on a budget, but for different reasons.

I personally lean toward Better Mortgage for fee transparency. This isn’t sponsored. I came to Better after comparing Loan Estimates for a few clients and seeing $0 lender fees with competitive rates. What impressed me was how easy it was to model points vs. credits and get a clear cash-to-close number without surprises.

From a value angle, $0 lender fees can save hundreds to thousands at closing. If another lender is 0.125% lower in rate but charges a hefty origination fee, Better can still win on the total five-year cost. Always compare the same-day Loan Estimates to see where the math lands for you.

Rocket Mortgage is a very close second. The app is excellent, communication is timely, and income analysis tools help self-employed borrowers avoid back-and-forth. If you want speed and a smooth interface, Rocket is hard to beat.

What puts Rocket in the running for me is the balance of speed and support. It can combine extended locks, appraisal waivers (when eligible), and strong servicing later. If I needed to close fast on a clean file, I might pick Rocket.

Guild Mortgage is my third pick, especially if you need help with the down payment. The team’s knowledge of grants and program stacking can lower cash-to-close more than shaving an eighth off your rate. For tight budgets, that matters.

I sometimes mix tools: I’ll get a Better quote for low fees, a Rocket quote for speed, and a Guild quote if I’m chasing assistance. Seeing three Loan Estimates the same day gives me confidence that I’m not leaving money on the table.

Choosing among the top options is genuinely tough. I stick with Better when I want the simplest fee picture, Rocket when I need speed and an elite app, and Guild when a grant can change the game.

I hope this helped you narrow your list and feel less stressed about the next step. Happy house hunting—and keep those docs organized.

Frequently Asked Questions

Q: How do I prove income if I’m self-employed?

Most lenders use two years of tax returns and average your income. Some accept 12–24 months of bank statements or a CPA letter. Keep books clean, maintain separate accounts, and be ready with explanations for any gaps.

Q: What fees can I negotiate or reduce?

Ask about lender credits, no-lender-fee programs, and shop title and insurance. Compare same-day Loan Estimates. You can often trade a slightly higher rate for lower upfront costs if cash is tight.

Q: Do down payment assistance programs work for self-employed buyers?

Yes, many programs are income- and location-based, not job-type-based. Lenders like Guild often help pair grants with FHA or conventional loans. Start early because paperwork can add time.

Q: Should I work with a mortgage broker instead of a direct lender?

A good broker can shop multiple lenders, which helps with complex self-employed files. Direct lenders offer tighter control over underwriting and timelines. I compare both: one broker quote and one direct lender quote on the same day.

Photo by Towfiqu barbhuiya: Unsplash