Having advised self-employed professionals across the Southeast for over a decade, I can say that Tennessee is one of the most attractive states in the country for independent workers from a tax perspective. With no state income tax on earned income, freelancers and contractors in Nashville, Memphis, Knoxville, and Chattanooga get to keep more of every dollar they earn compared to their counterparts in neighboring states. I have worked closely with musicians building careers on Music Row, independent healthcare consultants, and a rapidly growing tech freelance community, and the consistent advantage they all share is that Tennessee’s tax structure lets them reinvest more directly into their businesses and their futures.

Self Employment Tax Calculator

What Is Self-Employment Tax in Tennessee?

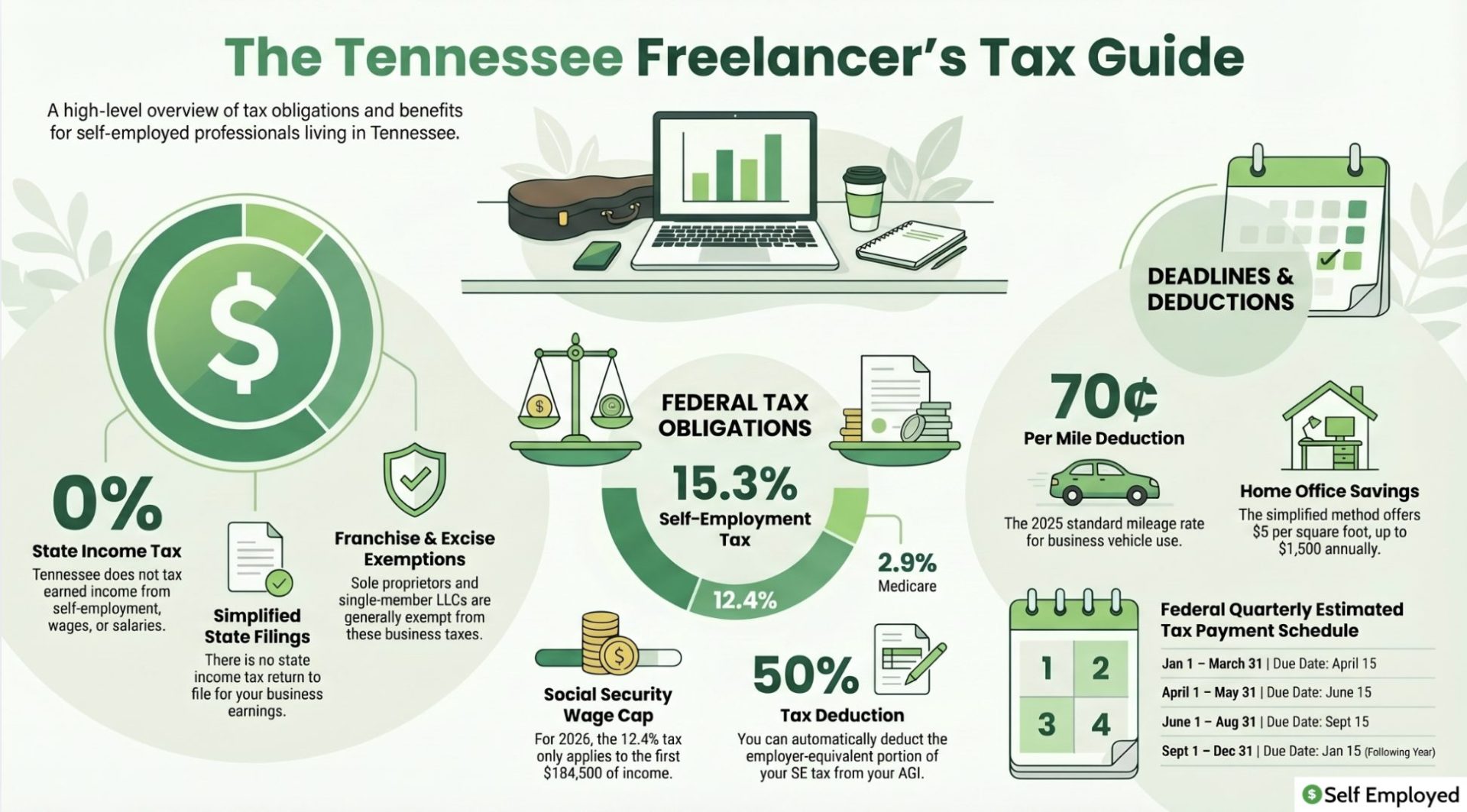

Self-employment tax is the federal tax that independent workers pay to fund Social Security and Medicare. When you work for an employer, the 15.3% combined tax is split evenly between you and your employer at 7.65% each. When you are self-employed, you are responsible for the full 15.3% yourself, covering both the employer and employee portions.

The 15.3% consists of two components. The Social Security portion is 12.4% and applies to your net self-employment earnings up to the annual wage base, which is $176,100 for 2025 and increases to $184,500 for 2026. Earnings above those thresholds are exempt from the Social Security portion. The Medicare portion is 2.9% and applies to all net self-employment income with no cap. If your net earnings exceed $200,000 as a single filer or $250,000 filing jointly, an additional 0.9% Medicare surtax applies to income above that threshold.

An important benefit is that you can deduct the employer-equivalent portion of your self-employment tax, which is 7.65%, from your adjusted gross income on your federal return. This deduction is available regardless of whether you itemize. You must have net self-employment earnings of at least $400 before you are required to pay self-employment tax and file Schedule SE.

Tennessee State Tax Landscape for the Self-Employed

Tennessee is one of the few states that imposes no state income tax on earned income, including wages, salaries, and self-employment income. This has been the case since the state fully repealed its Hall Income Tax on investment income (interest and dividends) effective January 1, 2021. Before that repeal, Tennessee taxed certain investment income but never taxed earned income from self-employment.

For self-employed workers, this means your self-employment income is subject only to federal taxes. There is no state income tax return to file for your business earnings, no state estimated payments to make on earned income, and no state-level deductions to track. This simplification saves time and reduces compliance costs compared to states with complex income tax systems.

Tennessee does have a state sales tax, which at 7% is among the highest in the country. Combined with local sales taxes, the effective rate can reach 9.75% in many areas. While this does not directly affect your self-employment tax obligations, it does impact your cost of doing business if you sell taxable goods or services. Self-employed individuals who sell tangible personal property or certain services in Tennessee need to register for a sales tax permit and collect and remit sales tax.

Tennessee also levies a franchise and excise tax on certain business entities. The excise tax is 6.5% on net earnings, and the franchise tax is 0.25% of net worth or the value of real or tangible personal property in Tennessee, with a minimum of $100. However, sole proprietors and single-member LLCs that are not treated as corporations are generally exempt from these taxes. If you operate as an S corporation or partnership, you should verify whether the franchise and excise tax applies to your entity.

How to File Self-Employment Taxes in Tennessee

Filing self-employment taxes from Tennessee is simpler than in most states because there is no state income tax on earned income to worry about. Your filing obligations are entirely at the federal level.

On the federal side, you report your business income and deductible expenses on Schedule C (Form 1040), which produces your net profit or loss. That net profit carries over to Schedule SE, where your self-employment tax is calculated. The resulting tax is added to your Form 1040, and the deductible half of the SE tax is subtracted from your adjusted gross income on the front page of your return.

If you received $600 or more from any single client during the tax year, that client should provide a Form 1099-NEC documenting the payment. Keep these forms organized alongside your own records of income from all sources. The federal filing deadline is April 15.

While you do not need to file a state income tax return for self-employment earnings, you may still have state-level obligations. If you collect sales tax, you must file Tennessee sales tax returns on the schedule assigned by the Department of Revenue, which can be monthly, quarterly, or annually depending on your volume. If your business entity is subject to the franchise and excise tax, Form FAE170 is due on the 15th day of the fourth month following the close of your tax year.

Quarterly Estimated Tax Payments in Tennessee

Because Tennessee does not tax earned income, your quarterly estimated tax payments are limited to federal obligations. You must make federal estimated payments if you expect to owe $1,000 or more in tax for the year. Payments are made using Form 1040-ES.

| Payment Period | Due Date |

|---|---|

| January 1 – March 31 | April 15 |

| April 1 – May 31 | June 15 |

| June 1 – August 31 | September 15 |

| September 1 – December 31 | January 15 of the following year |

To calculate your quarterly payments, estimate your total annual net self-employment income, apply the 15.3% self-employment tax rate, calculate your expected federal income tax, add the two together, subtract any credits or withholding, and divide by four. The safe harbor method of paying at least 100% of your prior year’s total federal tax liability across four equal installments (or 110% if your AGI exceeded $150,000) protects you from underpayment penalties regardless of how much your income changes.

The absence of state estimated payments is a meaningful administrative benefit for Tennessee’s self-employed workers. In states with income taxes, managing separate federal and state quarterly payments adds complexity, and missing a state payment can trigger separate penalties.

Tax Deductions and Credits for Tennessee’s Self-Employed

Although Tennessee does not have a state income tax, federal deductions remain critical for minimizing your overall tax burden. The deduction for 50% of your self-employment tax is automatic and reduces your adjusted gross income, which in turn lowers your federal income tax.

The home office deduction is available if you use a dedicated space regularly and exclusively for business. The simplified method allows a $5 per square foot deduction up to 300 square feet, providing a straightforward $1,500 deduction. The regular method uses actual expenses based on the business-use percentage of your home.

Self-employed individuals who pay their own health insurance premiums can deduct the cost of medical, dental, vision, and qualifying long-term care coverage from AGI. Retirement contributions through a SEP-IRA (up to 25% of net self-employment earnings) or Solo 401(k) reduce taxable income dollar for dollar.

Ordinary business expenses including software subscriptions, advertising, professional development, supplies, and professional service fees are fully deductible. Vehicle use for business purposes can be deducted at the standard mileage rate of 70 cents per mile for 2025 or through actual expense tracking.

| Deduction Category | Details |

|---|---|

| Self-Employment Tax Deduction | 50% of SE tax, reduces AGI automatically |

| Home Office | Simplified: $5/sq ft (max $1,500) or actual expenses |

| Health Insurance Premiums | Medical, dental, vision, long-term care |

| Retirement Contributions | SEP-IRA (up to 25% of net SE income), Solo 401(k) |

| Business Expenses | Supplies, software, advertising, professional fees |

| Vehicle/Mileage | 70 cents/mile (2025) or actual vehicle expenses |

Avoiding Common Pitfalls

Forgetting About Sales Tax Obligations

The most common mistake self-employed Tennesseans make is assuming that no state income tax means no state tax obligations at all. If you sell taxable goods or certain services, you must collect and remit Tennessee sales tax. The state’s combined state and local sales tax rates are among the highest in the nation, and failure to register and collect properly can result in significant back taxes and penalties. Check with the Tennessee Department of Revenue to determine whether your products or services are subject to sales tax.

Underestimating Federal Tax Obligations

Because Tennessee has no state income tax, some self-employed workers focus too much on the state advantage and neglect proper federal tax planning. The federal self-employment tax of 15.3% plus federal income tax represent your entire income tax burden, and failing to set aside enough for quarterly payments is a frequent issue. A good rule of thumb is to set aside 25% to 30% of your net self-employment income for federal taxes.

Misunderstanding Franchise and Excise Tax

Sole proprietors are generally exempt from Tennessee’s franchise and excise tax, but if you have structured your business as an LLC taxed as a corporation, an S corporation, or a partnership, you may be subject to these taxes. The excise tax of 6.5% on net earnings can be a meaningful expense. Verify your entity’s status with a tax professional if you are unsure.

Final Thoughts on Self-Employment Tax in Tennessee

Tennessee’s absence of a state income tax on earned income makes it one of the best states in the country for self-employed professionals from a pure tax perspective. Your obligations are streamlined to federal self-employment tax and federal income tax, with no state income tax return to file and no state estimated payments to manage on earned income. The trade-off is a higher sales tax, but for service-based businesses that do not sell taxable goods, this has minimal impact. Focus your energy on maximizing federal deductions, making timely quarterly estimated payments, and maintaining thorough records. Those three habits will serve you well in Tennessee’s favorable tax environment.

Frequently Asked Questions

Does Tennessee have a state income tax on self-employment income?

No. Tennessee does not impose a state income tax on earned income, including self-employment income. The state fully repealed its Hall Income Tax on investment income effective January 1, 2021. Self-employed workers in Tennessee are subject only to federal self-employment tax and federal income tax on their business earnings.

What is self-employment tax in Tennessee?

Self-employment tax in Tennessee is the federal tax that independent workers pay to fund Social Security and Medicare. The rate is 15.3% of net self-employment earnings, split between 12.4% for Social Security (on income up to $184,500 in 2026) and 2.9% for Medicare on all earnings. Since Tennessee has no state income tax on earned income, this federal tax is your primary income-related obligation.

Do I need to make quarterly estimated tax payments in Tennessee?

You need to make federal quarterly estimated payments if you expect to owe $1,000 or more in federal tax. These are due April 15, June 15, September 15, and January 15 of the following year using Form 1040-ES. You do not need to make state estimated income tax payments since Tennessee does not tax earned income.

What about Tennessee’s sales tax for self-employed workers?

Tennessee has a 7% state sales tax, and combined with local taxes, rates can reach 9.75%. If you sell taxable goods or certain services, you must register for a sales tax permit and collect and remit sales tax. Service-based businesses that do not sell tangible goods are generally not subject to sales tax, but you should verify with the Tennessee Department of Revenue.

What deductions can I claim as a self-employed person in Tennessee?

Self-employed individuals in Tennessee can claim all standard federal deductions including 50% of self-employment tax, health insurance premiums, home office expenses, retirement contributions to a SEP-IRA or Solo 401(k), business vehicle mileage at 70 cents per mile for 2025, and ordinary business expenses. Since there is no state income tax on earned income, these deductions apply only to your federal tax liability.