As a self-employed professional in North Dakota, understanding the north dakota income tax rate and how self-employment tax works is essential for managing your finances effectively. I’ve worked with countless independent contractors and small business owners navigating these tax obligations, and I want to share what I’ve learned about maximizing deductions while staying compliant with both state and federal requirements.

North Dakota offers one of the most favorable tax environments in the nation for self-employed individuals. The state’s three-bracket income tax system, combined with no local income taxes, creates a streamlined approach to tax planning. However, self-employment tax at the federal level remains a significant obligation that requires careful attention and quarterly planning.

In this guide, I’ll walk you through the complete picture of the north dakota income tax rate system, self-employment tax calculations, deduction strategies, and payment schedules. Whether you’re a freelancer, consultant, or business owner, this information will help you take control of your tax situation.

Understanding North Dakota’s income tax rate system

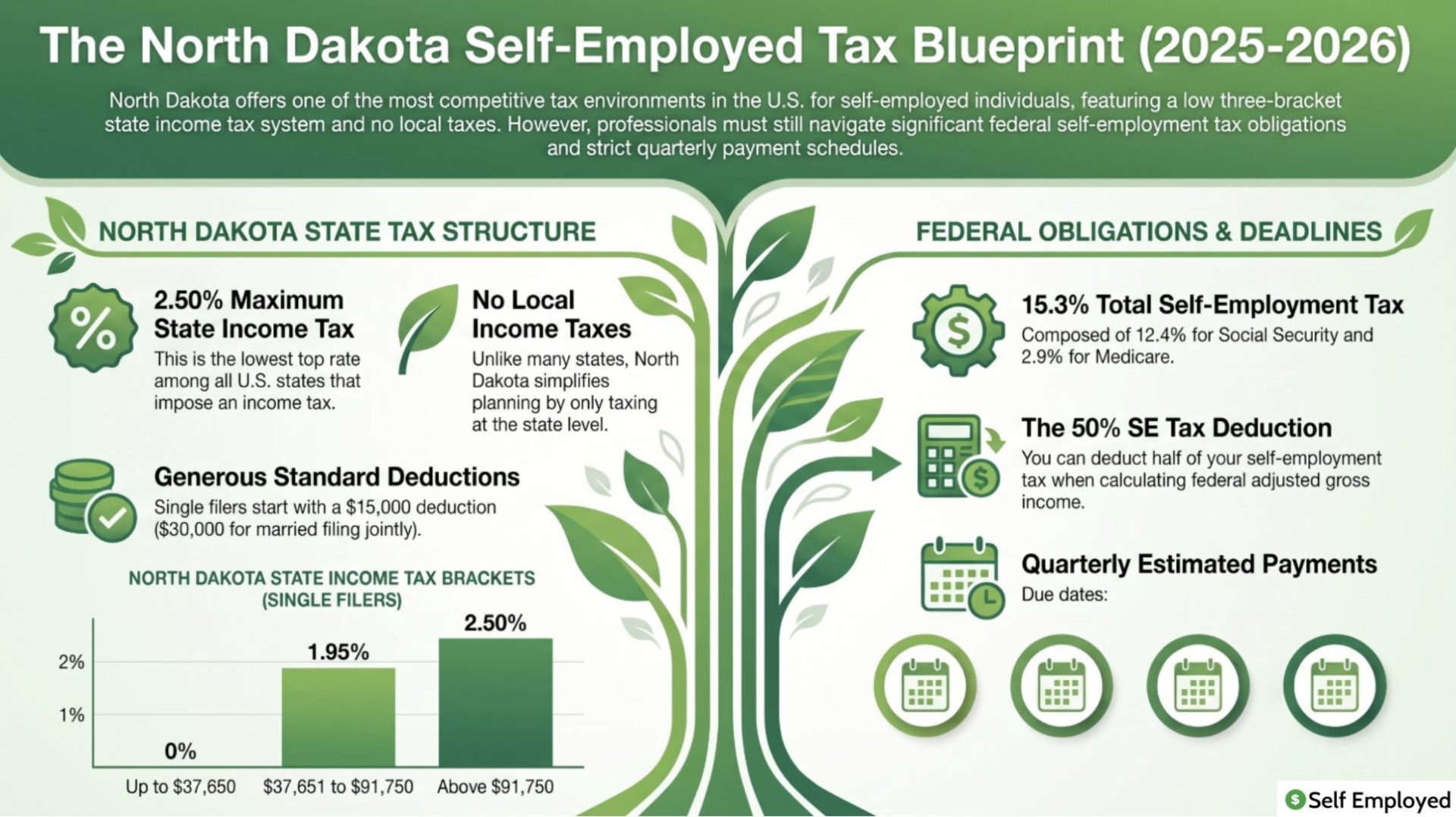

North Dakota maintains one of the most competitive tax structures in the United States. The state’s three-bracket system with a top north dakota income tax rate of just 2.50% is the lowest among all states that impose an income tax. This makes North Dakota particularly attractive for self-employed individuals looking to minimize their state tax burden.

Here’s how the brackets work:

- 0% on income up to $37,650 (single) or $66,900 (married filing jointly)

- 1.95% on income from $37,651 to $91,750 (single) or $66,901 to $191,550 (married filing jointly)

- 2.50% on income above $91,750 (single) or $191,550 (married filing jointly)

The standard deduction in North Dakota is $15,000 for single filers and $30,000 for married filing jointly. These deductions significantly reduce your taxable income before you even calculate the state income tax owed.

Unlike many states, North Dakota imposes no local income taxes. This means your only state income tax obligation comes at the state level, making your tax planning simpler and more predictable. I’ve found this clarity particularly helpful when working with clients across multiple states.

Self-employment tax explained

Self-employment tax is a federal tax that covers Social Security and Medicare taxes for self-employed individuals. While the north dakota income tax rate applies only to state income, self-employment tax is mandatory for all self-employed Americans regardless of where they operate.

The total self-employment tax rate is 15.3%, composed of two parts:

- Social Security tax: 12.4% on net earnings up to $176,100 for 2025 (and $184,500 for 2026)

- Medicare tax: 2.9% on all net self-employment earnings with no cap

You’re responsible for paying both the employer and employee portions of these taxes, which is why the rate is higher than what employees see withheld from their paychecks. However, you can deduct half of your self-employment tax when calculating your adjusted gross income, which provides some relief.

Calculating self-employment tax starts with your net profit from your business. You’ll multiply this by 92.35% to account for the employer portion deduction, then apply the self-employment tax rate. For most self-employed individuals, this results in a significant quarterly tax obligation.

Calculating your combined tax obligation

To understand your complete tax picture in North Dakota, you need to account for both state income tax and federal self-employment tax. Let me walk through a practical example.

Suppose you have $80,000 in net self-employment income. After claiming the standard deduction of $15,000, your taxable income is $65,000. At the 1.95% North Dakota rate, your state income tax would be approximately $1,267.50.

For self-employment tax, you’d calculate 92.35% of $80,000 ($73,880) and apply the 15.3% rate, resulting in approximately $11,304. You can then deduct half of this self-employment tax, further reducing your adjusted gross income for federal tax purposes.

This combined approach shows how North Dakota’s favorable state tax rate is offset somewhat by federal self-employment obligations. Understanding both components helps you plan effectively for quarterly payments and annual tax filings.

Maximizing deductions for self-employed professionals

One of the most powerful strategies I’ve learned for reducing tax liability is maximizing available deductions. Self-employed individuals in North Dakota can deduct many business expenses that employees cannot, effectively lowering both state and federal tax obligations.

Common deductible expenses include:

- Office supplies and equipment

- Professional fees and subscriptions

- Marketing and advertising costs

- Travel and vehicle expenses (mileage or actual)

- Health insurance premiums

- Contributions to a self-employed retirement plan (SEP-IRA or Solo 401k)

- Home office expenses

The home office deduction deserves special attention for remote workers. You can deduct either a simplified amount ($5 per square foot up to 300 square feet) or calculate actual expenses like rent, utilities, insurance, and maintenance proportional to your office space.

I particularly recommend exploring strategies used by self-employed professionals in other states for comparative insights, even though your state tax situation differs. Additionally, reviewing essential forms for self-employed professionals ensures you’re capturing all available deductions properly documented.

Quarterly estimated tax payments

Unlike W-2 employees who have taxes withheld throughout the year, self-employed individuals must make quarterly estimated tax payments. The IRS requires estimated payments when you expect to owe $1,000 or more in taxes.

Quarterly payments are due on:

- April 15 for income earned January through March

- June 15 for income earned April and May

- September 15 for income earned June through August

- January 15 (following year) for income earned September through December

The estimated tax payment includes both federal income tax and self-employment tax. I recommend setting aside approximately 30-35% of your net profit quarterly to cover these obligations, then adjusting based on your actual annual tax calculation.

Missing or underpaying estimated taxes can result in penalties and interest charges. The IRS applies these penalties based on the underpayment amount and duration, making timely quarterly payments crucial for managing your overall tax liability.

North Dakota tax forms and filing

Filing taxes as a self-employed individual requires completing several forms. The primary forms you’ll need include:

- Schedule C (or Schedule C-EZ) to report business income and expenses

- Schedule SE to calculate self-employment tax

- Form 1040 (individual income tax return)

- Form ND-1 (North Dakota tax return)

North Dakota requires separate state tax filing even if you have no state income tax liability. The state return allows you to claim deductions and credits that may reduce your liability below zero, resulting in a refund.

For detailed information on federal forms and filing requirements, visit the IRS website. For North Dakota-specific guidance, the North Dakota Office of State Tax Commissioner provides resources and forms.

Tax planning strategies for North Dakota self-employed individuals

Beyond simply calculating what you owe, strategic tax planning can significantly reduce your overall liability. I’ve found several approaches particularly effective for North Dakota-based self-employed professionals.

First, maximize your retirement contributions. A Solo 401k or SEP-IRA allows you to defer income and reduce current-year taxable income. For 2025, you can contribute up to $69,000 to a Solo 401k (or $76,500 if age 50+), which directly reduces both state and federal taxable income.

Second, consider business structure. While sole proprietorship is simplest, some self-employed individuals benefit from forming an S-Corporation for self-employment tax savings. This strategy works best for those with net self-employment income exceeding $70,000 annually.

Third, track and document all deductions meticulously. The difference between a thorough deduction strategy and a casual approach can amount to thousands of dollars annually. I recommend maintaining detailed records of all business expenses, mileage, and time spent on deductible activities.

Fourth, plan for estimated tax payments strategically. If your income varies significantly during the year, you may be able to adjust quarterly payment amounts based on actual earnings rather than equal installments.

Frequently asked questions about North Dakota income tax and self-employment tax

What is the highest north dakota income tax rate?

The highest North Dakota income tax rate is 2.50%, which applies to income above $91,750 for single filers or $191,550 for married filing jointly. This is the lowest top rate among all states that impose an income tax.

Do I owe North Dakota income tax as a non-resident?

If you’re a non-resident who earned income sourced in North Dakota, you may owe North Dakota income tax on that income. However, if you’re working remotely for a non-North Dakota employer from a North Dakota location, you typically don’t owe state tax. The sourcing of income determines the filing requirement.

Can I deduct my self-employment tax?

Yes, you can deduct half of your self-employment tax when calculating your adjusted gross income. This deduction reduces your federal taxable income but does not reduce your state taxable income, though it does lower your federal liability.

What are the self-employment tax rates for 2026?

For 2026, the self-employment tax rate remains 15.3% total: 12.4% for Social Security on earnings up to $184,500, plus 2.9% for Medicare with no earnings cap. These rates are set by federal law and apply in all states including North Dakota.

Do I need to file quarterly estimated tax payments in North Dakota?

You need to make quarterly federal estimated tax payments if you expect to owe $1,000 or more in taxes. North Dakota doesn’t have separate quarterly state requirements, but your quarterly federal payments should account for both federal income tax and self-employment tax obligations.

How do local income taxes affect self-employed individuals in North Dakota?

North Dakota has no local income taxes, so self-employed individuals only owe state and federal taxes. This simplifies tax planning and results in lower overall tax liability compared to many other states.

Can I claim the home office deduction in North Dakota?

Yes, you can claim the home office deduction on your federal taxes, which reduces your self-employment income subject to self-employment tax. North Dakota allows this deduction on your state return as well, providing a dual tax benefit.

Additional resources for self-employed tax planning

Understanding your complete tax picture requires staying informed about changes and maximizing available resources. Here are some guides that can help your overall tax strategy across different states.

For comparative insights into how self-employment taxes work in other jurisdictions, explore our comprehensive guides to self-employment tax in other states:

- Self-employment tax guide for California

- Self-employment tax guide for Texas

- Self-employment tax guide for Florida

- Self-employment tax guide for New York

- Self-employment tax guide for Washington

These resources provide state-by-state comparisons that help you understand how North Dakota’s favorable tax environment compares to other states, which is particularly useful if you’re considering relocation or expanding your business into multiple states.

Taking action on your North Dakota tax strategy

Understanding the north dakota income tax rate and self-employment tax obligations is the first step toward effective tax management. The next step is implementing a comprehensive strategy tailored to your specific situation.

I recommend starting by gathering your business income and expense records for the current year, then calculating your estimated tax liability using the brackets and rates outlined in this guide. Next, set up a system for quarterly estimated tax payments to avoid penalties and manage cash flow effectively.

Finally, consider working with a tax professional who understands North Dakota’s tax code and can help you identify deductions specific to your business. The investment in professional guidance often pays for itself through deductions and strategies you might otherwise miss.

Your North Dakota self-employment tax situation is manageable with proper planning and knowledge. By taking control of your tax strategy now, you’ll reduce stress at tax time and optimize your overall financial position.