California self-employment tax is among the most demanding in the country, and as someone who works with self-employed professionals in the state every day, I can tell you the numbers are real. California’s progressive income tax system, with rates climbing as high as 13.3%, means freelancers and independent contractors face some of the highest combined tax burdens in the nation. I have helped graphic designers in Los Angeles, tech consultants in the Bay Area, and content creators in San Diego work through these numbers, and the one thing they all share is that understanding the full picture – including the interplay between federal self-employment tax and California’s steep state rates – is what separates those who thrive from those who get blindsided every April.

Self-Employment Tax Calculator

What is self-employment tax in California?

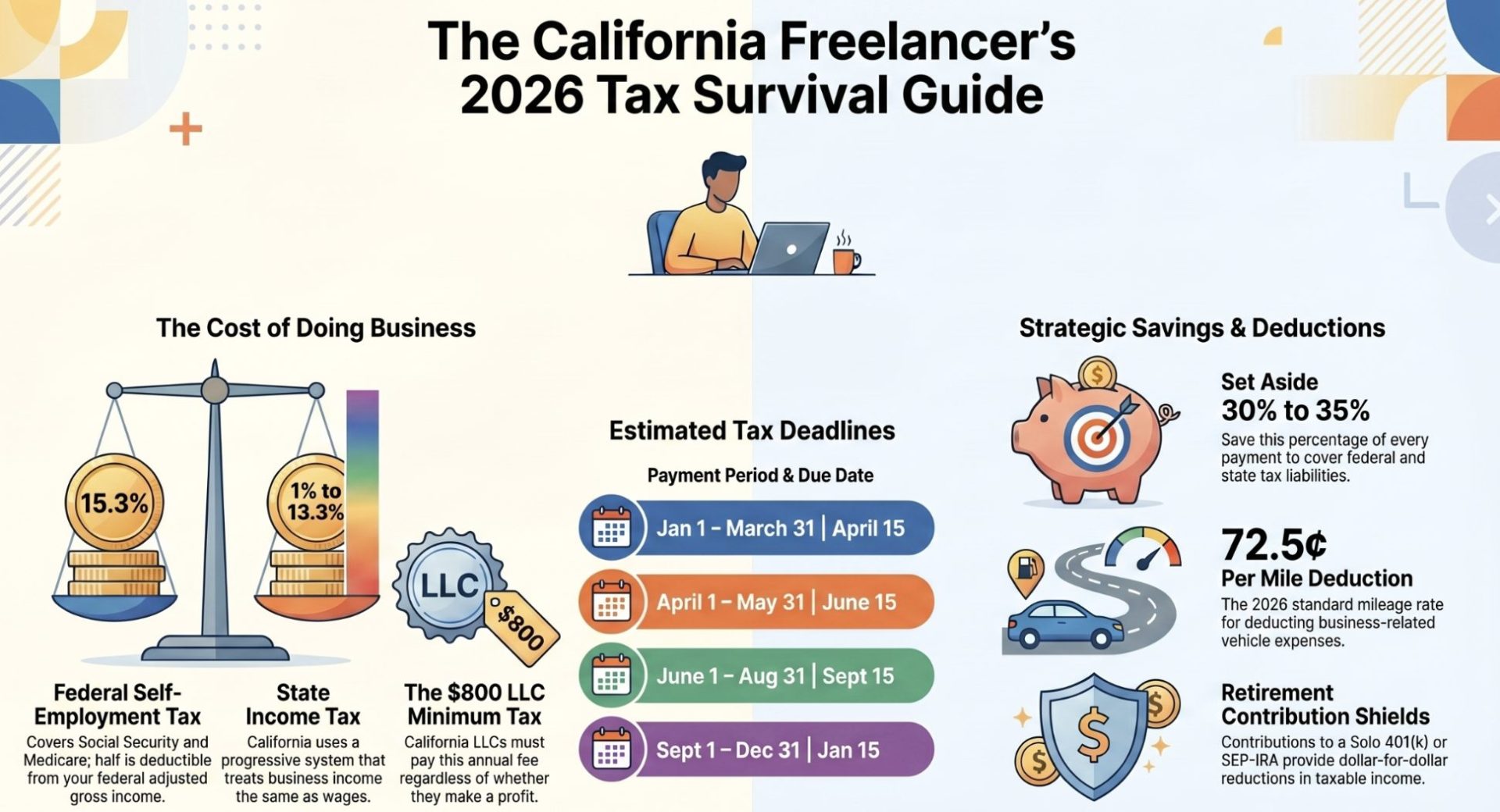

Self-employment tax is the mechanism through which independent workers fund Social Security and Medicare. When you work as a traditional employee, your employer pays half of these contributions and you pay the other half through payroll withholding. When you are self-employed, you cover the entire 15.3% yourself, which breaks down into 12.4% for Social Security and 2.9% for Medicare.

The Social Security portion applies only up to an annual wage base, which is $176,100 for the 2025 tax year and $184,500 for 2026. Once your net self-employment earnings exceed that threshold, you stop paying the 12.4% Social Security tax on the excess. The 2.9% Medicare tax, however, has no cap and applies to every dollar of net self-employment income. If your earnings exceed $200,000 as a single filer or $250,000 filing jointly, an additional 0.9% Medicare surtax applies to income above those thresholds.

One significant benefit available to all self-employed individuals is the ability to deduct the employer-equivalent portion of self-employment tax, which is 7.65%, from your adjusted gross income on your federal return. This is an above-the-line deduction, meaning you receive it regardless of whether you itemize. You are required to pay self-employment tax if your net earnings from self-employment reach $400 or more during the tax year.

It is important to understand that self-employment tax is a federal tax. California does not impose its own separate self-employment tax. However, your self-employment income is fully subject to California’s state income tax, which is where things get expensive for high earners in this state.

California state income tax for the self-employed

California’s progressive tax brackets

California has one of the most progressive income tax systems in the country, with nine brackets ranging from 1% to 12.3%. There is also an additional 1% Mental Health Services Tax surcharge on taxable income exceeding $1 million, bringing the effective top rate to 13.3%. For the 2025 tax year, the standard deduction for single filers is $5,706 and for married filing jointly it is $11,412.

These rates apply to your California taxable income, which for self-employed individuals starts with your federal adjusted gross income and is modified by California-specific adjustments. Unlike some states that offer preferential rates for business income, California taxes self-employment income at the same rates as wage income.

| Taxable Income (Single) | California Rate |

|---|---|

| $0 – $10,756 | 1% |

| $10,757 – $25,499 | 2% |

| $25,500 – $40,245 | 4% |

| $40,246 – $55,866 | 6% |

| $55,867 – $70,606 | 8% |

| $70,607 – $360,659 | 9.3% |

| $360,660 – $432,787 | 10.3% |

| $432,788 – $721,314 | 11.3% |

| Over $721,314 | 12.3% |

| Over $1,000,000 | Additional 1% surcharge |

For a self-employed Californian earning $100,000 in net income after deductions, the combined federal self-employment tax, federal income tax, and California state income tax can easily exceed 40% of earnings. This makes tax planning and deduction optimization absolutely critical in California.

State Disability Insurance for the self-employed

California offers a unique option for self-employed individuals: voluntary participation in the State Disability Insurance (SDI) program. Traditional employees have SDI withheld automatically, but self-employed workers can elect to opt in. If you do, you pay the SDI rate (currently around 1.1% of income) and gain access to disability and paid family leave benefits. This is worth considering if you do not carry private disability insurance, though it does add to your overall tax and contribution burden.

California Franchise Tax Board filing

Self-employed individuals file their California state return using Form 540. Your federal adjusted gross income serves as the starting point, and California’s own schedule of adjustments may add or subtract certain items. California requires estimated tax payments if you expect to owe $500 or more in state tax after withholding and credits. The state also treats capital gains as ordinary income, meaning profits from selling investments are taxed at the same progressive rates as your self-employment earnings.

How to file self-employment taxes in California

Filing self-employment taxes in California requires coordinating your federal return with your California state return. On the federal side, you report your business income and expenses on Schedule C (Form 1040), which calculates your net profit. That net profit flows to Schedule SE, where your 15.3% self-employment tax is computed. The deductible half of your SE tax is then subtracted from your adjusted gross income on the main Form 1040. Reviewing the essential tax forms for self-employed professionals ensures you file the right documents at both the federal and state level.

For California, you file Form 540, the state’s individual income tax return. Your federal AGI carries over as the starting point, and you apply California-specific modifications. If you made estimated tax payments during the year using Form 540-ES, those payments are credited against your final state tax liability.

Clients who paid you $600 or more during the year should provide a Form 1099-NEC. However, you are responsible for reporting all self-employment income regardless of whether you received a 1099. California’s Franchise Tax Board actively cross-references federal return data with state filings, so discrepancies between your federal and state reported income will trigger inquiries.

One filing consideration unique to California is the $800 minimum franchise tax for LLCs. If you have structured your freelance business as a California LLC, you owe this flat fee regardless of whether the LLC generated a profit. LLCs with gross revenue exceeding $250,000 also owe an additional fee ranging from $900 to $11,790 depending on revenue level. Sole proprietors who have not formed an LLC are not subject to this fee.

Quarterly estimated tax payments in California

Self-employed individuals in California must make estimated tax payments to both the IRS and the California Franchise Tax Board throughout the year. Federal estimated payments are required if you expect to owe $1,000 or more in federal tax, and California requires estimated payments if you expect to owe $500 or more in state tax.

The quarterly due dates follow a slightly uneven schedule:

| Payment Period | Due Date |

|---|---|

| January 1 – March 31 | April 15 |

| April 1 – May 31 | June 15 |

| June 1 – August 31 | September 15 |

| September 1 – December 31 | January 15 of the following year |

To calculate your quarterly payment, estimate your total annual net self-employment income, apply the 15.3% federal SE tax rate, add your expected federal income tax and California state income tax, subtract any withholding or credits, and divide by four. The safe harbor approach works well here: paying at least 100% of last year’s total tax liability (or 110% if your AGI exceeded $150,000) across four installments will protect you from underpayment penalties regardless of how your current year income fluctuates.

California’s underpayment penalty is calculated at a rate that typically runs around 7% annually on the underpaid amount. Combined with the federal underpayment penalty, missing quarterly deadlines can become costly quickly, especially given California’s high tax rates.

Tax deductions and credits for California’s self-employed

Given California’s high tax rates, maximizing your deductions is not optional – it is essential for keeping your tax burden manageable. The good news is that most federal deductions flow through to reduce your California taxable income as well, since California uses your federal AGI as the starting point for its return.

The 50% self-employment tax deduction automatically reduces your federal AGI, which in turn lowers your California taxable income. For someone earning $100,000 in net self-employment income, this deduction alone saves roughly $7,650 in federal AGI reduction, which then saves you additional money on your California state taxes as well.

The home office deduction is particularly valuable in California, where housing costs are among the highest in the nation. The simplified method allows a $5 per square foot deduction up to 300 square feet for a maximum of $1,500. The actual expense method, which accounts for the percentage of your home used exclusively for business and applies it to rent or mortgage interest, utilities, insurance, and maintenance, often yields a significantly larger deduction in high-cost California markets.

Health insurance premiums for medical, dental, vision, and long-term care coverage are deductible from your federal AGI if you are self-employed and not eligible for employer-sponsored coverage through a spouse. This deduction reduces both your federal and California tax liability.

Retirement contributions through a SEP-IRA (up to 25% of net self-employment earnings) or Solo 401(k) provide dollar-for-dollar reductions in taxable income. Given California’s top rate of 13.3%, a $20,000 retirement contribution could save a high-earning Californian over $2,600 in state taxes alone, in addition to federal savings.

Business expenses including software subscriptions, advertising, professional development, supplies, travel, and professional service fees are all deductible. Vehicle expenses can be deducted using the standard mileage rate of 72.5 cents per mile for 2026 (up from 70 cents in 2025) or actual vehicle costs. Good year-round bookkeeping for the self-employed is essential for tracking these deductions throughout the year.

| Deduction Category | Details |

|---|---|

| Self-Employment Tax Deduction | 50% of SE tax, reduces federal AGI and CA taxable income |

| Home Office | Simplified: $5/sq ft (max $1,500) or actual expenses |

| Health Insurance Premiums | Medical, dental, vision, long-term care |

| Retirement Contributions | SEP-IRA (up to 25% of net SE income), Solo 401(k) |

| Business Expenses | Supplies, software, advertising, professional fees, travel |

| Vehicle/Mileage | 72.5 cents/mile (2026) or actual vehicle expenses |

Strategies for reducing your California tax burden

Choosing the right business structure

One of the most impactful decisions a California freelancer can make is choosing the right business structure. Operating as a sole proprietor is the simplest option, but forming an S Corporation can provide meaningful tax savings once your net income reaches approximately $60,000 to $80,000 or more. With an S Corp, you pay yourself a reasonable salary (subject to payroll taxes) and take the remaining profit as distributions, which are not subject to self-employment tax. This strategy can save thousands of dollars annually, though it comes with additional administrative costs including payroll processing and a separate corporate tax return. Keep in mind that California imposes a minimum $800 franchise tax on LLCs and S Corps, which erodes the benefit at lower income levels.

Timing income and expenses

Because California’s rates are so high, the timing of income recognition and expense deductions matters more here than in most states. If you expect your income to be significantly higher in one year than the next, accelerating deductible expenses into the high-income year and deferring income where legally possible can generate meaningful tax savings. Conversely, if you anticipate a jump in income next year, consider deferring large deductions to offset that higher income.

Retirement account maximization

Contributing the maximum allowable amount to a SEP-IRA or Solo 401(k) is one of the single most effective tax reduction strategies for California’s self-employed. These contributions reduce both federal and California taxable income simultaneously. A Solo 401(k) allows up to $23,500 in employee deferrals for 2025 (plus $7,500 catch-up if you are 50 or older), plus employer contributions of up to 25% of net self-employment income, for a combined maximum that can exceed $69,000.

Avoiding common pitfalls

Underestimating your total tax burden

The most common mistake I see California freelancers make is underestimating how much they actually owe. When you add 15.3% federal self-employment tax, federal income tax at your marginal rate, and California state tax that can reach 9.3% or higher for moderate incomes, the total effective rate often surprises people. A self-employed Californian earning $120,000 in net income can easily face an effective combined rate approaching 40% before accounting for deductions. Setting aside 30% to 35% of every payment you receive is a reasonable baseline for most California freelancers.

Ignoring the LLC franchise tax

Many freelancers form California LLCs without fully understanding the cost implications. The $800 annual minimum franchise tax applies even if your LLC earns nothing, and the LLC fee structure adds additional costs starting at $250,000 in gross revenue. If your freelance income is modest, operating as a sole proprietor may be more cost-effective until your earnings justify the LLC or S Corp structure.

Failing to separate business and personal finances

California’s Franchise Tax Board is known for being thorough in its auditing practices. Mixing business and personal expenses makes it difficult to substantiate deductions and can trigger additional scrutiny. Maintaining a dedicated business bank account and using accounting software to categorize every transaction will save you significant stress if you are ever audited and will make your annual filing process much smoother. The California Franchise Tax Board website provides detailed guidance on self-employment filing requirements.

Final thoughts on self-employment tax in California

California is one of the most challenging states for self-employed individuals from a tax perspective, but it is also one of the most rewarding places to build a business. The combination of 15.3% federal self-employment tax and California’s progressive income tax rates up to 13.3% demands proactive tax planning. By maximizing your deductions, making timely quarterly estimated payments, choosing the right business structure, and contributing aggressively to retirement accounts, you can keep your effective tax rate well below the theoretical maximums. If your self-employment income exceeds $100,000, working with a CPA or tax professional who specializes in California self-employment tax is one of the best investments you can make.

Frequently Asked Questions

What is the self-employment tax rate in California?

The federal self-employment tax rate is 15.3%, which includes 12.4% for Social Security (on net earnings up to $184,500 in 2026) and 2.9% for Medicare on all earnings. California does not impose a separate state self-employment tax, but your self-employment income is subject to California state income tax at rates ranging from 1% to 13.3%.

How much should I set aside for taxes as a California freelancer?

A reasonable guideline is to set aside 30% to 35% of your net self-employment income for federal and California state taxes combined. If your income exceeds $200,000, consider setting aside closer to 40% to account for the higher California tax brackets and the additional Medicare surtax.

When are quarterly estimated tax payments due in California?

Quarterly estimated payments are due on April 15, June 15, September 15, and January 15 of the following year. These deadlines apply to both federal estimated payments (Form 1040-ES) and California state estimated payments (Form 540-ES). California requires estimated payments if you expect to owe $500 or more in state tax.

What deductions can I claim as a self-employed person in California?

You can deduct 50% of your self-employment tax, health insurance premiums, home office expenses, retirement contributions to a SEP-IRA or Solo 401(k), vehicle mileage at 72.5 cents per mile for 2026, and ordinary business expenses like software, advertising, supplies, and professional services. Most federal deductions also reduce your California taxable income.

Do I need to pay the $800 LLC franchise tax in California?

Only if you have formed a California LLC or S Corporation. Sole proprietors who operate under their own name or a DBA are not subject to the $800 minimum franchise tax. If you have formed an LLC, the fee applies annually regardless of whether the business generated income.

What forms do I need to file self-employment taxes in California?

At the federal level, you need Schedule C (business income and expenses), Schedule SE (self-employment tax calculation), and Form 1040. For California, file Form 540, the state individual income tax return. If making estimated payments, use Form 1040-ES for federal and Form 540-ES for California.