Hi, I’m Elliot from Selfemployed.com. After two decades helping self-employed professionals navigate mortgages, I’ve learned that the biggest barrier isn’t finding money—it’s understanding what lenders will approve and at what cost. The self-employed mortgage calculator is your first tool in that discovery process. This guide shows you how to use it effectively and what the numbers actually mean for your mortgage eligibility.

Unlike traditional employees who plug in a straightforward salary, self-employed professionals need calculators that account for business expenses, income variability, and the unique way lenders evaluate self-employment income. Understanding how to use these tools properly gives you accurate approval expectations before talking to an actual lender.

## What a Self-Employed Mortgage Calculator Does Differently

A standard mortgage calculator assumes steady W-2 income and simple debt obligations. You input monthly income and debts, and it outputs how much you can borrow. It’s fast but dangerously inaccurate for self-employed professionals.

Self-employed calculators account for the complexity lenders actually evaluate. They recognize that your taxable income (what appears on your tax returns) often differs significantly from your actual cash flow. They model how business expenses, depreciation, and deductions affect your qualifying income. They understand that mortgage lenders usually average your self-employment income over two years rather than using current-year income alone.

Effective calculators also incorporate different income verification methods. Some allow you to input bank statement income separately from tax return income, recognizing that some lenders accept your actual deposits while others use tax-return-averaged figures.

## Key Inputs: Understanding What Lenders Need to See

Accurate calculator results depend on accurate inputs. Here’s what you’ll typically need:

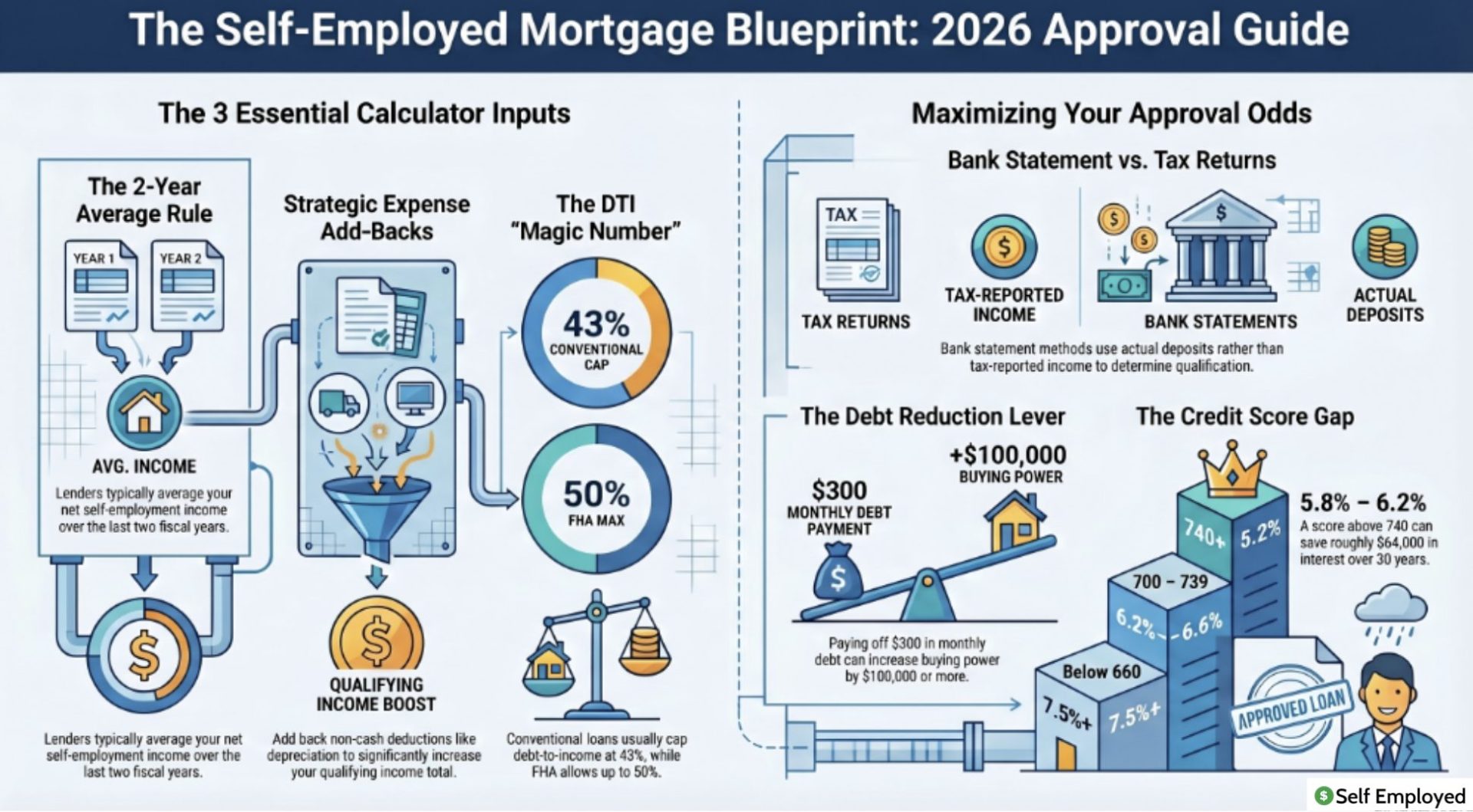

Your average monthly gross self-employment income from the last two years. If your tax returns showed $80,000 in net self-employment income for year one and $95,000 for year two, your average is $87,500 annually or about $7,292 monthly. Some lenders may add back certain deductions like home office expenses or vehicle depreciation, so have those figures available too.

Your complete monthly debt obligations. Include credit card minimum payments, car loans, student loans, personal loans, and any other regular debts. Don’t forget less obvious obligations like child support or alimony. Mortgage lenders will discover these anyway through credit reports.

Your available down payment. Larger down payments improve approval odds and affect your monthly payment. Most calculators show results for different down payment percentages, helping you see how $25,000 versus $50,000 down changes your buying power.

Your estimated credit score. While a calculator won’t change its core math based on this, it helps you understand interest rate ranges. Self-employed borrowers with scores above 720 get substantially better rates than those scoring 650-680.

Your target loan term. Most calculators assume 30-year mortgages as default, but many self-employed borrowers prefer 15-year or 20-year terms to minimize interest paid. Running scenarios with different terms shows the monthly payment and total interest cost differences.

## Using Business Expense Add-Backs Strategically

This feature distinguishes quality self-employed calculators from basic tools. Many legitimate business deductions reduce your tax liability but don’t reduce actual cash availability. Lenders recognize certain add-backs, meaning they add these expenses back to your taxable income for mortgage qualification purposes.

Common add-backs include depreciation (especially real estate depreciation if you own a home office or rental property used for business), business insurance premiums, professional dues and licenses, vehicle expenses claimed as depreciation, and sometimes meals and entertainment above a certain threshold.

If your tax returns show $75,000 in net self-employment income but your accountant included $15,000 in home depreciation, mortgage lenders might use $90,000 as your qualifying income. Entering $75,000 as base income and $15,000 as add-backs gives you the accurate $90,000 figure a lender would use.

However, not all deductions qualify for add-backs. Actual cash expenses like salaries you pay employees, equipment purchases, and supplies don’t get added back. Work with your accountant to identify which deductions in your situation qualify for lender add-backs. Bring that list when running calculator scenarios.

## Debt-to-Income Ratio: The Magic Number for Approval

Lenders use your debt-to-income ratio (DTI) more than any other metric in approval decisions. Your DTI compares your total monthly debt to your gross monthly income. If you earn $6,000 monthly and have $1,500 in existing debts, your DTI is 25% ($1,500 ÷ $6,000).

For 2026, conventional mortgages typically allow DTI up to 43%. FHA loans go up to 50%. Some non-QM lenders specializing in self-employed borrowers accept DTI up to 60%, though rates climb significantly at these levels.

When your calculator shows your DTI, it’s usually calculating this as housing debt plus existing obligations divided by gross income. Some calculators show “front-end DTI” (housing costs only) separately from “back-end DTI” (all debts including housing). Front-end is typically limited to 28%, while back-end is the 43-50% range.

If your calculator shows 45% DTI, you’re above conventional limits but within FHA and non-QM ranges. This matters because it tells you which lenders to approach. No point applying with a traditional bank if your DTI exceeds their limits; you need non-QM specialists who explicitly accept higher ratios.

## Income Calculation Methods and Their Impact

Self-employed income can be calculated multiple ways, and your calculator should offer options reflecting lender practices.

“Average” method takes your net income from the last two tax years, adds them, and divides by 24 months. If year one was $80,000 and year two was $100,000, this method uses $90,000 annually or $7,500 monthly. Most traditional lenders use this method.

“Most recent” method uses your most recent year’s tax return income. If year two (most recent) was $100,000, this method uses that figure. Lenders use this for borrowers with clearly increasing income trajectories.

“Bank statement” method calculates based on your actual deposits rather than tax-reported income. Lenders taking this approach examine 12-24 months of business bank statements and average your monthly deposits. If statements show consistent $8,500 monthly deposits, they use approximately $102,000 annual income.

Run scenarios with all three methods. You’ll often see the largest qualifying income using bank statement averaging, medium amounts with most-recent-year methods, and sometimes lower figures with two-year average (if your income recently dropped). Understanding all three helps you know which lenders to pursue.

## Credit Score Impacts on Mortgage Approval and Rates

While calculator results shouldn’t theoretically change based on credit score (the math doesn’t), interest rates absolutely do. Seeing what different scores mean for your actual monthly payment is valuable.

Current 2026 mortgage rates for self-employed borrowers roughly follow these patterns: credit score 740+, about 5.8-6.2% depending on loan type; score 700-739, about 6.2-6.6%; score 680-699, about 6.6-7.0%; score 660-679, about 7.0-7.5%; score below 660, typically 7.5%+.

On a $300,000 mortgage, the difference between 6% and 7% is roughly $180 monthly, or $2,160 annually. Over 30 years, that compounds to about $64,000 in additional interest paid. This illustrates why improving your credit score before applying genuinely matters.

If your calculator shows you qualify for a $350,000 mortgage but at your current 650 credit score the payment feels tight, consider delaying application three to six months while improving your score. Even reaching 680-690 might improve your rate by 0.5%, potentially saving $130+ monthly.

## Variables Affecting Self-Employed Mortgage Approval

Beyond the numbers, real lenders consider factors calculators can’t fully model. Understanding these helps you interpret calculator results realistically.

Length of self-employment matters enormously. Most lenders require two years minimum; some want three. If you’ve been self-employed for 18 months, no calculator can predict approval. But understanding what lenders will see at 24 months (your two-year mark) helps you plan.

Business stability indicators like consistent clients, multi-year contracts, or diversified income streams all improve approval odds even with identical financial numbers. Calculators can’t capture this. A freelancer with three major corporate clients retaining them annually is stronger than someone with the same income from dozens of one-time gigs, though numbers look identical.

Recent significant changes in business structure or ownership affect approval. If you recently incorporated, changed your business model dramatically, or shifted from one business to another, lenders scrutinize more carefully even with strong numbers. Calculators don’t know about these flags.

Income trends matter. Growing income shows strength; declining income raises flags. If your calculator input shows $95,000 in year two income but your business is now generating $110,000, mention this upward trajectory to lenders. Conversely, if numbers show decline, address it proactively.

## Multiple Calculator Scenarios: Finding Your Range

Rather than trusting one calculator run, effective planning involves multiple scenarios showing your approval range.

Run conservative scenarios assuming lower income, no add-backs, and current interest rates. This shows your “worst case” approval likelihood. If even conservative scenarios show good approval odds, you’re in strong position.

Run moderate scenarios with realistic income figures, modest add-backs, and current rates. This is your probable approval scenario.

Run optimistic scenarios with higher income figures (perhaps current-year income if it’s higher than your two-year average), generous add-backs, and slightly better-than-current rates. This shows your best-case approval scenario.

The gap between conservative and optimistic often tells you whether you’re clearly approvable or borderline. If conservative scenarios show $300,000 buying power and optimistic shows $350,000, you’re clearly in the $300k-325k range realistically. If conservative shows $250k and optimistic $400k, you’re in a wide range and should talk to actual lenders to narrow it.

## Using Calculators to Plan Your Mortgage Timeline

Beyond immediate approval, calculators help you plan. If current numbers suggest $320,000 buying power but you want $400,000, can you improve your situation?

Increasing income is the most powerful lever. If each $10,000 in additional annual income increases your approval by approximately $35,000-40,000, adding $20,000 in business income gets you $70,000-80,000 closer to your goal. This might mean waiting six months to 12 months while you grow revenue.

Decreasing debt is equally powerful. If you have $15,000 in credit card debt at $300 monthly payments, paying it off removes $3,600 annually from your required debt service. This alone might increase your approval by $100,000+.

Improving your credit score costs nothing but time. Run calculator scenarios at your current score, then at 700, 720, and 750. Seeing the rate differences (and thus payment differences) motivates the effort to improve score through on-time payments and lowered balances.

## Preparing Your Actual Lender Conversation

Once you’ve run calculator scenarios thoroughly, you’re ready for real lender conversations. Bring your calculators results with you or reference them confidently in phone conversations. Lenders respect borrowers who understand their own finances.

Tell the lender: “My calculator shows I should qualify for between $X and $Y based on my two-year average income. Can you tell me which income calculation method you use and what range that creates in your actual underwriting?”

Ask specifically: “Does your program accept bank statement qualifying? What about business expense add-backs?” Get specific answers about the method they’ll use, not just generic responses about self-employed lending.

Bring your detailed financial information: two years of tax returns, six to 12 months of business bank statements, and your most recent business profit-and-loss statement. Lenders will ask for these anyway, but bringing them proactively shows you’re prepared.

Understand the difference between pre-qualification (rough estimate) and pre-approval (conditional approval pending property appraisal). Your calculator provides pre-qualification estimates. After meeting with a lender and providing documentation, they’ll offer pre-approval numbers, which are much more reliable.

## Final Thoughts on Self-Employed Mortgage Calculators

A self-employed mortgage calculator is your starting point, not your final answer. Use it to understand what lenders might approve, what rates you might qualify for, and what factors most affect your specific situation. Use it to identify whether you should wait and improve your finances or proceed now.

Most importantly, use calculator insights to have informed conversations with actual lenders. When you understand your own numbers thoroughly, you negotiate better, avoid surprises, and make decisions confidently. Homeownership as a self-employed professional is genuinely achievable—the calculator just helps you see your path forward clearly.

## Frequently Asked Questions

Can I use current-year income on a mortgage calculator even though I haven’t filed taxes yet?

Most lenders require two years of filed tax returns. Calculators can show what your approval would be with current income, but actual lender approval requires documented tax returns. Use current-year estimates to see future potential, not current qualification.

How accurate is a mortgage calculator for self-employed people?

Calculators are accurate for rough estimates but shouldn’t be trusted as final numbers. Different lenders use different income calculation methods. Your actual approval might be 5-15% higher or lower depending on the specific lender you apply with.

What if my calculator shows I don’t qualify?

Try adjusting variables: lower your target loan amount, increase your down payment, add add-back income if applicable, or reduce existing debts. Then revisit. If still short, talk to a mortgage broker about non-QM options or timing your application after income improves.

Should I pay off debts before applying for a mortgage?

Typically yes, especially if your DTI is above 40%. Paying off a $5,000 credit card might improve your DTI by 2-3%, potentially increasing your approval by $50,000-75,000. The benefit usually outweighs waiting to pay after purchase.

How much can I improve my approval by increasing my down payment?

Every additional 1% down (roughly $3,000 on a $300,000 purchase) improves your approval odds and can increase your qualifying amount slightly. More importantly, it improves your rates and removes PMI requirements at 20% down.

Is bank statement qualifying really better for self-employed people?

Often yes, if your cash flow is strong and consistent. Bank statement qualifying ignores your tax returns entirely, which helps if deductions reduced your tax income below actual cash flow. However, you need consistent deposits showing steady income.