How social security vulnerability affects your self-employed retirement planning

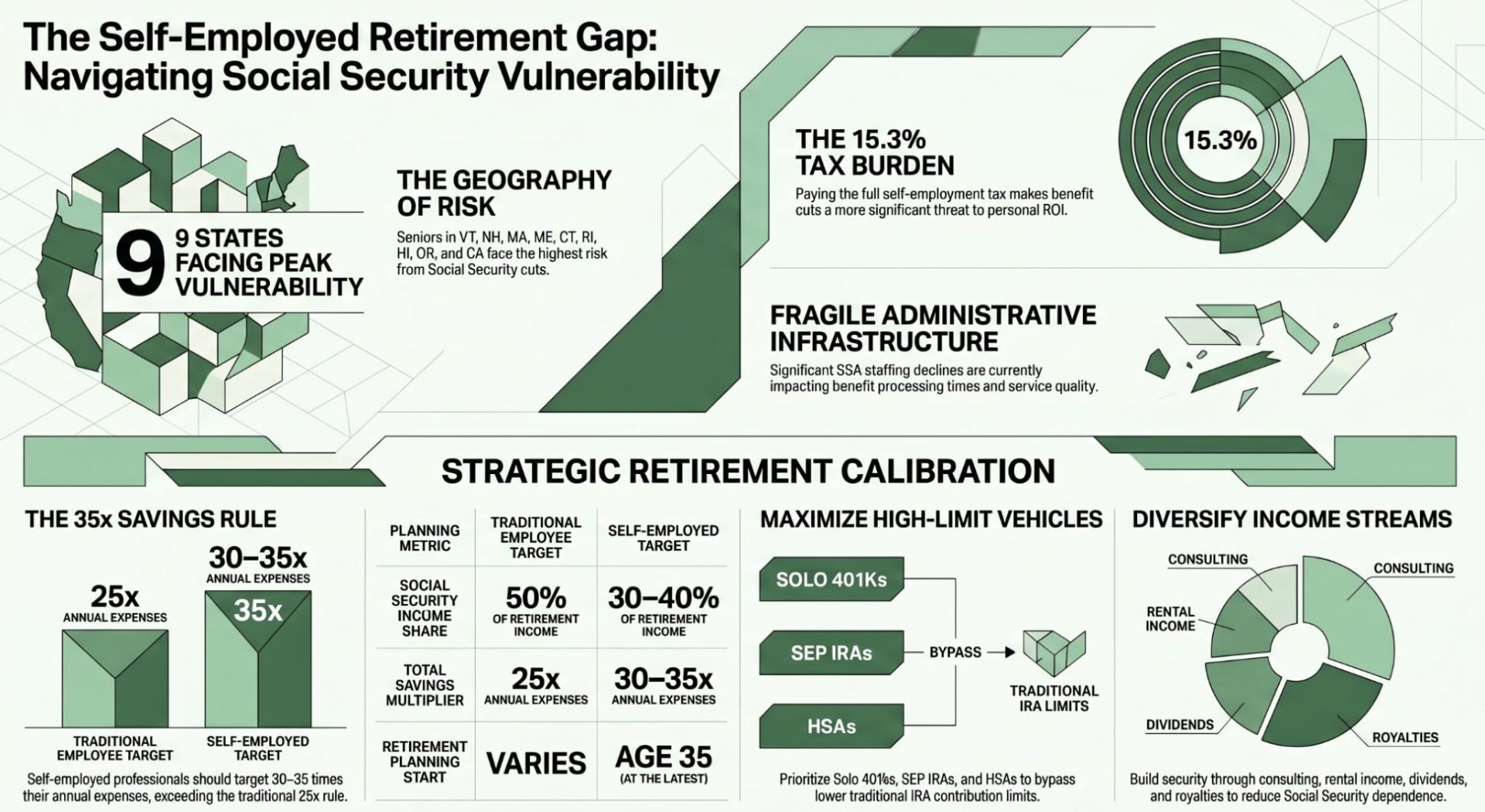

Recent research from Retirement Living has identified which states face the greatest vulnerability to social security cuts. Vermont, New Hampshire, Massachusetts, Maine, Connecticut, Rhode Island, Hawaii, Oregon, and California top the list. This data becomes especially significant for self-employed professionals who can’t rely on employer-sponsored pensions and must take personal responsibility for retirement security.

I’ve spent years helping self-employed professionals understand their unique retirement challenges. Unlike traditional employees who split Social Security contributions with employers, self-employed workers pay the full 15.3% self-employment tax. This higher contribution level makes Social Security cuts feel even more threatening to your retirement income security.

Understanding state-level social security vulnerability

The vulnerability analysis considers multiple factors: the proportion of seniors in each state’s population, economic conditions affecting the state’s ability to provide supplemental benefits, and the dependency rate of seniors on Social Security income. States with aging populations and lower average incomes show greater vulnerability because larger portions of their populations depend more heavily on Social Security benefits.

For self-employed professionals, this state-level analysis directly impacts your retirement planning. If you live in a vulnerable state, you need to assume a higher likelihood of reduced Social Security benefits or later retirement eligibility. This assumption should influence how much you save independently and how you allocate your retirement investments.

The broader context of SSA staffing challenges

Social Security Administration staffing has declined significantly, affecting benefit processing times and service quality. This context amplifies concerns about the program’s long-term viability. When an agency responsible for processing millions of claims faces budget constraints and staff reductions, the system becomes more fragile.

I view this staffing reality as a practical warning signal for self-employed professionals. The current system may not deliver benefits as smoothly or on the timeline you expect. Building sufficient retirement savings independently protects you from these systemic risks.

Why self-employed professionals face unique retirement challenges

Self-employed professionals lack the employer 401k matching that traditional employees receive. They also can’t rely on employer pension plans. The combination of higher self-employment taxes and greater responsibility for retirement savings creates a distinctive financial situation that requires careful planning.

The vulnerability of Social Security adds another layer of risk. Unlike an employee who might rely on Social Security as one of three retirement income sources (personal savings, employer pension, Social Security), self-employed professionals typically depend on only two sources: personal savings and Social Security. This concentration of risk means that any reduction in Social Security benefits creates a proportionately larger impact on your retirement income.

Strategic retirement planning for self-employed professionals

Given these vulnerabilities, I recommend that self-employed professionals pursue multiple retirement savings strategies simultaneously. A SEP IRA or Solo 401k allows you to save significantly more than traditional IRAs. Health Savings Accounts provide a powerful triple-tax advantage if you have a high-deductible health plan.

Beyond formal retirement accounts, building a taxable investment portfolio creates flexibility. While not tax-advantaged like retirement accounts, taxable investments offer accessibility before age 59.5 and can fund earlier retirement if you choose to leave self-employment before full Social Security eligibility.

Understanding self-employment tax rules and retirement contribution limits in your state helps you maximize your savings capacity. California self-employed professionals, for example, face state income taxes that reduce after-tax income available for retirement savings. This reality makes tax-efficient retirement planning even more important.

Calculating your retirement savings target

I work from a principle that self-employed professionals should plan for Social Security to provide 30-40% of target retirement income rather than the 50% many employees expect. This assumption requires building larger personal savings before retirement.

The traditional rule suggests needing 25 times your annual expenses in retirement savings. For self-employed professionals in vulnerable states, I’d recommend targeting 30-35 times your annual expenses. This higher target compensates for uncertainty about Social Security benefits while providing flexibility to retire early if desired.

Geographic considerations for self-employed professionals

The states identified as most vulnerable to Social Security cuts deserve special attention from self-employed professionals living in those regions. This vulnerability might factor into longer-term location decisions. Some self-employed professionals maintain flexibility to relocate as they approach retirement, potentially moving to states with lower cost of living and less vulnerable Social Security situations.

However, I recognize that most people can’t simply move for tax and Social Security reasons. The better approach involves acknowledging the vulnerability and planning accordingly through more aggressive retirement savings and diversified income sources.

Building diversified retirement income streams

Rather than relying primarily on Social Security, self-employed professionals should develop multiple income sources in retirement. Some possibilities include part-time consulting or freelance work that generates ongoing income, rental income from investment properties, dividend income from diversified investment portfolios, royalties from intellectual property or past work, and passive income from digital products or courses.

I’ve observed that the self-employed professionals who feel most secure in retirement are those who maintained the ability to generate income through their expertise even after formally retiring. This flexibility protects against Social Security uncertainty while maintaining mental engagement.

Tax optimization in your retirement plan

Self-employed professionals can use tax-advantaged retirement accounts to reduce current taxable income while building retirement savings. This double benefit makes retirement saving especially important. Proper bookkeeping and accounting ensures you capture all available retirement contributions and tax deductions.

Working with a tax professional who understands self-employment becomes increasingly valuable as your business grows. The right structure for retirement contributions can save thousands in taxes annually while building wealth systematically.

State-specific planning for vulnerable areas

If you live in Vermont, New Hampshire, Massachusetts, Maine, Connecticut, Rhode Island, Hawaii, Oregon, or California, consider state-specific retirement challenges. Some states offer additional retirement savings programs or tax advantages for certain types of retirement accounts. Understanding these options helps you optimize your retirement strategy.

California, for instance, has specific rules about self-employment income and retirement planning. Knowing these rules helps you structure your retirement savings most effectively.

Timeline for building retirement security

I recommend that self-employed professionals begin intentional retirement planning by age 35 at the latest. Starting earlier provides more time to benefit from compounding growth. Even small regular contributions, starting in your late 20s or early 30s, can grow into substantial retirement wealth over 30-35 years.

If you’re starting retirement savings later in your self-employed career, don’t despair. Catch-up contributions and the ability to save a large percentage of business income can accelerate wealth building. However, the earlier you start, the easier the process becomes.

How much should self-employed professionals save for retirement?

Plan to save 30-35 times your annual expenses given Social Security uncertainty. This is higher than the 25x rule for traditional employees because you can’t rely on employer pensions. Use tax-advantaged accounts like SEP IRAs or Solo 401ks to maximize savings capacity.

Why are some states more vulnerable to Social Security cuts?

States with aging populations and higher senior dependency rates face greater vulnerability. Vermont, New Hampshire, Massachusetts, Maine, Connecticut, Rhode Island, Hawaii, Oregon, and California show the highest vulnerability due to demographic and economic factors.

Which retirement accounts should self-employed professionals prioritize?

Solo 401ks and SEP IRAs allow much higher contributions than traditional IRAs. Health Savings Accounts provide triple-tax advantages if you have a high-deductible health plan. Taxable investment accounts add flexibility for early retirement access.

How should I factor Social Security into retirement planning?

Plan conservatively by assuming Social Security provides only 30-40% of your retirement income rather than 50%. This conservative assumption protects you if benefits are reduced while allowing flexibility if benefits are higher than expected.

Can self-employed professionals create multiple income streams in retirement?

Yes. Many self-employed professionals develop rental income, investment portfolios, part-time consulting, digital product royalties, or intellectual property income. These streams reduce Social Security dependence while maintaining engagement and flexibility.

At what age should self-employed professionals start retirement planning?

Begin by age 35 at the latest, though earlier is better. Starting in your late 20s or early 30s maximizes compounding growth. Even if you start later, catch-up contributions and the ability to save significant percentages of business income can accelerate retirement wealth building.