Hello again—Elliot here. Over my years running selfemployed.com, I’ve counseled countless business owners facing the toughest financial scenario: being self-employed AND having bad credit. The combination feels like a double burden when you’re trying to secure financing. But here’s what I’ve learned: bad credit doesn’t mean no credit. There are real, accessible options in 2026 if you know where to look and how to position yourself. This guide cuts through the noise and gives you honest, practical strategies.

The Reality of Bad Credit and Self-Employment

When you combine self-employment with bad credit, lenders see compounded risk. Self-employment alone is perceived as income volatility. Bad credit alone signals past payment problems. Together, they create the profile of “highest risk.” But this doesn’t mean you can’t borrow.

Understanding this perception is the first step. Lenders aren’t being unfair; they’re managing risk based on historical data. Self-employed borrowers do default at higher rates than W-2 employees (though not dramatically). Bad credit borrowers do default at higher rates than good credit borrowers. Therefore, a self-employed person with bad credit presents statistically higher risk.

Your job is to overcome this perception with evidence that you’re not the statistical average. You’ve recovered from whatever caused your bad credit. Your business is stable or growing. You have cash flow to service debt. These narratives, supported by documentation, matter.

What Constitutes “Bad Credit”?

Bad credit typically means a FICO score below 620. The score ranges are:

Excellent: 750-850

Good: 670-749

Fair: 580-669

Poor: 300-579

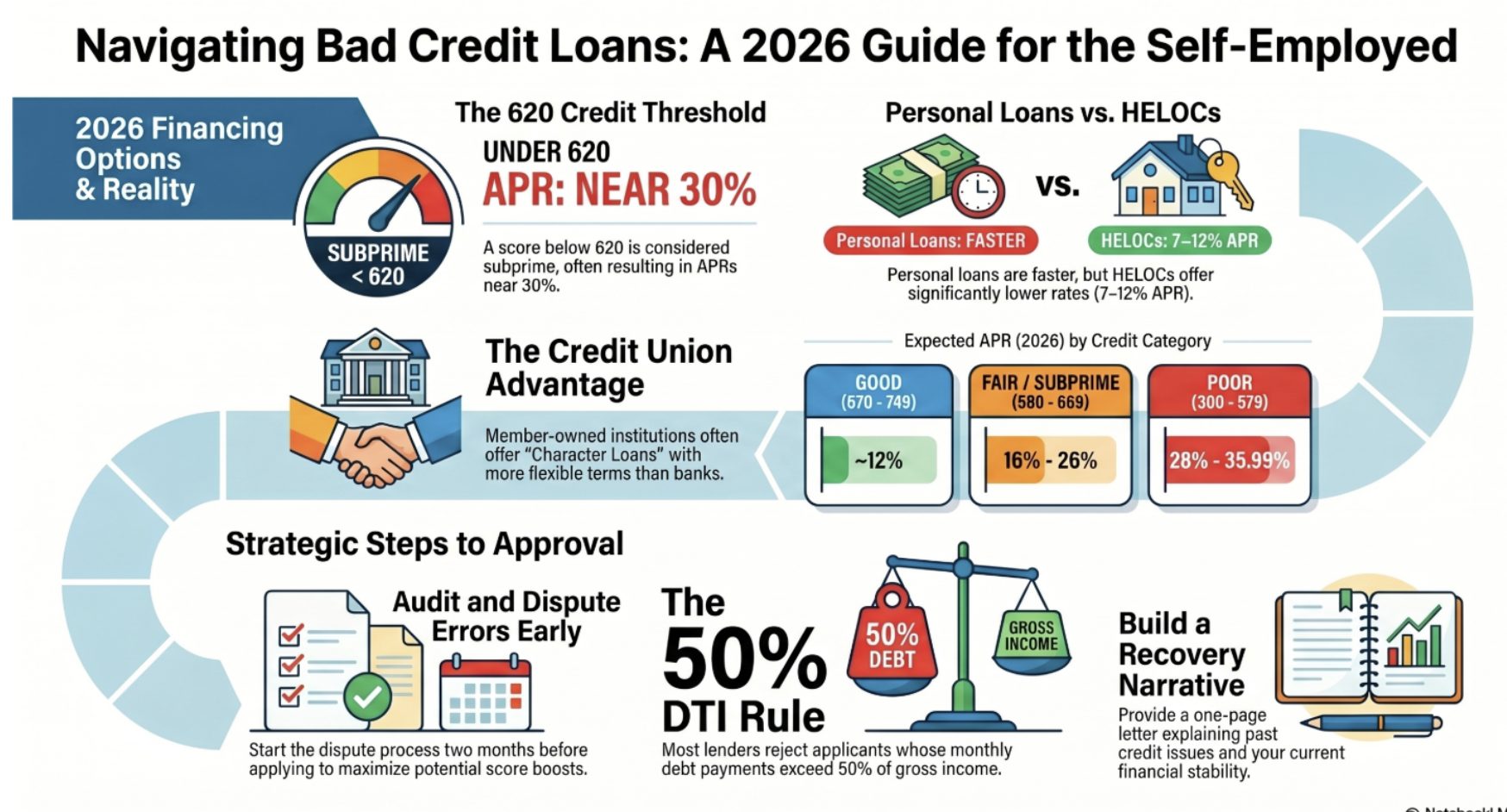

If your score is 620-650, you’re in “subprime” territory—not great, but not catastrophic. Many lenders still engage with this range. Below 600 becomes genuinely difficult.

Your credit score reflects five factors: payment history (35%), credit utilization (30%), length of credit history (15%), credit mix (10%), and new inquiries (10%). If you’re self-employed, your income volatility doesn’t directly affect your score. Your score reflects whether you’ve paid past debts on time.

2026 Bad Credit Loan Options for Self-Employed Borrowers

Personal Loans: The Most Flexible Option

Personal loans are typically unsecured (no collateral required) and available from banks, credit unions, and online lenders. For borrowers with bad credit, interest rates in 2026 range from approximately 8.99% to 35.99% APR depending on the lender and your specific profile. Prosper, a major peer-to-peer lender, charges 8.99% to 35.99% APR with terms from two to five years and origination fees from 1% to 9.99%.

For the average self-employed person with bad credit (say, a 580-620 score), expect rates in the 24-36% APR range. This is expensive, but the advantage is speed and accessibility. Many online lenders can fund loans in 1-3 business days.

Personal loans work best when you need a smaller amount ($5,000-$25,000) for a specific purpose. Using the loan to pay off higher-interest debt can actually improve your financial position, despite the seemingly high rate.

Installment Loans: Accessible and Structured

Installment loans are similar to personal loans but often available from lenders that specialize in subprime borrowing. These loans break repayment into fixed monthly installments, which is psychologically easier to manage than other forms of debt.

Minimum credit score requirements vary: some lenders accept 500-560, while traditional lenders require 629+. SBA-affiliated lenders typically want 650-675. Alternative lenders like Fundbox approve applicants with scores as low as 500.

For self-employed borrowers, lenders evaluate income by reviewing 12-24 months of bank statements to calculate average monthly income. They’re looking for consistency. If your business income has grown or stabilized over recent months, that’s compelling.

Home Equity Loans or HELOCs: Lower Rates, Higher Risk

If you own a home with equity, this is worth serious consideration. Home equity loans and home equity lines of credit (HELOCs) are secured by your home’s equity, so interest rates are dramatically lower—typically 7-12% APR even with bad credit, compared to 24-36% for unsecured personal loans.

The tradeoff is obvious: you’re putting your home at risk. If you default, the lender can foreclose. This only makes sense if you’re confident in your ability to repay.

For self-employed borrowers, home equity loans have two advantages: (1) lenders care less about the source of your income because they have security, and (2) rates are low enough that the loan actually improves your financial position.

Credit Union Loans: The Overlooked Advantage

Credit unions are member-owned financial institutions with different incentive structures than banks. They’re often more flexible with self-employed members and members with fair credit. Even if you’ve been denied elsewhere, ask your credit union specifically about bad credit personal loans or flex loans.

Credit unions sometimes offer “Character Loans” or “Credit Builder Loans” designed specifically for members rebuilding credit. These loans have higher rates than prime lending but significantly lower than online subprime lenders. Plus, credit union lenders often will have real conversations with you, whereas online lenders are purely algorithmic.

Interest Rates in 2026: What to Expect

Here’s the harsh truth: bad credit borrowers in 2026 face APR ranges of 32-36% for the worst-case scenarios. But there’s a spectrum.

A self-employed borrower with a 600-620 credit score, 2+ years of documented income, and solid bank statements might qualify for 20-26% APR with an online lender or 16-20% with a credit union.

Someone with a 560 score or less than 2 years of self-employment history might face 28-35% APR.

For context, the average personal loan rate in 2026 for someone with a 700 credit score (good credit) is approximately 12%. You’re paying a premium for bad credit, roughly 10-24% higher rates than a good-credit borrower would receive.

Shop Multiple Lenders: Rate Variation is Substantial

One lender might offer 28% APR while another offers 22% for the identical borrower. This isn’t a mistake; it’s risk tolerance variation. Online lenders use different algorithms, have different cost structures, and target different borrower segments.

Check at least 3-5 lenders before committing. Most allow you to check rates with a soft credit inquiry, which doesn’t damage your score. This takes 30 minutes and could save you thousands in interest over the loan term.

Qualification Steps for Self-Employed with Bad Credit

Step 1: Audit Your Credit Report

Before applying, pull your credit reports from all three bureaus (Equifax, Experian, TransUnion) at AnnualCreditReport.com. Look for:

Errors: Accounts you don’t recognize, incorrect account status, wrong payment history. Dispute these immediately with the bureau. Errors sometimes boost scores 20-50 points.

Antiquated accounts: Items from 7+ years ago shouldn’t be on your report. Request deletion.

Accounts in your name that aren’t yours: Sign of identity theft. Dispute immediately.

Recent activity: Are recent payments being reported correctly? Ensure that any good payment history from the last 12 months is showing.

Disput errors take 30-45 days to resolve, so start this process 2+ months before you need the loan.

Step 2: Organize Your Income Documentation

Gather:

Two years of personal tax returns (Form 1040 with all schedules)

Two years of business tax returns (Schedule C, Form 1120, K-1s as applicable)

Twelve months of business bank statements

Six months of personal bank statements

Year-to-date profit and loss statement (if it’s mid-year)

Business license or Articles of Incorporation

Self-employed lenders will scrutinize these documents. Make sure they’re organized, clearly labeled, and easy to follow. If your business is newer than two years, include documentation showing business legitimacy: client contracts, invoices, or a business plan.

Step 3: Calculate Your DTI Honestly

Your debt-to-income ratio is what lenders care about most. Add up all monthly debt payments (mortgage, car loan, credit cards at minimum payment, student loans, etc.) and divide by your gross monthly income.

For bad credit borrowers, a DTI above 50% is problematic. Some lenders will go to 60%, but only with compensating factors like substantial savings or a co-signer.

If your DTI is too high, you have three options:

1. Pay down existing debts before applying

2. Increase documented income (more on this below)

3. Reduce the loan amount you’re requesting

Step 4: Build Your Narrative

Write a one-page letter explaining:

What caused your bad credit (job loss, medical emergency, business downturn). Take responsibility but contextualize.

How you’ve recovered since then (new income sources, payment consistency over the last year, business growth).

Why you need this loan (legitimate business or personal expense).

Why you’re a good risk today despite past problems.

Lenders read these. They humanize you. A narrative that shows self-awareness and recovery is genuinely persuasive.

Step 5: Shop and Compare

Apply with multiple lenders simultaneously (within a 14-day window to minimize credit score impact). Compare:

APR (not just interest rate—APR includes fees)

Loan term and monthly payment

Origination fees

Prepayment penalties (avoid lenders with these)

Funding timeline

Customer reviews on independent sites (Trustpilot, Google Reviews)

Then choose the best option.

Strategies to Improve Approval Odds

Get a Co-Signer

A co-signer with good credit and stable income dramatically improves approval odds and rates. If a lender offers you 32% APR solo but 18% APR with a co-signer, the savings are substantial. The co-signer assumes responsibility if you don’t pay, so choose someone who understands the risk and is willing to help.

Consider a Secured Loan

If you have a vehicle, savings account, or investment account, some lenders will provide loans secured against these assets. Rates are lower, approval odds are higher, but you risk losing the asset if you default.

Increase Your Down Payment or Collateral

If you’re borrowing to purchase something (car, equipment), offering a larger down payment reduces the lender’s risk exposure. This can improve your approval odds and rates by 2-4%.

Wait 6-12 Months (If Possible)

Every month of on-time payments improves your credit score by 2-5 points. Every year of consistent payment history is powerful. If you don’t need the money immediately, waiting allows your credit to recover somewhat. A 600 score that becomes 620 over 12 months significantly improves your lending options.

Red Flags: Loans to Avoid

Not all bad credit loans are created equal. Avoid:

Payday loans: These trap you in cycles of debt. Interest rates exceed 400% APR in many states. They prey on self-employed people with desperate cash flow situations.

Title loans: Borrowing against your vehicle’s title exposes you to losing your car. Rates are often 25-40% with short terms, making default likely.

Lenders requiring upfront fees: If a lender asks you to pay an “application fee” or “processing fee” upfront before approval, it’s likely a scam. Legitimate lenders deduct fees from your loan proceeds.

Predatory online lenders: Some online lenders target self-employed people specifically with extremely high rates (50%+) or unnecessary add-ons. Check independent reviews.

Lenders who won’t discuss their terms clearly: Legitimate lenders explain APR, fees, and term transparently. Vagueness is a red flag.

Alternative Financing for Self-Employed with Bad Credit

Peer-to-Peer Lending

Platforms like Prosper, LendingClub, or Upstart connect borrowers with individual investors. These platforms sometimes approve lower-credit borrowers that banks reject. Rates vary widely (8%-35%+ APR), so rates aren’t always better, but approval odds are sometimes higher.

Credit Card Cash Advances

If you have access to a credit card, a cash advance is instantaneous and requires no approval. But interest rates are typically 25-30% APR, which is equal to or worse than personal loan rates, without the fixed payment schedule. Use only in emergencies.

Business Lines of Credit

Some lenders offer small business lines of credit with minimal credit requirements (550+). These are structured as credit lines, not loans, so you pay interest only on what you draw. If you have a business, this can be useful.

Borrow from Friends or Family

If possible, this is often your cheapest option. Establish a written agreement with terms, even with family. This protects both parties and demonstrates seriousness. Interest rates can be low (2-5%) or zero, which beats any third-party lender.

SBA Disaster Loans

If you’re a self-employed business owner affected by a declared disaster, SBA disaster loans exist specifically for your situation. These have favorable terms and minimal credit requirements. Check SBA.gov to see if you qualify.

Managing Loan Payments with Irregular Income

Set Automatic Payments

Regardless of your income variability, set up automatic payments from your business account on the day you typically receive payments. This prevents missed payments, which further damage your credit.

Budget for Worst-Case Cash Flow

If your business typically has slow months, budget for the loan payment during those slow months. Only borrow an amount your worst-case income can cover. Self-employed people who borrow at their peak income often struggle when income dips.

Use Loan Payoff to Build Credit

Even an expensive bad credit loan can rebuild your credit if you make consistent, on-time payments. After 12 months of perfect payment history, your score might improve 40-60 points. After 24 months, another 40-60 points. Using a bad credit loan strategically as a credit-building tool can be smart.

Frequently Asked Questions

What credit score do I need to qualify for a bad credit personal loan in 2026?

Most lenders accept scores as low as 500-560, though rates are better at 600+. Some online lenders accept scores below 500. Credit unions sometimes approve members with lower scores than traditional lenders. Your credit score is important, but it’s not the only factor—self-employment income documentation matters equally.

How much interest will I pay on a bad credit personal loan if I’m self-employed?

Interest rates range from 8.99% to 35.99% APR depending on the lender and your specific profile. Most self-employed borrowers with bad credit (580-620 score) qualify for 20-30% APR. Better credit or larger down payments lower this. Online lenders tend to charge higher rates than credit unions.

Can I get a loan if I’ve been self-employed for less than two years?

Yes, but with higher scrutiny. Provide whatever documentation you have: one year of tax returns, business license, bank statements, client contracts, or a CPA letter. Some lenders will approve newer business owners, especially if income is documented and stable. Bad credit makes this harder, so a co-signer helps significantly.

Is a home equity loan better than a personal loan if I have bad credit?

Home equity loans offer dramatically lower rates (7-12% vs. 24-36%), making them attractive if you own a home with equity. But you’re risking your home. Only pursue this if you’re confident you can repay. If your business is very volatile or income is uncertain, the security of a personal loan (without home risk) might be worth the higher rate.

How much should I borrow if I’m self-employed with bad credit?

Borrow only what you need and what your documented income can cover during slow business months. If you typically earn $4,000/month and have $2,000 in other debts, a $400/month loan payment works. A $800/month loan payment leaves you exposed to default risk during down months. Conservative borrowing is critical when self-employed.

Should I use a bad credit loan to consolidate higher-interest debt?

Sometimes. If you’re paying 35% APR on credit cards and can get a personal loan at 26% APR, consolidation saves money despite the “bad credit” label. However, if consolidation only slightly lowers your rate and extends your repayment timeline, the total interest paid might be similar or higher. Run the math before consolidating.