Having worked with self-employed professionals across the Midwest for years, I find Illinois to be one of the more straightforward states when it comes to tax planning. The state’s flat 4.95% income tax rate means there are no surprises as your income grows, unlike the progressive bracket systems in neighboring states. That simplicity is a real advantage for freelancers and independent contractors who are trying to forecast their tax obligations. Of course, the 15.3% federal self-employment tax still applies, and Illinois does have some unique considerations around local requirements and business registration that can trip up newcomers. I have helped freelancers in Chicago, the suburbs, and downstate communities navigate these obligations, and the consistent theme is that a clear understanding of both the federal and Illinois-specific rules leads to fewer headaches at tax time.

Self Employment Tax Calculator

What Is Self-Employment Tax in Illinois?

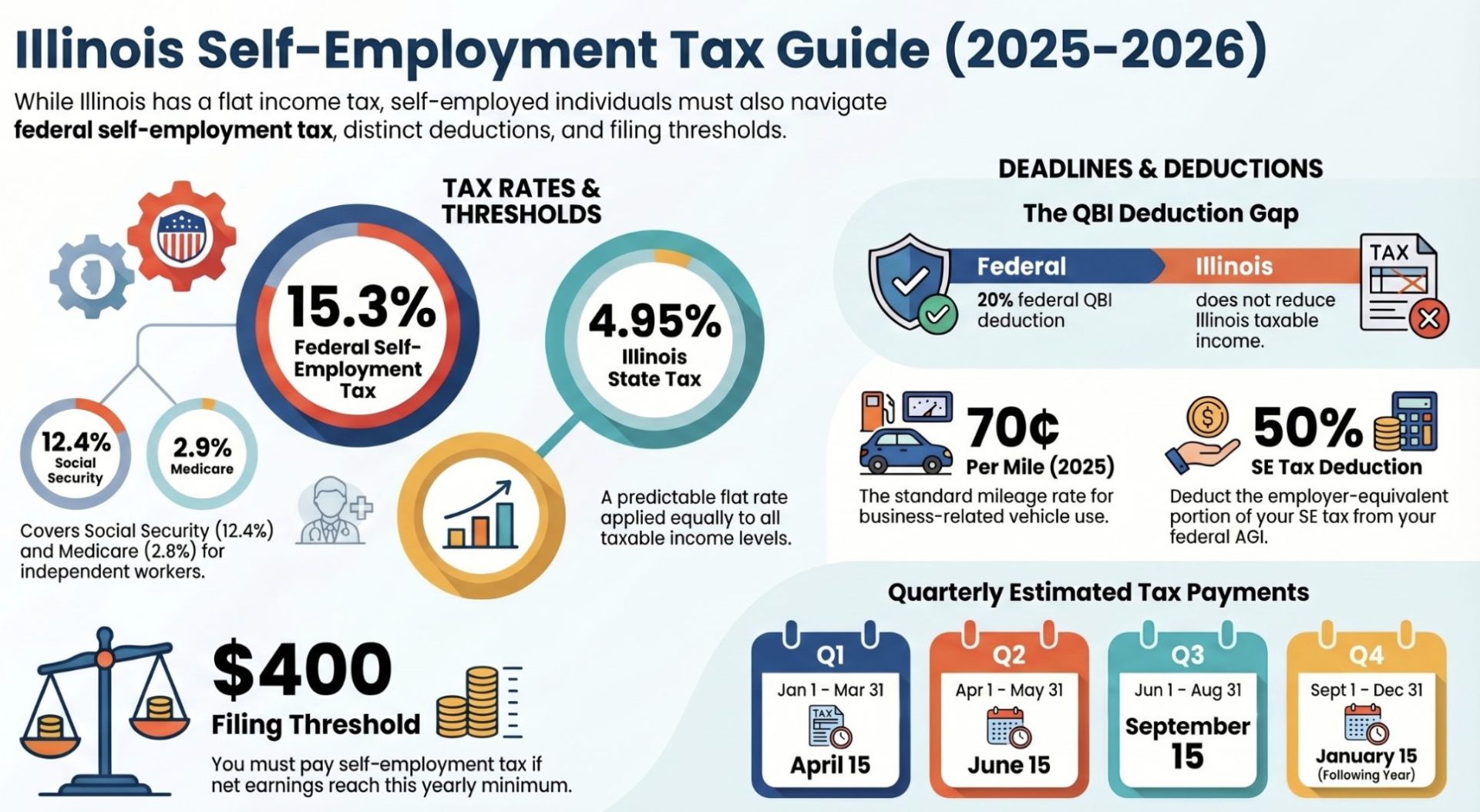

Self-employment tax is the federal tax that independent workers pay to fund Social Security and Medicare. When you work for an employer, these contributions are split evenly between you and the employer at 7.65% each. When you are self-employed, you cover the entire 15.3% yourself, with 12.4% going to Social Security and 2.9% to Medicare.

The Social Security portion applies to net self-employment earnings up to the annual wage base, which is $176,100 for 2025 and $184,500 for 2026. Earnings above those thresholds are not subject to the Social Security tax. The Medicare tax applies to all net self-employment earnings without any cap. If your net earnings exceed $200,000 as a single filer or $250,000 filing jointly, an additional 0.9% Medicare surtax applies to the excess.

You can deduct the employer-equivalent portion of your self-employment tax, which is 7.65%, from your adjusted gross income on your federal return. This is an above-the-line deduction available regardless of whether you itemize. You must pay self-employment tax if your net self-employment earnings are $400 or more in a tax year.

Illinois does not impose a separate state self-employment tax. Your self-employment income flows through to your Illinois state return and is taxed at the state’s flat income tax rate.

Illinois State Income Tax for the Self-Employed

Flat Tax Rate

Illinois has maintained a flat individual income tax rate of 4.95% since 2017. Unlike states with progressive brackets, this rate applies equally to every dollar of taxable income regardless of how much you earn. For self-employed individuals, this means your tax calculation is simple: multiply your Illinois taxable income by 4.95%.

The flat rate provides predictability that is especially useful for freelancers with variable income. Whether you earn $40,000 or $400,000 in net self-employment income, the Illinois rate stays the same. This stability has been maintained through the 2025 and 2026 tax years, with proposed rate increases deferred during budget reviews.

Personal Exemptions

For the 2025 tax year, Illinois provides a personal exemption of $2,850 per person. For married couples filing jointly, the combined exemption is $5,700. However, these exemptions phase out at higher income levels: if your federal adjusted gross income exceeds $250,000 as a single filer or $500,000 for married filing jointly, you are not eligible for the exemption.

Filing Requirements

Self-employed individuals file their Illinois state return using Form IL-1040. The starting point is your federal adjusted gross income, which is then modified by Illinois-specific additions and subtractions to arrive at your Illinois base income. The filing deadline is April 15, aligning with the federal deadline. Illinois requires estimated tax payments if you expect your tax liability to exceed $400 after withholding and credits.

Illinois also imposes a replacement tax on partnerships and S corporations at 1.5%, which is relevant if you have structured your freelance business as one of these entities rather than operating as a sole proprietor.

How to File Self-Employment Taxes in Illinois

Filing in Illinois requires coordinating your federal and state returns. On the federal side, you report your business income and deductible expenses on Schedule C (Form 1040), which produces your net profit. That figure carries to Schedule SE where your 15.3% self-employment tax is calculated. The deductible half of your SE tax reduces your federal adjusted gross income.

For Illinois, you file Form IL-1040 using your federal AGI as the starting point. Illinois applies its own adjustments, including additions for certain items that were deducted federally but are not recognized by the state, and subtractions for items like retirement income that Illinois exempts. The resulting base income is multiplied by the flat 4.95% rate to determine your state tax liability.

If you made estimated payments during the year using Form IL-1040-ES, those are credited against your final state tax. Illinois accepts electronic filing through its MyTax Illinois portal.

Clients who paid you $600 or more should provide a Form 1099-NEC. You are responsible for reporting all self-employment income regardless of whether you received a 1099. The Illinois Department of Revenue cross-references federal return data with state filings, so discrepancies will generate correspondence.

One consideration for Illinois freelancers is that local municipalities generally do not impose separate income taxes. Unlike Ohio, where municipal income taxes add a significant layer of complexity, Illinois self-employed individuals typically only need to worry about federal and state obligations. This simplifies the filing process considerably.

Quarterly Estimated Tax Payments in Illinois

Both the IRS and Illinois require self-employed individuals to make estimated tax payments throughout the year. Federal estimated payments are required if you expect to owe $1,000 or more in tax. Illinois requires estimated payments if your expected tax liability exceeds $400.

The quarterly due dates are:

| Payment Period | Due Date |

|---|---|

| January 1 – March 31 | April 15 |

| April 1 – May 31 | June 15 |

| June 1 – August 31 | September 15 |

| September 1 – December 31 | January 15 of the following year |

To calculate your quarterly payments, estimate your total annual net self-employment income, apply the 15.3% federal SE tax rate, add your expected federal income tax and Illinois state tax at 4.95%, subtract any withholding or credits, and divide by four. Use Form 1040-ES for federal payments and Illinois Form IL-1040-ES for state payments.

Illinois allows you to avoid underpayment penalties by paying at least 100% of your prior year’s state tax liability in four equal installments, or 90% of your current year’s expected liability. The safe harbor approach of using last year’s total works well for most freelancers and provides protection even if your income increases substantially.

Tax Deductions and Credits for Illinois’s Self-Employed

Maximizing deductions reduces both your federal and Illinois tax liability since Illinois uses your federal AGI as the starting point for its return. The 50% self-employment tax deduction automatically lowers your federal AGI, which flows through to reduce your Illinois taxable income as well.

The home office deduction is available through either the simplified method at $5 per square foot up to 300 square feet for a maximum of $1,500, or the actual expense method. Health insurance premiums for medical, dental, vision, and qualifying long-term care coverage are deductible from your federal AGI.

Retirement contributions to a SEP-IRA (up to 25% of net self-employment earnings) or Solo 401(k) reduce your taxable income dollar for dollar. At Illinois’s 4.95% rate, a $20,000 retirement contribution saves you $990 in state taxes on top of your federal savings.

The Qualified Business Income (QBI) deduction allows eligible self-employed individuals to deduct up to 20% of their qualified business income from their federal taxable income. This deduction is taken on Form 1040 and does not reduce your self-employment tax, but it can meaningfully reduce your federal income tax. Note that Illinois does not conform to the federal QBI deduction, so it does not reduce your Illinois taxable income.

Ordinary business expenses such as software, advertising, professional development, supplies, and professional service fees are deductible on Schedule C. Vehicle mileage is deductible at 70 cents per mile for 2025.

| Deduction Category | Details |

|---|---|

| Self-Employment Tax Deduction | 50% of SE tax, reduces federal AGI and IL taxable income |

| Home Office | Simplified: $5/sq ft (max $1,500) or actual expenses |

| Health Insurance Premiums | Medical, dental, vision, long-term care |

| Retirement Contributions | SEP-IRA (up to 25% of net SE income), Solo 401(k) |

| QBI Deduction | Up to 20% of qualified business income (federal only) |

| Business Expenses | Supplies, software, advertising, professional fees |

| Vehicle/Mileage | 70 cents/mile (2025) or actual vehicle expenses |

Avoiding Common Pitfalls

Forgetting About Illinois Estimated Payments

Many Illinois freelancers focus exclusively on their federal estimated payments and forget that Illinois also requires quarterly estimated payments if their state liability exceeds $400. The state’s underpayment penalty is calculated as interest on the shortfall, and while the amounts may seem small per quarter, they compound over the course of a year.

Misunderstanding the QBI Deduction at the State Level

The federal Qualified Business Income deduction of up to 20% is a powerful tool for reducing your federal income tax, but Illinois does not conform to this provision. Self-employed individuals who assume the QBI deduction reduces their Illinois taxable income will discover a larger state tax bill than expected. Make sure your tax planning accounts for this difference.

Not Registering Your Business Properly

Illinois requires businesses to register with the Secretary of State and may require additional registrations depending on your business type and location. If you sell taxable goods or services, you may need to register for a sales tax certificate with the Illinois Department of Revenue. Chicago imposes additional registration requirements and a higher sales tax rate than the rest of the state. Even if you are a service-based freelancer, understanding whether your specific services are subject to sales tax in Illinois can prevent compliance issues.

Poor Recordkeeping

Both the IRS and Illinois Department of Revenue require documentation to support your deductions. Maintaining organized records of all income, expenses, mileage, and home office use throughout the year is essential. Accounting software and separate business bank accounts make this process significantly easier and provide strong audit defense.

Final Thoughts on Self-Employment Tax in Illinois

Illinois’s flat 4.95% state income tax rate makes tax planning relatively straightforward for self-employed individuals. Combined with the 15.3% federal self-employment tax and federal income tax, your total tax burden is manageable compared to many states, especially given the absence of local income taxes in most Illinois communities. By maximizing your deductions, making timely estimated payments to both the IRS and the Illinois Department of Revenue, and understanding the nuances like the QBI deduction’s state-level treatment, you can keep your effective tax rate well under control. If your self-employment income exceeds $75,000 or your business structure involves an LLC or S Corp, working with an Illinois-based tax professional is a smart investment.

Frequently Asked Questions

What is the Illinois state income tax rate for self-employed individuals?

Illinois has a flat income tax rate of 4.95% that applies to all taxable income regardless of amount. This rate has been stable since 2017 and applies to self-employment income the same way it applies to wages. Combined with the 15.3% federal self-employment tax, Illinois freelancers face a total SE and state tax rate of about 20.25% before federal income tax.

When are quarterly estimated tax payments due in Illinois?

Quarterly estimated payments are due on April 15, June 15, September 15, and January 15 of the following year. These deadlines apply to both federal estimated payments (Form 1040-ES) and Illinois state estimated payments (Form IL-1040-ES). Illinois requires estimated payments if your expected tax liability exceeds $400.

Does Illinois have local income taxes for self-employed individuals?

No. Unlike some neighboring states such as Ohio, Illinois municipalities generally do not impose local income taxes on self-employment income. Your state tax obligations are limited to the flat 4.95% Illinois income tax filed on Form IL-1040.

What deductions can I claim as a self-employed person in Illinois?

You can deduct 50% of your self-employment tax, health insurance premiums, home office expenses, retirement contributions to a SEP-IRA or Solo 401(k), vehicle mileage at 70 cents per mile for 2025, and ordinary business expenses. The federal QBI deduction of up to 20% reduces your federal tax but does not reduce your Illinois state tax.

What forms do I need to file self-employment taxes in Illinois?

At the federal level, you need Schedule C (business income and expenses), Schedule SE (self-employment tax), and Form 1040. For Illinois, file Form IL-1040, the state individual income tax return. For estimated payments, use Form 1040-ES for federal and Form IL-1040-ES for Illinois state payments.

Does the Qualified Business Income deduction apply in Illinois?

The QBI deduction of up to 20% of qualified business income reduces your federal taxable income but Illinois does not conform to this provision. Your Illinois taxable income will be higher than your federal taxable income by the amount of the QBI deduction you claimed

Self-Employment Tax Guides by State

- Check out self-employment tax rates for Maine

- See the self-employment tax guide for Nebraska

- Learn about self-employment taxes in Ohio

- Explore self-employment tax rates for Vermont

- View the self-employment tax guide for Colorado

.