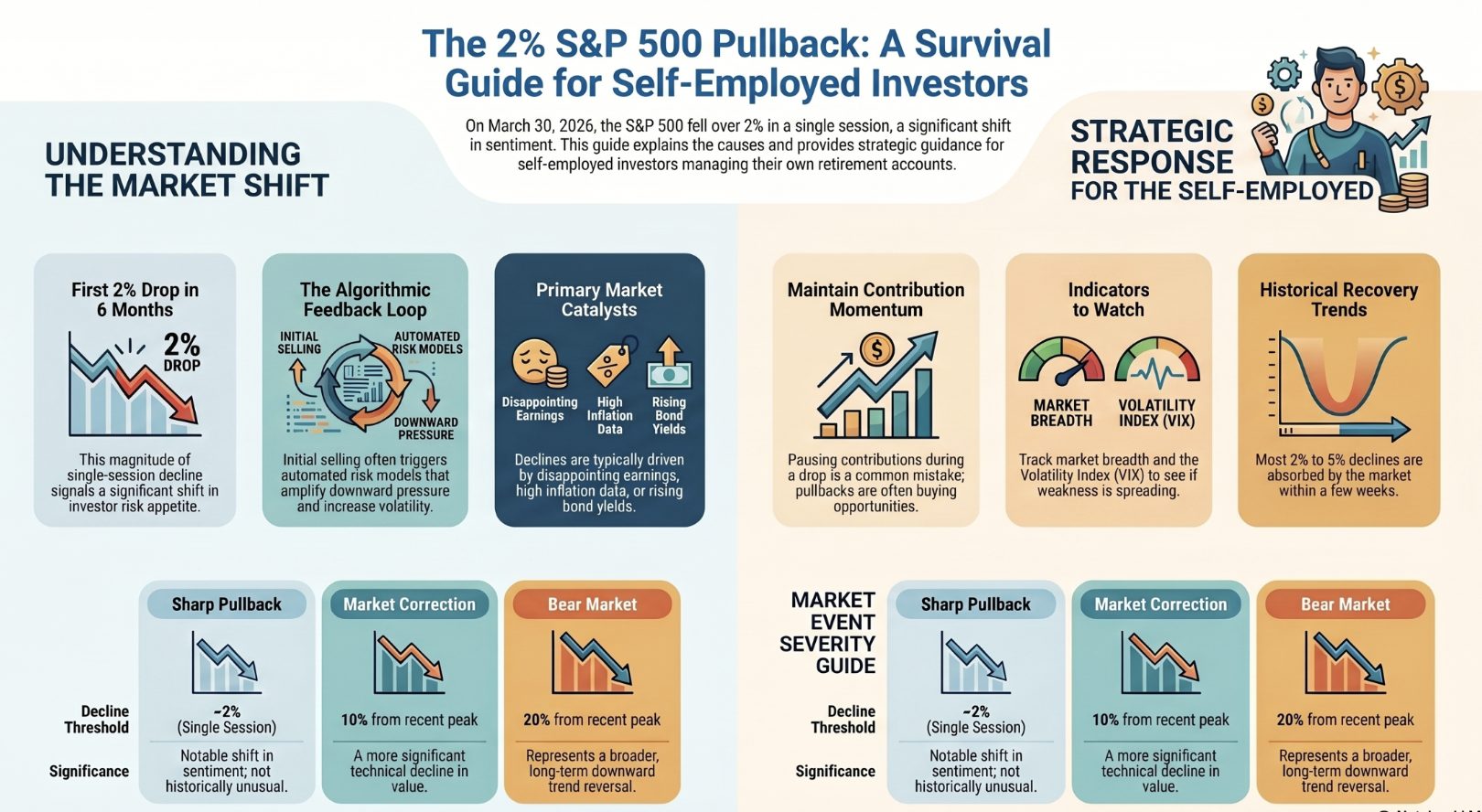

The S&P 500 fell more than 2% in a single session – the first such S&P 500 correction of that magnitude in six months – rattling investors who had grown accustomed to steady advances and muted volatility. The selloff hit broad swaths of the market and marked a clear shift in sentiment after a long stretch of momentum-driven gains.

For self-employed professionals and independent business owners who invest their own retirement funds, understanding what drives a sharp S&P 500 correction and how to respond matters more than it does for employees with employer-managed 401(k)s. You are your own financial planner. Decisions about your investments are entirely yours.

Why this S&P 500 correction matters

A 2% single-session decline, after six months without one, signals a change in market risk appetite. When gains stack up over months, even modest disappointments – in earnings guidance, inflation data, or Fed commentary – can trigger a rush to lock in profits. The resulting selloff then triggers algorithmic and risk-parity strategies that amplify the move before stabilizing.

Large pullbacks also expose where positioning is stretched. When passive inflows have pushed valuations to elevated levels, a single catalyst can set off a cascade of selling that looks dramatic even when the underlying economy remains sound.

“The S&P 500 slumped more than 2% for the first time in six months, rattling investors after a long stretch of gains.”

What typically drives sharp market declines

No single factor explains every sharp market decline. That said, traders consistently point to a familiar set of catalysts that converge and accelerate selling:

- Disappointing earnings or lowered guidance from market-leading companies.

- Inflation data coming in above expectations, pressuring interest rate outlooks.

- Rising bond yields that compress equity valuations, particularly in growth stocks.

- Geopolitical headlines that trigger a flight to safe-haven assets.

- Algorithmic selling as volatility thresholds breach and risk models activate.

When markets trend higher for extended periods, volatility measures fall and hedges are unwound. A sharp drop can then force those protections back on rapidly, adding to downside pressure. That feedback loop is why a “routine” 2% decline can feel sudden and disorienting.

How self-employed investors should think about S&P 500 corrections

Unlike salaried employees who contribute automatically to employer plans with no decisions required, self-employed professionals manage their own retirement and investment accounts. A Solo 401(k) or SEP-IRA means you decide contribution timing, asset allocation, and response to market volatility – all of it.

In my experience working with self-employed professionals, the biggest investing mistakes happen during sharp corrections. People pause contributions when prices drop – the exact opposite of what long-term wealth building requires. If you have been contributing consistently, a 2% pullback is not a reason to change course. It may actually be a reason to accelerate contributions if your cash flow allows.

The SEC’s investor education materials recommend maintaining a diversified, long-term portfolio strategy rather than reacting to short-term volatility. That guidance applies especially to self-employed investors without the behavioral guardrails of automatic enrollment.

Reading market signals after a sharp drop

Attention after a correction typically focuses on whether weakness broadens or fades. A few indicators are worth tracking:

- Market breadth: are most sectors declining, or just a few?

- Credit spreads: are corporate bonds pricing in economic stress, or just equity repositioning?

- Volume on down days versus up days: sustained high volume on selling days is more concerning than a single spike.

- Reactions to upcoming earnings and inflation data: the first major catalyst after a drop often determines direction for the following weeks.

Historical context: most S&P 500 corrections recover

Looking back across market history, the vast majority of 2% to 5% single-session declines have been absorbed within weeks as buyers return at lower prices. A minority have foreshadowed longer corrections – typically when they coincided with deteriorating economic data, tightening credit conditions, or a policy shift. The key question is always whether the shock is isolated or part of a broader trend reversal.

For self-employed professionals building wealth through their own investment accounts, the right framework is almost always the same: maintain your allocation, keep contributing, and review your plan with a fee-only financial advisor rather than reacting to headlines. Our guide to building sustainable income as a self-employed professional covers how to structure your finances to withstand market volatility.

What to watch in the sessions ahead

Near term, markets will look for signals about whether this is a short-lived shakeout or the start of a choppier phase:

- Upcoming Consumer Price Index (CPI) inflation data from the Bureau of Labor Statistics.

- Federal Reserve guidance on interest rate policy.

- High-profile corporate earnings reports from market-leading companies.

- Volatility index (VIX) behavior: sustained elevation signals ongoing uncertainty.

If credit markets remain calm and economically sensitive sectors hold up, equity weakness may prove temporary. If weakness spreads to funding markets or consumer credit, caution tends to persist longer.

Frequently asked questions

What causes an S&P 500 correction?

An S&P 500 correction can be triggered by disappointing earnings, inflation data above expectations, rising bond yields, geopolitical events, or a combination of factors. Sharp declines are often amplified by algorithmic selling once volatility thresholds are breached, turning an orderly pullback into a fast move lower before stabilizing.

Is a 2% S&P 500 drop significant?

In the context of normal market fluctuations, a 2% single-session decline is noteworthy but not historically unusual. It becomes more significant when it occurs after a long period of calm, as this one did – the first such drop in six months – because it signals a change in investor sentiment and risk appetite.

How should self-employed investors respond to a stock market correction?

Self-employed investors should generally maintain their contribution schedule and long-term asset allocation during corrections rather than pausing or making reactive changes. If anything, a pullback may represent an opportunity to accelerate contributions to a Solo 401(k) or SEP-IRA at lower prices. Consult a fee-only financial advisor before making significant allocation changes.

What is the difference between a correction and a bear market?

A stock market correction is typically defined as a decline of 10% or more from a recent peak. A bear market is a decline of 20% or more. A single-session drop of 2%, while significant in isolation, does not meet the technical definition of either – it is a sharp pullback that may or may not develop into a broader correction depending on subsequent data and market behavior.