After helping dozens of self-employed professionals with their finances, I’ve noticed a pattern: the same money myths appear again and again, holding people back from building the wealth they deserve. These aren’t small misconceptions – they’re fundamental beliefs about money that shape every financial decision you make. In this article, I’m going to debunk six hard truths about money myths that have quietly sabotaged the financial plans of countless entrepreneurs and self-employed workers.

Money myth #1: You need a high income to build wealth

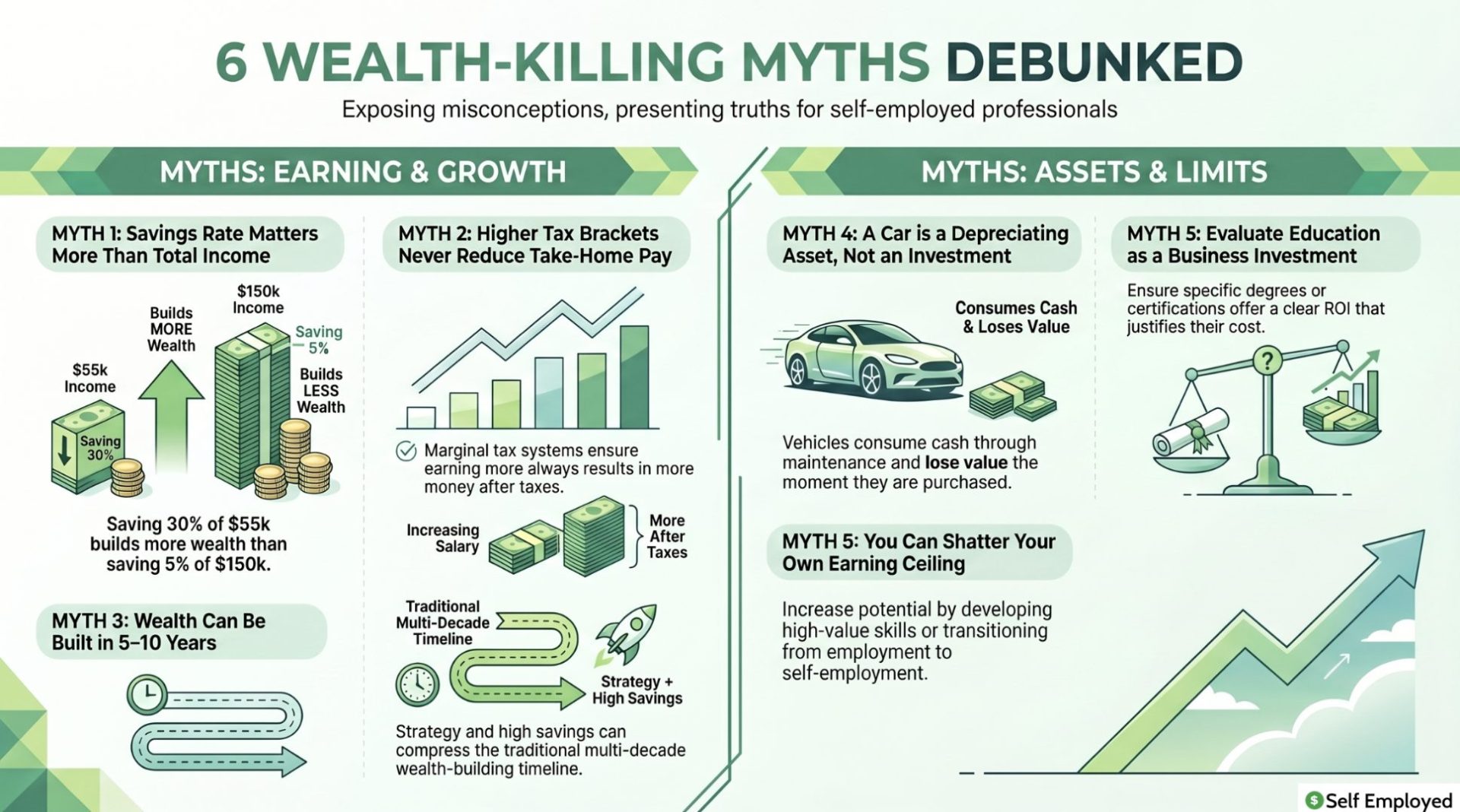

This is perhaps the most destructive money myth I encounter. Many people believe that building wealth requires earning six figures or more. The reality? I’ve worked with self-employed professionals earning $40,000 annually who’ve accumulated $200,000+ in assets, while I’ve also seen six-figure earners with negative net worth.

The difference isn’t income – it’s savings rate. A graphic designer earning $55,000 who saves 30% of their income will build more wealth than an executive earning $150,000 who only saves 5%. After helping business owners analyze their cash flow, I’ve consistently found that money myths about needing high income prevent people from focusing on what actually matters: the percentage of income they retain.

Your income is a tool, but your spending habits and investment discipline are the actual wealth-builders. Someone earning a modest income who invests consistently will outpace a high earner who spends everything they make.

Money myth #2: A college degree guarantees financial security

This money myth persists because it was partially true a generation ago. Today, the data tells a different story. According to the Federal Reserve, student loan debt now exceeds $1.7 trillion, and many degree holders struggle with negative cash flow for years after graduation.

In my experience working with self-employed professionals, some of the highest earners never completed a four-year degree. They pursued apprenticeships, certifications, or launched businesses directly. Meanwhile, others spent six years and $100,000 on education that led to modest-paying positions.

This doesn’t mean education is worthless – it means you need to evaluate education as a business investment. Will this specific degree, from this specific program, lead to earnings that justify the cost and time? For many fields, the answer is no. This money myth costs people hundreds of thousands of dollars because they never question the assumption that “everyone should go to college.”

Money myth #3: There’s a ceiling to how much you can earn as an employee

This money myth has both truth and deception. Yes, there’s an employment ceiling for most positions – a salary cap determined by your job title, experience, and company size. But many people believe this ceiling is much lower than it actually is.

After discussing finances with hundreds of self-employed workers, I’ve learned that most employees significantly underestimate their earning potential within their current employment. Negotiating raises, changing companies, and advancing to management positions can increase employee income dramatically without requiring entrepreneurship.

However, there IS a point where traditional employment caps out for most people. This is why some of my clients have transitioned to self-employment. The money myth here isn’t that an earnings ceiling exists – it’s that you can’t do anything about it. In reality, you have options: develop higher-value skills, move into management, or transition to self-employment and create your own income ceiling.

Money myth #4: Your car is an investment

This money myth costs the average American over $10,000 annually in vehicle expenses, and it’s rooted in a fundamental misunderstanding of what constitutes an investment. A car is a depreciating asset that consumes cash through payments, insurance, fuel, and maintenance. From the moment you drive it off the lot, it loses value.

I’ve worked with self-employed professionals who spend 20-30% of their income on vehicles while complaining they can’t save for retirement. The money myth that a car is an investment makes this seem acceptable. In reality, it’s consumption disguised as necessity.

This doesn’t mean avoiding cars entirely – transportation is often essential. But approaching your vehicle purchase strategically matters enormously. A three-year-old used car purchased for cash and maintained well is fundamentally different from financing a new vehicle every five years. The former is a practical expense; the latter is a wealth-draining mistake that this money myth enables.

Money myth #5: Building wealth takes decades

Yes and no. This money myth contains just enough truth to be dangerous. Building substantial wealth does take time, but the timeline depends entirely on your starting point and strategy. Some people build wealth in years instead of decades – not through get-rich-quick schemes, but through strategic decisions about income, savings, and investments.

In my experience consulting with self-employed professionals, those who combine three elements build wealth much faster: increasing their income through skill development, maintaining high savings rates, and investing in assets with strong cash flow potential. A freelancer who increases their hourly rate from $50 to $100 while simultaneously increasing their savings rate creates momentum that compounds rapidly.

The money myth that wealth-building necessarily takes decades paralyzes people into inaction. If you believe you have 30 years anyway, why start now? In reality, starting immediately and making strategic choices can cut that timeline in half. The best time to start building wealth was 20 years ago; the second best time is today.

Money myth #6: Tax brackets mean you shouldn’t earn more money

This money myth causes real financial harm. Many self-employed professionals deliberately limit their income because they believe earning more will push them into a higher tax bracket and they’ll “lose money.” This is mathematically impossible in the US tax system, which uses marginal tax brackets.

Here’s how it actually works: If you’re in the 22% tax bracket and earn one dollar more, you only pay 22 cents in federal taxes on that dollar. You don’t suddenly lose 22% of your entire income. Yet this money myth persists, and I’ve encountered multiple six-figure earners who’ve intentionally turned down work or clients because they feared tax consequences.

Understanding tax brackets is essential for self-employed professionals. The IRS website provides clear bracket information annually, and proper tax planning through vehicles like self-employed bookkeeping and strategic deductions can minimize your actual tax burden. But the first step is eliminating this money myth that earning more money somehow results in earning less after taxes. It doesn’t. Learn about self-employment tax obligations in your state to make informed decisions.

Why these money myths matter so much

Each of these money myths operates as a hidden belief that shapes your financial behavior. You don’t actively “believe” them – they sit in the background, influencing your decisions without conscious awareness. The professional who believes they need a high income to build wealth makes different financial choices than someone who understands that savings rate matters more. The person who thinks cars are investments makes different purchasing decisions than someone who sees them as depreciating expenses.

Breaking free from money myths requires honest examination of your financial beliefs. Where did you learn them? Are they based on current reality or outdated information? What financial decisions have they influenced?

For self-employed professionals specifically, understanding these myths becomes even more critical. When you control your own income and business structure, your financial beliefs directly impact your bottom line. Exploring self-employment ideas and strategies becomes much more productive once you’ve cleared out the myths that were previously limiting your thinking.

Moving forward: building wealth based on reality

The path forward involves replacing these money myths with evidence-based financial principles. Focus on your savings rate rather than your absolute income. Evaluate education as an investment with clear returns. Understand that tax brackets reward, not punish, higher earnings. View your car as an expense, not an investment. And recognize that with intentional strategy, you can compress the wealth-building timeline significantly.

The good news? Once you identify which money myths have been holding you back, change happens quickly. You’ll make different decisions about money. You’ll negotiate higher rates. You’ll maintain higher savings rates. You’ll invest more strategically. These small, better decisions compound over time into dramatically different financial outcomes.

FAQ

What’s the difference between a money myth and actual financial advice?

Money myths are beliefs repeated so often they’re assumed true, but they lack evidence or contradict how modern economics actually works. Real financial advice is based on data, current tax law, and documented outcomes. If a financial belief makes you feel helpless or prevents you from taking action, it’s likely a money myth.

How do money myths form in the first place?

Money myths often come from outdated advice that was once true, family patterns passed down without examination, media narratives that oversimplify complex topics, or social comparison with people whose full financial pictures you can’t see. Once established, they’re reinforced because people tend to seek information confirming what they already believe.

Can I still build wealth if I believe some of these myths?

Yes, but it’s like driving with the handbrake partially engaged. You might eventually reach your destination, but it’s slower and more difficult. Clearing out money myths removes unnecessary obstacles and lets your effort translate more directly into results.

How much money do I actually need to start investing?

This depends on your investment vehicle, but many options exist for people starting with small amounts. Target-date funds, index funds, and even fractional share investing through most brokerages let you start with $100 or less. The key is starting, not the amount you start with.

Should I really limit my work because of taxes?

Absolutely not. In the US progressive tax system, earning more money always results in more take-home income, even after taxes. A higher tax bracket means only your income in that bracket is taxed at the higher rate. Work with a tax professional if you’re uncertain about your specific situation.

Is the savings rate really more important than income?

For building long-term wealth, yes. Two people with vastly different incomes can accumulate different amounts of wealth if their savings rates differ significantly. The person making $50,000 and saving 40% will build more wealth than the person making $200,000 and saving 5%.

How long does it really take to build meaningful wealth?

If you combine increased income, high savings rates, and strategic investing, you can build meaningful wealth in 5-10 years. Most people take longer because they do one or two of these things, not all three. The timeline expands primarily because most people don’t optimize all three variables simultaneously.