Colorado has long been a magnet for independent professionals, and having worked with self-employed clients from Denver to Durango over the years, I have seen firsthand why so many freelancers and entrepreneurs choose to build their careers here. The state’s flat income tax keeps things simple and predictable, the outdoor lifestyle attracts talented remote workers, and the business culture in cities like Boulder, Fort Collins, and Colorado Springs is deeply entrepreneurial. Understanding how Colorado’s tax system interacts with your federal self-employment obligations is the key to making the most of what this state has to offer.

Self Employment Tax Calculator

What Is Self-Employment Tax in Colorado?

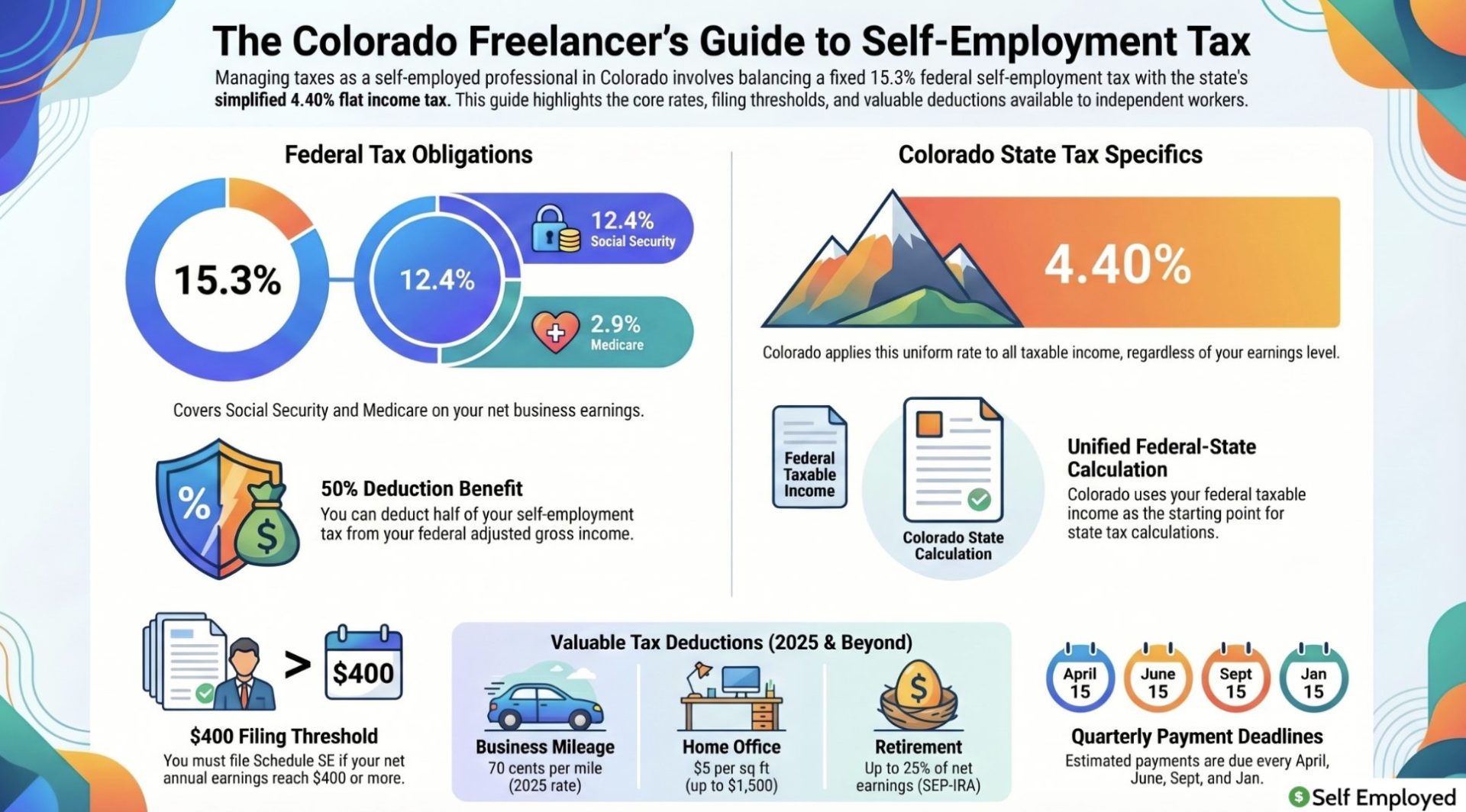

Self-employment tax is the federal tax through which independent workers fund Social Security and Medicare. Traditional W-2 employees split the 15.3% combined tax with their employer at 7.65% each, but self-employed individuals pay the full 15.3% themselves.

The 15.3% consists of two components. The Social Security portion is 12.4% and applies to net self-employment earnings up to the annual wage base, which is $176,100 for 2025 and increases to $184,500 for 2026. Earnings above those thresholds are not subject to the Social Security portion. The Medicare portion is 2.9% and applies to all net self-employment income with no cap. If your net earnings exceed $200,000 as a single filer or $250,000 filing jointly, an additional 0.9% Medicare surtax applies to income above that threshold.

You can deduct the employer-equivalent portion of your self-employment tax, 7.65%, from your adjusted gross income on your federal return. This deduction is available regardless of whether you itemize. You are required to pay self-employment tax and file Schedule SE when your net self-employment earnings reach $400 in a tax year.

Colorado State Income Tax for the Self-Employed

Colorado uses a flat income tax, which makes calculating your state tax liability straightforward. For tax year 2025, the flat rate is 4.40% on all Colorado taxable income. This rate applies uniformly regardless of your income level, which eliminates the complexity of navigating multiple brackets.

One unique aspect of Colorado’s system is that the state does not have its own standard deduction. Instead, Colorado uses your federal taxable income as the starting point for calculating state tax. Since your federal taxable income already reflects either the federal standard deduction or your itemized deductions, Colorado effectively piggybacks on the federal calculation. This simplifies preparation but also means that federal deductions have a direct impact on your Colorado tax liability.

Colorado’s flat rate has fluctuated in recent years due to the state’s TABOR (Taxpayer’s Bill of Rights) framework, which ties tax rates to revenue surpluses. The rate was 4.25% for a period before moving to 4.40% for 2025 when surplus revenue fell below the threshold needed to trigger a further reduction. The mechanism that adjusts the rate runs annually through 2034, so the rate could shift in future years depending on state revenue performance.

| Tax Year | Colorado Flat Rate |

|---|---|

| 2024 | 4.25% |

| 2025 | 4.40% |

| 2026 | 4.40% (subject to TABOR adjustment) |

Colorado does not impose a separate state-level self-employment tax or any local income taxes. Your self-employment income flows through to your Colorado Form DR 0104 and is taxed at the flat rate along with all other income.

How to File Self-Employment Taxes in Colorado

Filing self-employment taxes in Colorado involves coordinating your federal and state returns. On the federal side, you report business income and deductible expenses on Schedule C (Form 1040), which produces your net profit or loss. That net profit carries over to Schedule SE, where your self-employment tax is calculated. The resulting tax is added to your Form 1040, and the deductible half of the SE tax is subtracted from your adjusted gross income.

For Colorado, you file Form DR 0104. Your federal taxable income is the starting point, and Colorado allows certain additions and subtractions to arrive at Colorado taxable income. The flat 4.40% rate is then applied to determine your state tax. The filing deadline aligns with the federal deadline of April 15, with an automatic six-month extension available for filing, though you must pay at least 90% of your estimated tax by April 15 to avoid penalties.

If you received $600 or more from any single client during the tax year, that client should provide a Form 1099-NEC. Maintain organized records of all income from every source, including payments below the 1099 threshold. Colorado encourages electronic filing through Revenue Online at colorado.gov/revenueonline.

Quarterly Estimated Tax Payments in Colorado

Self-employed individuals must make estimated tax payments throughout the year. At the federal level, payments are required if you expect to owe $1,000 or more. Colorado requires estimated payments if you expect to owe more than $1,000 in state tax after withholding and credits.

| Payment Period | Due Date |

|---|---|

| January 1 – March 31 | April 15 |

| April 1 – May 31 | June 15 |

| June 1 – August 31 | September 15 |

| September 1 – December 31 | January 15 of the following year |

Because Colorado uses a flat rate, estimating your state tax is simple: take your projected annual federal taxable income, apply any Colorado-specific adjustments, and multiply by 4.40%. Divide by four for each quarterly installment. The safe harbor method of paying 100% of your prior year’s total tax liability (or 110% if AGI exceeded $150,000) across four installments protects against underpayment penalties. Use Form 1040-ES for federal payments and Colorado Form DR 0104EP for state payments.

Tax Deductions and Credits for Colorado’s Self-Employed

Since Colorado starts with your federal taxable income, every federal deduction you claim directly reduces your Colorado tax liability as well. This makes federal deduction strategy doubly valuable for Colorado’s self-employed workers.

The deduction for 50% of your self-employment tax reduces your AGI automatically, saving you on both your federal and Colorado state returns. The home office deduction provides $5 per square foot under the simplified method up to 300 square feet for a $1,500 maximum, or you can calculate actual expenses based on business-use percentage.

Self-employed individuals who pay their own health insurance premiums can deduct medical, dental, vision, and qualifying long-term care coverage from AGI. Retirement contributions through a SEP-IRA (up to 25% of net self-employment earnings) or Solo 401(k) reduce taxable income dollar for dollar. Business expenses such as software subscriptions, advertising, professional development, supplies, and professional fees are fully deductible. Vehicle use for business can be deducted at 70 cents per mile for 2025 or through actual expense tracking.

| Deduction Category | Details |

|---|---|

| Self-Employment Tax Deduction | 50% of SE tax, reduces AGI automatically |

| Home Office | Simplified: $5/sq ft (max $1,500) or actual expenses |

| Health Insurance Premiums | Medical, dental, vision, long-term care |

| Retirement Contributions | SEP-IRA (up to 25% of net SE income), Solo 401(k) |

| Business Expenses | Supplies, software, advertising, professional fees |

| Vehicle/Mileage | 70 cents/mile (2025) or actual vehicle expenses |

Avoiding Common Pitfalls

Not Tracking Rate Changes Year to Year

Colorado’s TABOR-linked rate adjustment mechanism means the flat rate can change from one year to the next based on state revenue. Using last year’s rate for your current estimated payments can result in underpayment or overpayment. Always verify the current year’s rate before calculating your quarterly installments.

Misclassifying Workers

Worker misclassification is a common issue in Colorado’s construction, outdoor recreation, and tech industries. If the IRS or Colorado Department of Revenue determines that someone you classified as a contractor is actually an employee, you could face back taxes, penalties, and interest. The determination hinges on the degree of control over when, where, and how the work is performed.

Neglecting Paid Family and Medical Leave

Colorado’s FAMLI (Family and Medical Leave Insurance) program, which launched in 2024, requires contributions from both employers and employees. Self-employed individuals can opt into the program voluntarily. If you opt in, you pay the full 0.9% premium on your wages. While participation is optional for the self-employed, it is worth understanding the program and making a deliberate decision about whether the benefits justify the cost.

Poor Recordkeeping

Maintaining organized records of all income and expenses is essential. Keep receipts for every business deduction, maintain mileage logs, and track income from all sources. Using accounting software and maintaining separate business and personal bank accounts simplifies the process significantly.

Final Thoughts on Self-Employment Tax in Colorado

Colorado’s flat 4.40% state income tax rate, combined with no local income taxes, creates a clean and predictable tax environment for self-employed professionals. The state’s approach of using federal taxable income as the starting point means that every federal deduction you claim automatically reduces your Colorado liability as well. Staying on top of quarterly estimated payments, taking full advantage of available deductions, and keeping thorough records are the pillars of effective tax management. For those with complex situations or questions about the FAMLI program or entity structuring, a tax professional familiar with Colorado’s system can provide valuable guidance.

Frequently Asked Questions

What is self-employment tax in Colorado?

Self-employment tax in Colorado is the federal tax that independent workers pay to fund Social Security and Medicare. The rate is 15.3% of net self-employment earnings, split between 12.4% for Social Security (on income up to $184,500 in 2026) and 2.9% for Medicare on all earnings. Colorado does not impose a separate state-level self-employment tax, but your self-employment income is subject to the state’s flat 4.40% income tax for 2025.

What is Colorado’s income tax rate?

Colorado uses a flat income tax rate of 4.40% for tax year 2025. This rate applies to all taxable income regardless of income level. The rate is subject to annual adjustment under Colorado’s TABOR framework based on state revenue surpluses, so it may change in future years.

When are quarterly estimated tax payments due in Colorado?

Quarterly estimated payments are due on April 15, June 15, September 15, and January 15 of the following year. These dates apply to both federal (Form 1040-ES) and Colorado (Form DR 0104EP) estimated payments. Colorado requires estimated payments if you expect to owe more than $1,000 in state tax after withholding and credits.

Does Colorado have local income taxes?

No. Colorado does not impose local or municipal income taxes. Your self-employment income is subject only to federal taxes and the state’s flat income tax rate, simplifying the filing process.

Self-Employment Tax Guides by State

- Check out self-employment tax rates for Hawaii

- See the self-employment tax guide for Maine

- Learn about self-employment taxes in Nevada

- Explore self-employment tax rates in Pennsylvania

- View the self-employment tax guide for Wisconsin

What deductions can I claim as a self-employed person in Colorado?

Self-employed individuals in Colorado can claim all standard federal deductions including 50% of self-employment tax, health insurance premiums, home office expenses, retirement contributions to a SEP-IRA or Solo 401(k), business vehicle mileage at 70 cents per mile for 2025, and ordinary business expenses. Because Colorado uses federal taxable income as its starting point, these deductions reduce both your federal and state tax liability.