I’ve guided thousands of self-employed professionals through health insurance decisions. After managing my own health coverage while building selfemployed.com, I understand the unique challenges we face. Let me share what I’ve learned about finding affordable, reliable health insurance in 2025-2026. Choosing health insurance when self-employed feels overwhelming. You’re navigating terminology like metal tiers, deductibles, and subsidies while also managing business decisions. I’m here to simplify this process and help you find coverage that actually works for your situation.

Current Health Insurance Costs for Self-Employed

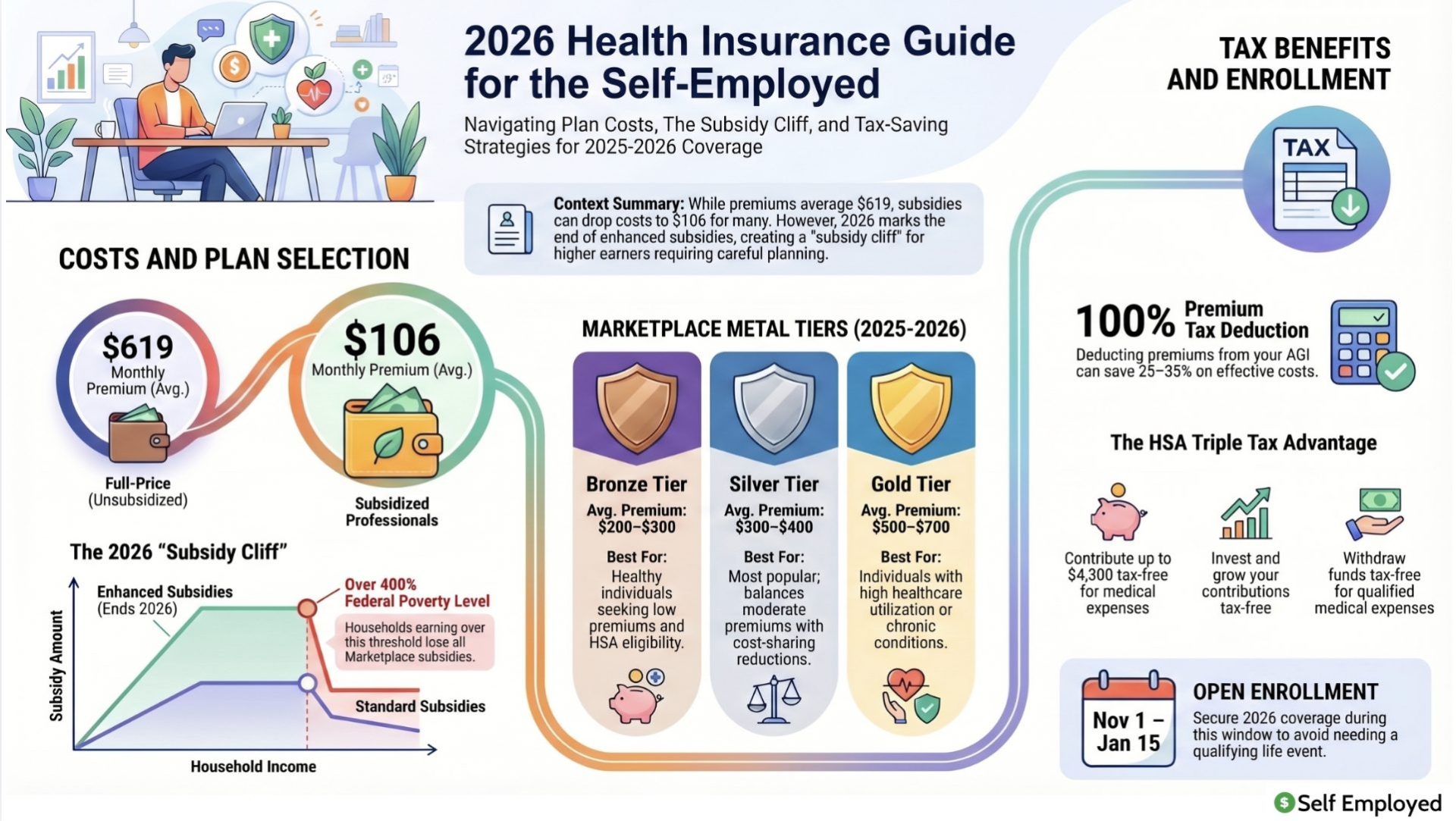

Here’s the realistic pricing landscape for 2025-2026: The average full-price Marketplace premium is $619 monthly. However, most self-employed professionals qualify for advance premium tax credits, significantly reducing actual costs. The average premium after tax credits is approximately $106 monthly. For a 40-year-old on the benchmark Silver plan, expect around $497 monthly before subsidies. Critically, important changes occurred in 2026. Congress allowed enhanced subsidies to expire, creating what’s called the “subsidy cliff.” Households earning above 400% of the federal poverty level no longer receive Marketplace subsidies in 2026. This means higher-income self-employed individuals may see significant premium increases. For 2026, you need to carefully run subsidy estimates to understand your exact costs. The good news: if you qualify for subsidies, your actual cost is often just $100-300 monthly for solid coverage.

Top Health Insurance Carriers for Self-Employed

Leading carriers serving self-employed individuals in 2025-2026 include Blue Cross Blue Shield, which provides broad network access and plan options in most states. UnitedHealthcare offers comprehensive coverage with strong customer service. Aetna provides excellent options for those optimizing tax benefits. Oscar appeals to tech-savvy individuals seeking streamlined digital experiences. Ambetter and Cigna also serve the self-employed market effectively. Each carrier offers plans at different metal tiers. Your choice should balance monthly premiums against out-of-pocket costs based on your expected healthcare utilization.

Understanding ACA Metal Tiers

Marketplace plans are categorized into four metal tiers based on how costs are shared between you and the insurance company:

- Bronze plans: feature the lowest premiums ($200-300 monthly) but highest deductibles ($6,000-$7,000). You pay for most routine care. Bronze works if you’re young, healthy, and rarely visit doctors. New for 2026, Bronze plans now qualify as High-Deductible Health Plans (HDHP), enabling Health Savings Account (HSA) contributions.

- Silver plans: are the most popular for self-employed individuals. They balance moderate premiums ($300-400 monthly) with reasonable deductibles ($3,000-$5,000). Silver plans also qualify for cost-sharing reductions, further lowering out-of-pocket expenses for those who qualify.

- Gold plans: have higher premiums ($500-700 monthly) but lower deductibles ($1,000-$3,000). They make sense if you expect significant healthcare expenses or prefer predictable out-of-pocket costs.

- Platinum plans: feature the highest premiums ($900-1,200 monthly) with lowest deductibles ($500-$1,000). Only rarely does this make sense for self-employed individuals.

Tax Benefits That Reduce Effective Costs

Here’s where health insurance becomes truly affordable for self-employed people: tax deductions. Since 2003, self-employed individuals can deduct 100% of health insurance premiums on their tax returns. This reduction to adjusted gross income (AGI) effectively saves you 25-35% of premium costs through tax savings, depending on your tax bracket. Example: If you pay $300 monthly ($3,600 annually) in premiums, and your tax bracket is 25%, the deduction saves you $900 in taxes. Your effective premium cost drops to $2,700 annually, or $225 monthly. Additionally, if you enroll in a high-deductible health plan (HDHP) like Bronze or Silver plans, you can open a Health Savings Account (HSA). HSAs offer triple tax advantages: tax-deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses. In 2026, you can contribute $4,300 annually to your HSA (individual coverage). This further reduces your taxable income while building a medical expense fund.

Choosing Your Insurance Strategy

Assess your health needs first. Do you have chronic conditions requiring regular care? Take medications? If yes, Silver or Gold plans make sense. If you’re young and healthy, Bronze offers sufficient protection at lower cost. Evaluate your expected out-of-pocket spending. Add your monthly premium to your deductible. What’s your total worst-case expense if you need significant care? Compare this across metal tiers. Run your subsidies. Visit healthcare.gov and input your expected 2026 income. The system shows exactly what you’ll pay monthly at each metal tier with subsidies applied. Don’t guess your income—this drives subsidy accuracy. Consider HSA eligibility. If enrolled in an HDHP (Bronze or Silver qualifying), you can contribute to an HSA. This triple-tax-advantaged account can cover medical expenses or grow for retirement after age 65.

Enrollment Timeline for 2026

Open Enrollment for 2026 coverage runs from November 1, 2025, through January 15, 2026. If you miss this window, you need a qualifying life event (marriage, birth, relocation, income change, etc.) to enroll outside the annual period. Special enrollment periods also exist. Turning 26 and losing parent coverage, losing employer insurance, or experiencing income fluctuations may qualify you for enrollment windows outside the standard Open Enrollment Period.

FAQs About Self-Employed Health Insurance

Full-price Marketplace premiums average $619 monthly. With subsidies, average actual cost is $106 monthly. However, the 2026 subsidy cliff means higher-income self-employed individuals may face $400-800+ monthly premiums.

Yes, 100% of your health insurance premiums are deductible as an adjustment to AGI. This effectively reduces your cost 25-35% through tax savings, depending on your tax bracket.

Congress allowed subsidy enhancements to expire at the end of 2025. Households earning above 400% of federal poverty level ($59,100 for individuals) no longer receive Marketplace subsidies in 2026. Run your income estimates on healthcare.gov to determine your actual costs.

Silver plans are typically optimal, balancing moderate premiums with reasonable deductibles and qualifying for cost-sharing reductions. Bronze works for young, healthy individuals. Gold suits those expecting significant healthcare needs.

Yes, if you enroll in a high-deductible health plan. For 2026, Bronze and Silver qualifying plans are considered HDHPs, enabling HSA contributions ($4,300 individual annual limit) for triple tax advantages.

Open Enrollment runs November 1, 2025, through January 15, 2026. You need a qualifying life event to enroll outside this window.

## My Final Recommendation For most self-employed professionals in 2025-2026, I recommend a Silver plan through the Marketplace. Here’s why: Silver plans balance premium costs with reasonable deductibles. If you qualify for subsidies, they’re incredibly affordable. If you don’t qualify (due to higher income), the tax deduction makes them manageable. If you’re young and healthy, consider Bronze to reduce premiums. Immediately open an HSA to capture triple tax advantages. If you expect significant healthcare costs, Gold plans provide better predictability. Most importantly: don’t skip enrollment. The individual mandate penalty ended, but health insurance protects you from catastrophic medical debt. One unexpected hospitalization without insurance could devastate your business finances. Start by visiting healthcare.gov during Open Enrollment. Run your income estimate, compare plans, and select coverage. The process takes about 20 minutes. This single action protects your business and health for the coming year.